[ad_1]

Up to date on November thirtieth, 2023 by Bob Ciura

Actual Property Funding Trusts (i.e., “REITs”) are tax-advantaged earnings automobiles which have turn out to be more and more fashionable with earnings buyers. It’s because they don’t have to pay any earnings tax on the company stage however as a substitute function pass-through entities. In alternate for this profit, they have to meet particular tips, together with paying out at the least 90% of taxable earnings to shareholders by dividends.

In consequence, high-yield and dividend-growth buyers usually love REITs and dedicate a substantial portion of their portfolios to them.

You’ll be able to obtain our full record of REITs, together with vital metrics similar to dividend yields and market capitalizations, by clicking on the hyperlink under:

Nonetheless, whereas REITs would not have to pay company earnings tax, shareholders usually should pay tax on the dividend earnings they obtain from them. This earnings is mostly taxed in certainly one of 3 ways:

Capital Good points – this portion of the dividend consists of features generated from asset gross sales and are taxed as capital features.

Return of Capital – this portion of the dividend isn’t taxable, because it includes a discount within the investor’s price foundation. This money circulate usually both comes from the rental earnings that’s written off by way of depreciation accounting guidelines for the underlying actual property or isn’t lined by money circulate in any respect and as a substitute is being funded with money reserves and/or debt. Ultimately, capital features taxes might be paid on this portion of the earnings if/when the shareholder decides to promote his shares.

Odd earnings – is the portion of the dividend earnings that is still after the capital features and return of capital parts are deducted. It’s taxed on the shareholder’s high earnings tax bracket, although it’s exempted from FICA taxes. That is in distinction to the “certified dividends” that many corporations pay, that are taxed at long-term capital features charges, that are usually equal to or lower than the highest earnings tax bracket of the person shareholder.

Out of those classifications of REIT dividends, return of capital is probably the most fascinating because it defers all taxation on the dividends till the REIT shares are bought. Capital features are the subsequent most fascinating, provided that the capital features tax charge is often decrease than the earnings tax charge, making the odd earnings classification the least fascinating of REIT dividend classifications. One other essential tax consideration to bear in mind when holding REITs in a taxable account is that they profit from the 20% pass-thru earnings deduction. Provided that REITs are labeled as pass-thru entities, 20% of their dividends are exempted from taxation, additional limiting the tax legal responsibility for shareholders holding REITs in a taxable account.

What this implies is that when you maintain a REIT with a meaningfully excessive share of its dividends being labeled as a return of capital for the long run, when mixed with the 20% pass-thru earnings deduction, the tax burden could wind up being fairly affordable in a taxable account.

On this article, we’ll talk about seven REITs that paid out a significant share of their dividends as a return of capital in 2021 as a place to begin for buyers who wish to spend money on tax-efficient REITs in a taxable account. Word that this breakdown usually adjustments from 12 months to 12 months.

The breakdown for the earlier 12 months’s dividends is often introduced in January, so it’s unattainable to foretell future taxation classifications with certainty.

Desk of Contents

You’ll be able to immediately bounce to any particular part of the article by utilizing the hyperlinks under:

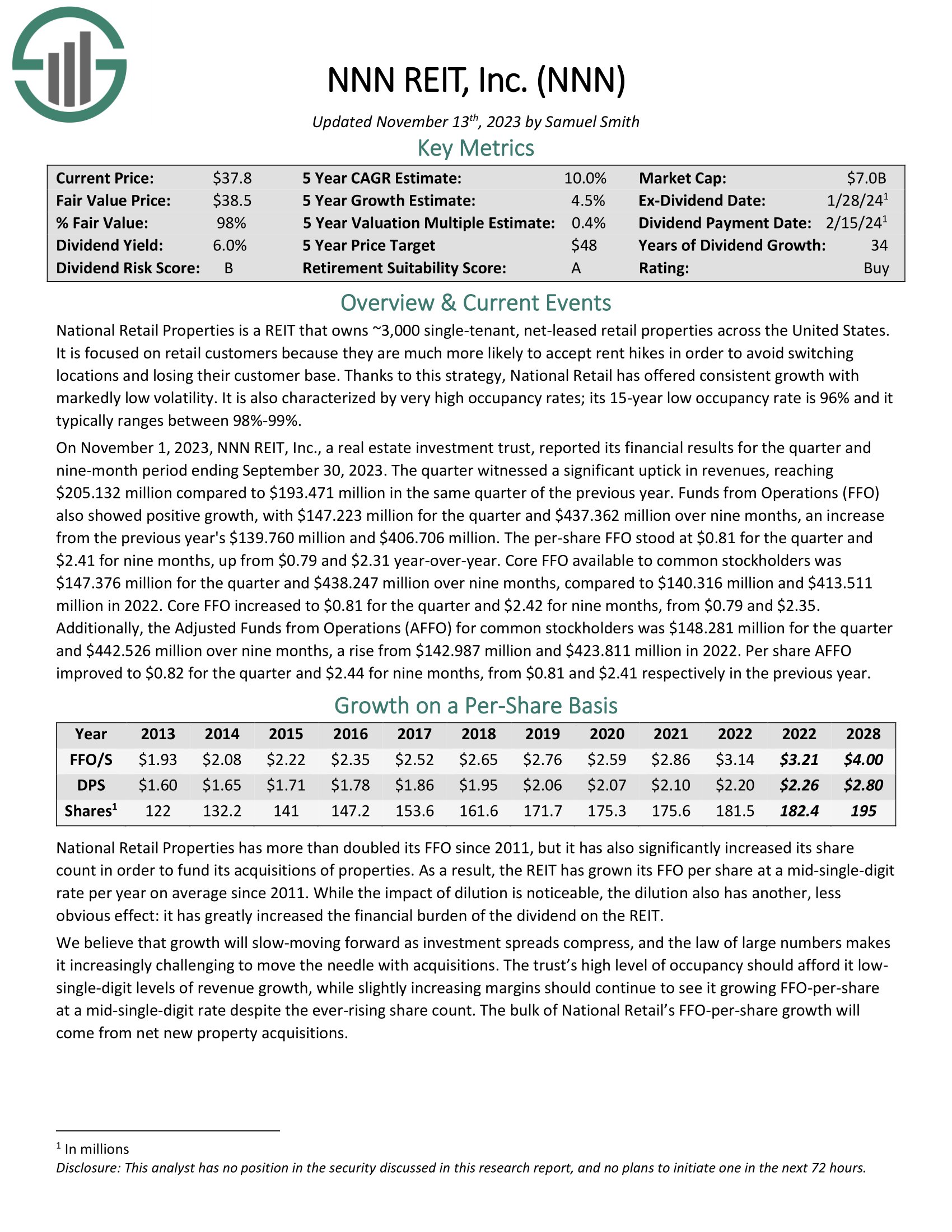

#1. Nationwide Retail Properties (NNN)

NNN is a triple internet lease REIT that primarily owns single-tenant free-standing retail actual property. The enterprise mannequin is a low threat provided that the tenant bears all accountability for working bills, insurance coverage, and property upkeep, the leases are prolonged in phrases and have seniority on the stability sheet, and NNN’s administration fastidiously does the underwriting.

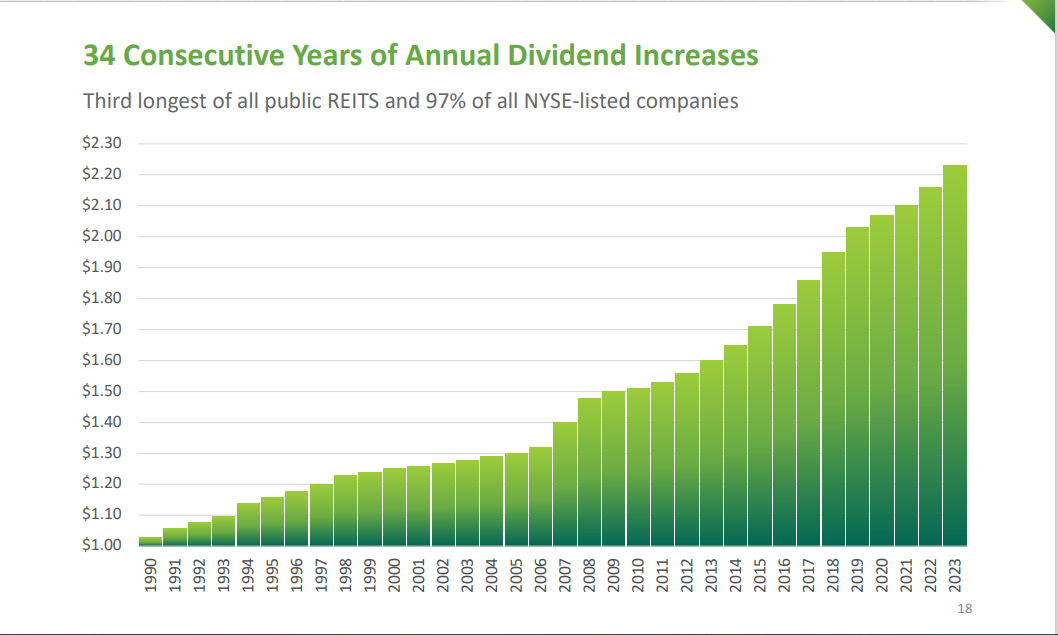

Its great observe file of producing steady and commonly rising money circulate from its actual property portfolio has enabled the REIT to extend its dividend for over 30 consecutive years, making it a Dividend Champion.

Supply: Investor Presentation

In 2022, its dividend breakdown was as follows: 99.83% was labeled as odd earnings. When mixed with the 20% pass-thru earnings deduction, NNN qualifies as a reasonably tax-efficient supply of reliable earnings.

Click on right here to obtain our most up-to-date Certain Evaluation report on Nationwide Retail Properties (preview of web page 1 of three proven under):

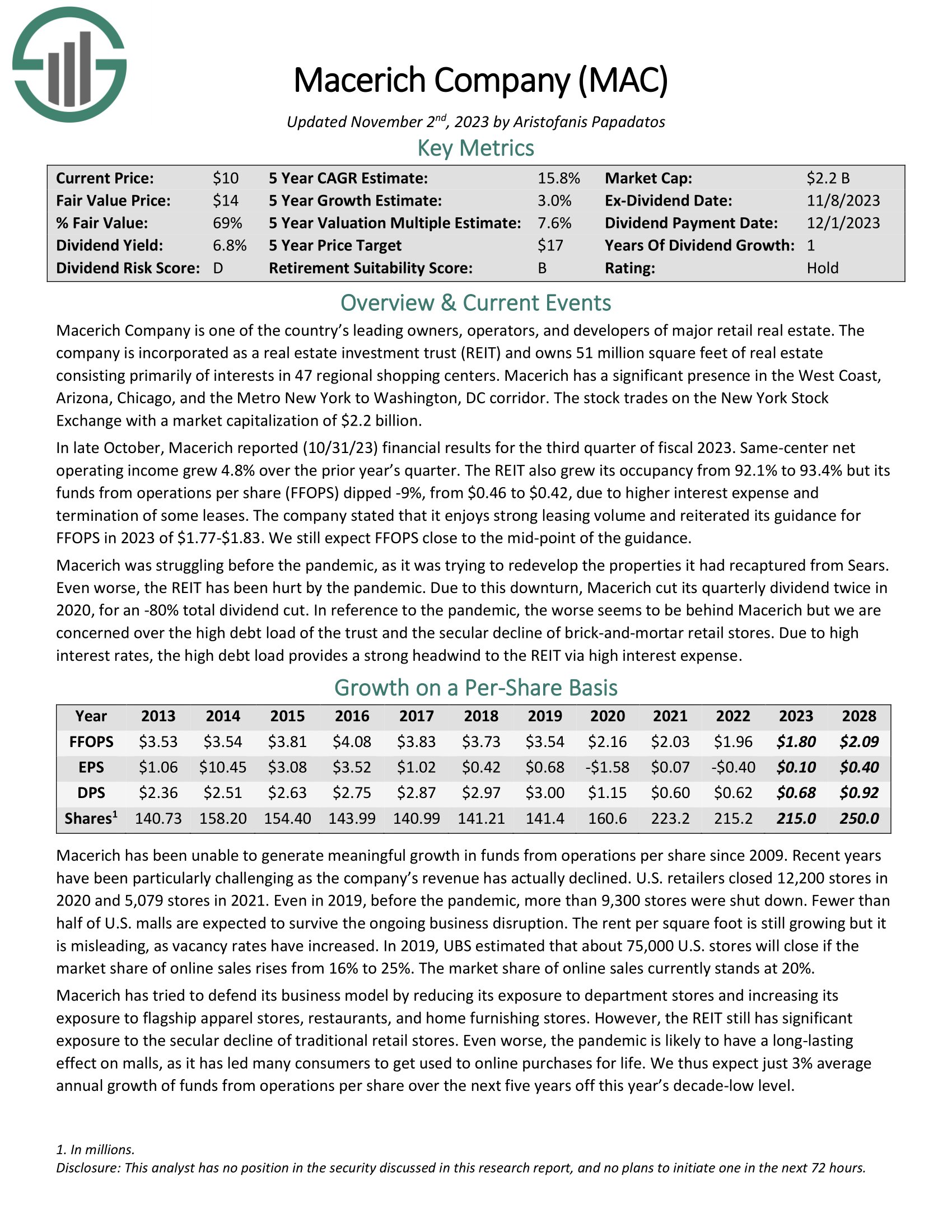

#2. Macerich (MAC)

MAC primarily owns class-A malls in main markets throughout america. Whereas it has struggled in recent times as a consequence of a surge in tenant bankruptcies because of the rise of e-commerce and the COVID-19 lockdowns, its properties at this time are thriving.

Whereas its dividend observe file is poor and the stability sheet may use additional deleveraging within the present setting, its properties are among the many finest positioned to thrive long-term within the mall sector.

In 2022, its dividend breakdown was as follows: roughly 80% was labeled as odd earnings, 8% was labeled as capital features, and the rest was labeled as return of capital. When mixed with the 20% pass-thru earnings deduction, MAC qualifies as a really tax-efficient supply of earnings.

Click on right here to obtain our most up-to-date Certain Evaluation report on Macerich (preview of web page 1 of three proven under):

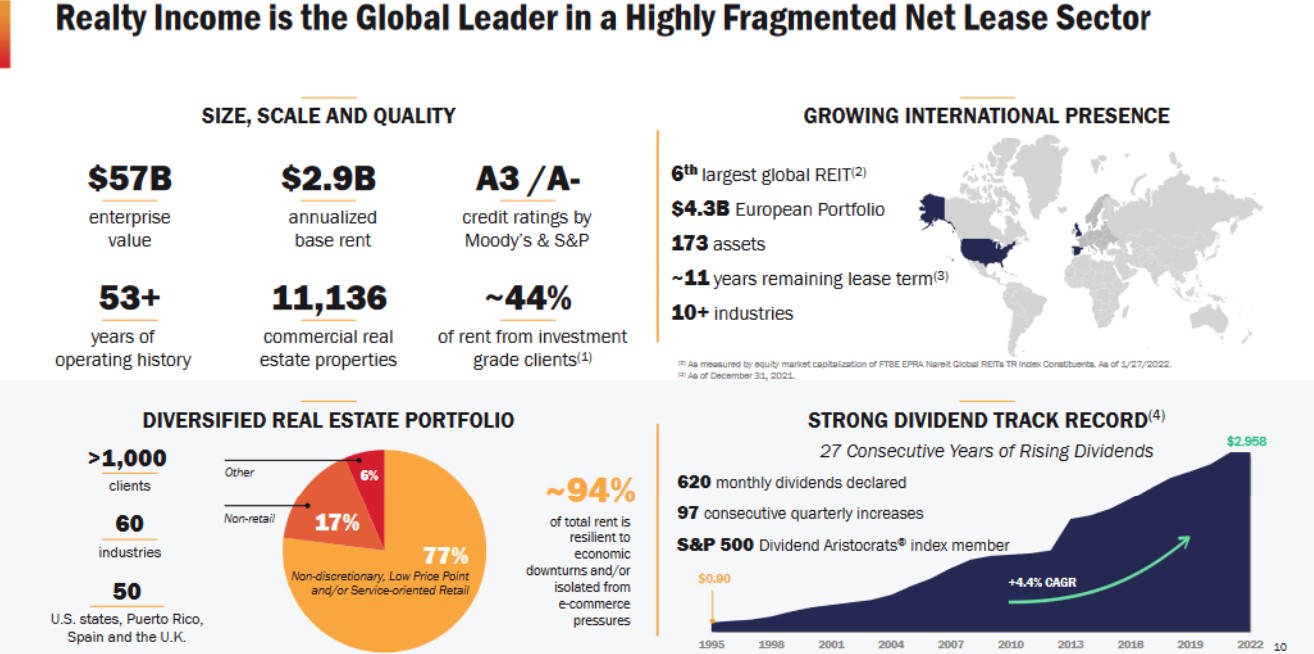

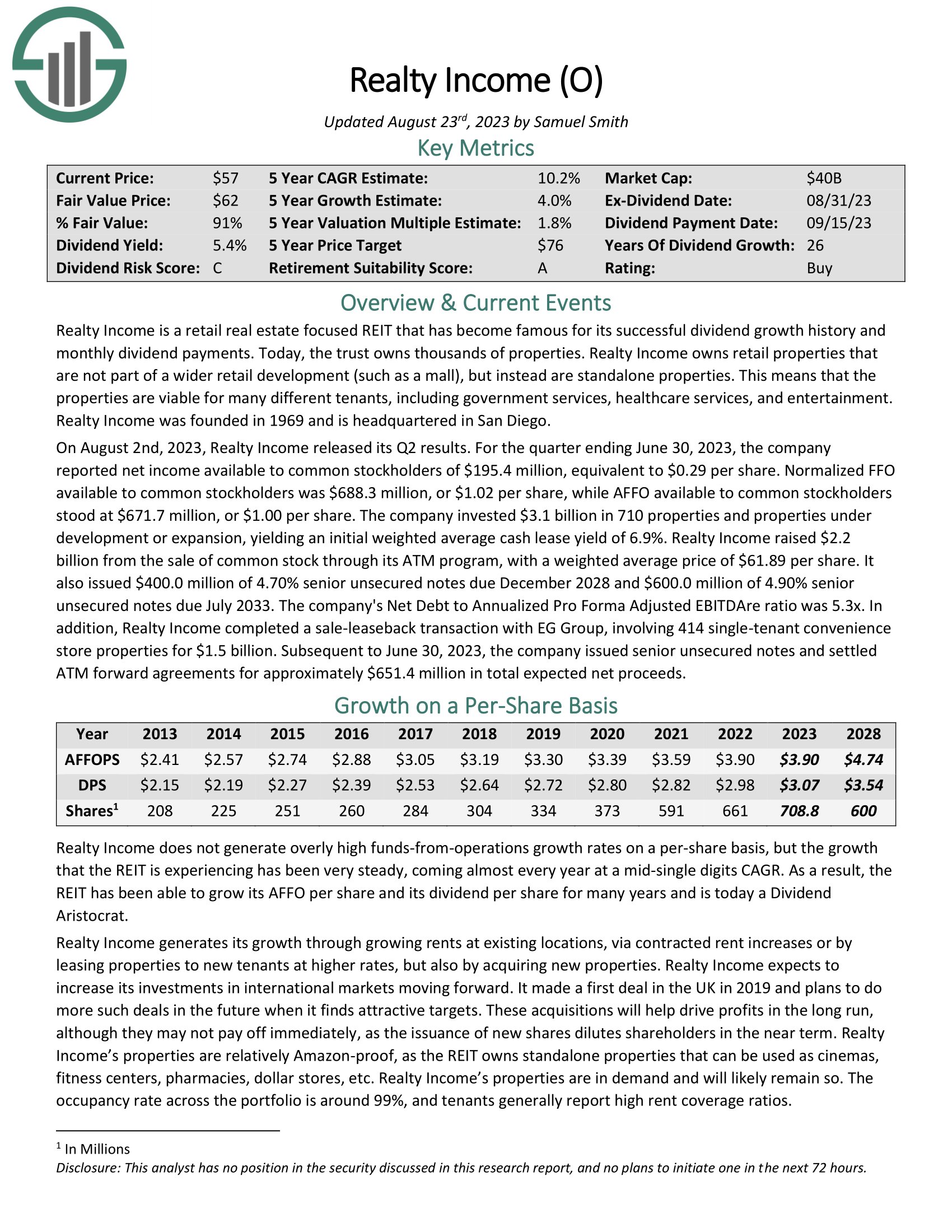

#3. Realty Earnings (O)

O isn’t labeled “The Month-to-month Dividend Firm” for nothing: it has an incredible observe file of paying month-to-month dividends that develop year-over-year. Its dividend progress streak makes it a Dividend Aristocrat.

Supply: Investor Presentation

On high of that, administration has applied its conservative triple internet lease enterprise mannequin to close perfection, delivering market-crushing whole returns all through its publicly traded existence because the Nineteen Nineties and constructing probably the most intensive portfolio of triple internet lease actual property on the earth. The stability sheet can be stellar, with one of many highest credit score rankings within the REIT sector, giving it a price of capital benefit over friends and implying that it is without doubt one of the lowest-risk actual property investments out there. With a 4.6% present dividend yield, it is usually a wholesome supply of present earnings.

In 2021, its dividend breakdown was as follows: 30.958% was labeled as odd earnings, 1.747% was labeled as capital features, and 67.295% was labeled as return of capital. When mixed with the 20% pass-thru earnings deduction, O qualifies as a really tax-efficient supply of reliable earnings.

Click on right here to obtain our most up-to-date Certain Evaluation report on Realty Earnings (preview of web page 1 of three proven under):

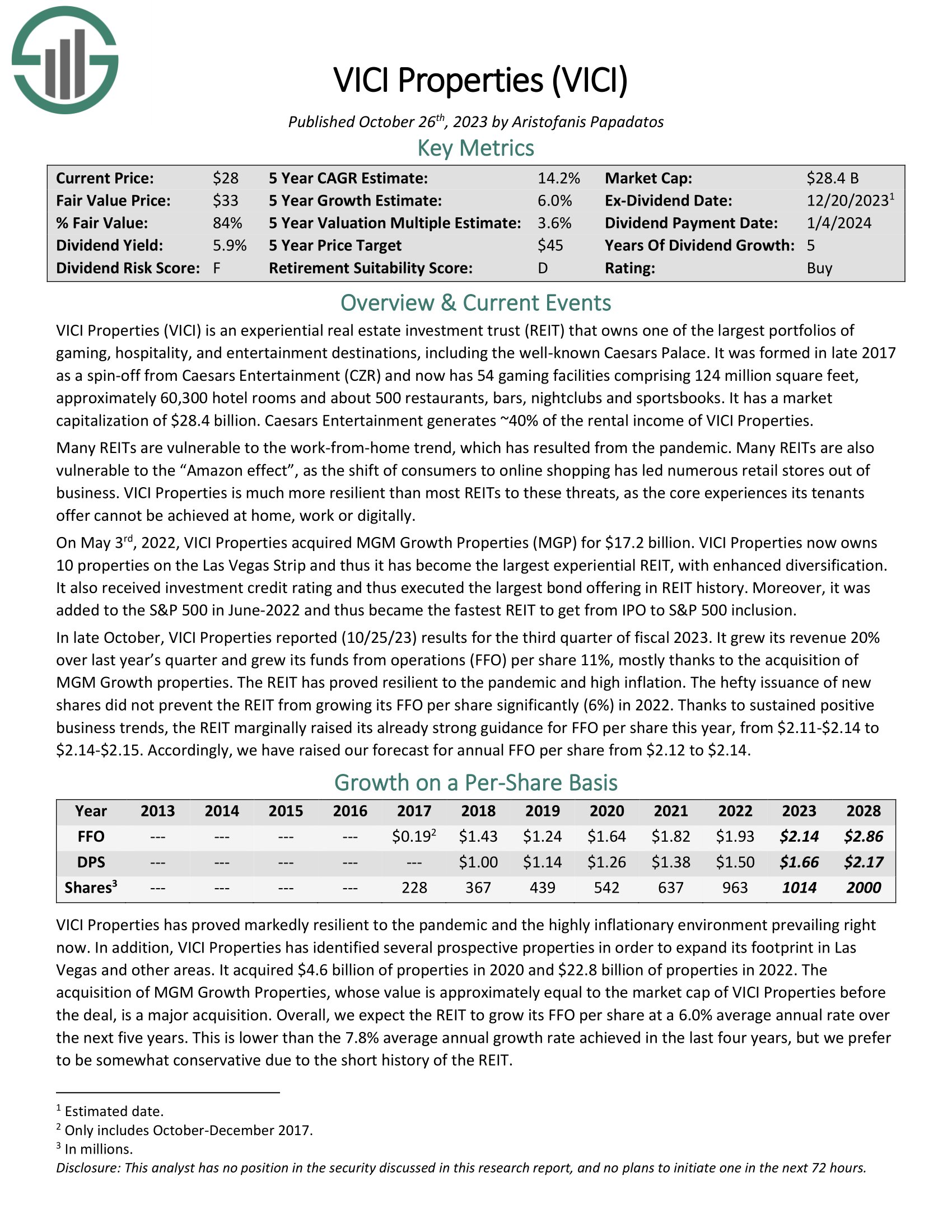

#4. VICI Properties (VICI)

VICI owns an in depth portfolio of casinos – together with the well-known Caesars Palace – in addition to lots of of eating places, bars, and nightclubs. It implements a triple internet lease enterprise mannequin, resulting in steady and persistently rising rental earnings from its actual property portfolio. In consequence, it has been capable of generate rising dividends per share annually since going public again in 2017 and is predicted to proceed doing so for years to return. On high of that, its 4.9% present dividend yield makes it a great choose for income-focused buyers.

In 2021, its dividend breakdown was as follows: 52.652% was labeled as odd earnings, and 47.348% was labeled as return of capital. When mixed with the 20% pass-thru earnings deduction, VICI qualifies as a really tax-efficient supply of reliable earnings.

Click on right here to obtain our most up-to-date Certain Evaluation report on VICI Properties (preview of web page 1 of three proven under):

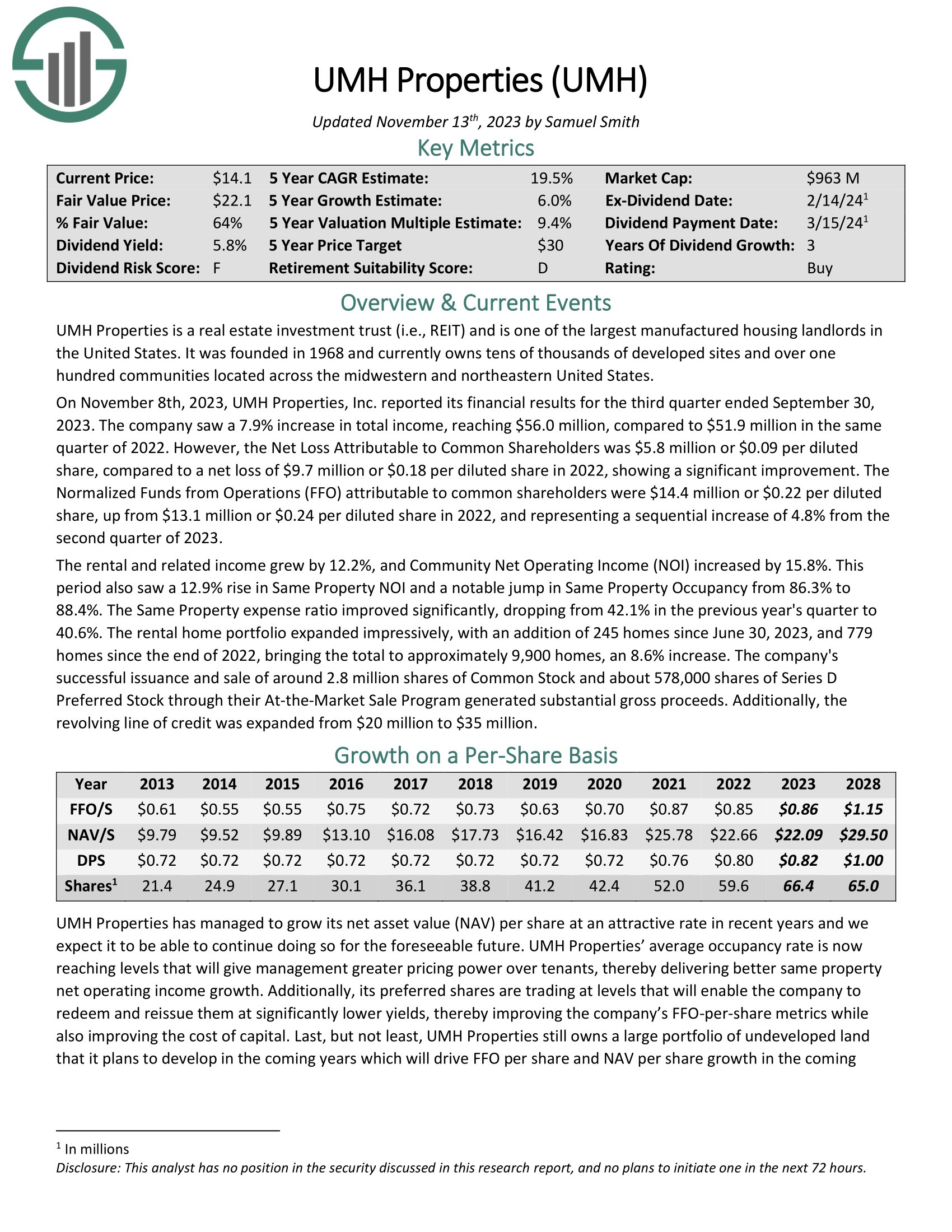

#5. UMH Properties (UMH)

UMH owns manufactured housing communities throughout america and at present owns tens of 1000’s of properties in over 100 communities within the Midwest and Northeast.

On November eighth, 2023, UMH Properties, Inc. reported its monetary outcomes for the third quarter. The corporate noticed a 7.9% enhance in whole earnings, reaching $56.0 million, in comparison with $51.9 million in the identical quarter of 2022.

The Normalized Funds from Operations (FFO) attributable to widespread shareholders have been $14.4 million or $0.22 per diluted share, up from $13.1 million or $0.24 per diluted share in 2022, and representing a sequential enhance of 4.8% from the second quarter of 2023.

In 2022, its dividend breakdown was as follows: 100% was labeled as return of capital. When mixed with the 20% pass-thru earnings deduction, UMH clearly qualifies as a extremely tax-efficient supply of reliable earnings.

Click on right here to obtain our most up-to-date Certain Evaluation report on UMH Properties (preview of web page 1 of three proven under):

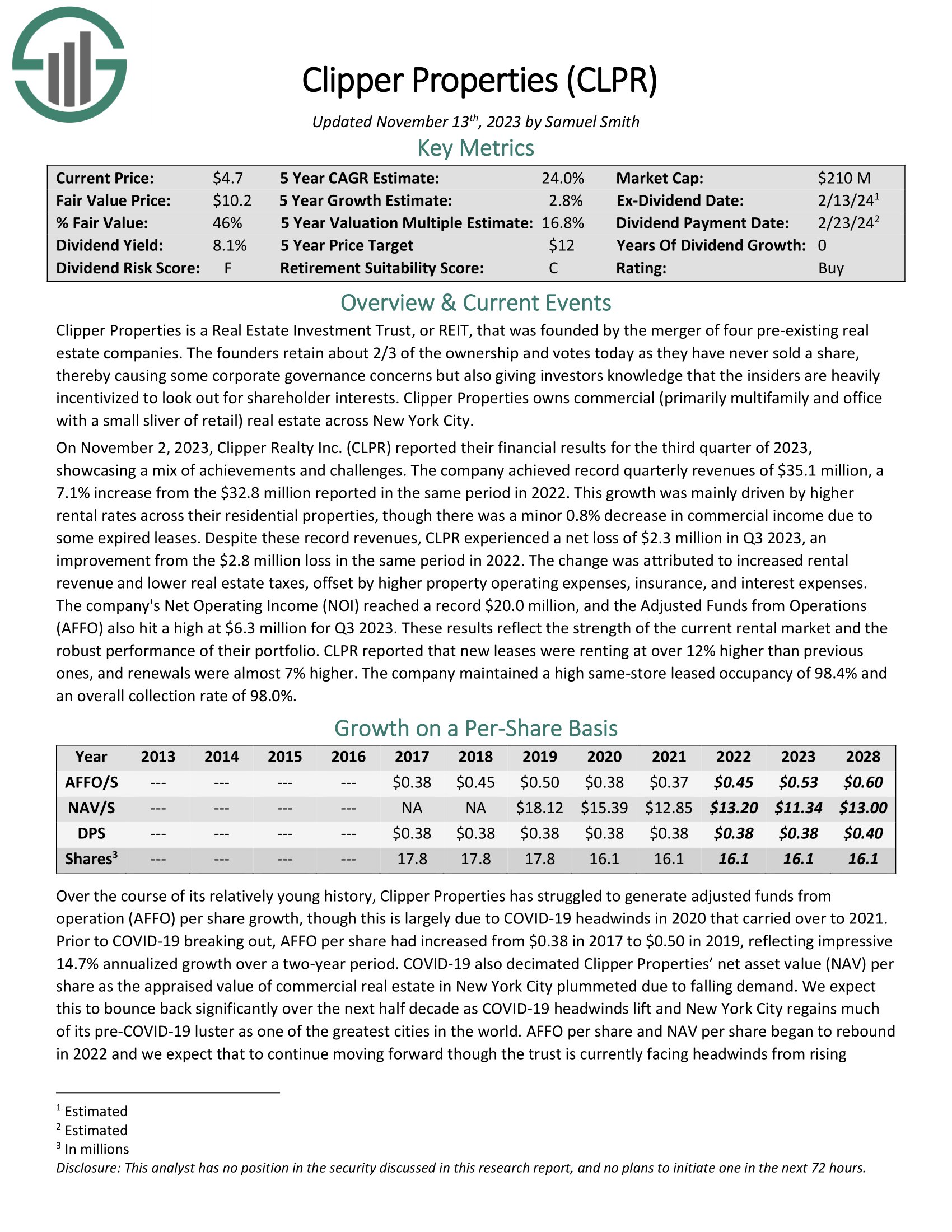

#6. Clipper Realty Inc. (CLPR)

CLPR primarily owns multifamily and workplace actual property in New York Metropolis and is owned roughly two-thirds by the founders of the REIT. It was a merger between 4 pre-existing actual property companies and went public in 2017. It has paid out a flat $0.38 annualized dividend annually since going public.

It at present provides buyers a dividend yield of seven.4%, making it a sexy choose for buyers searching for predictable present earnings alongside publicity to high quality actual property in one of many world’s biggest cities.

In 2022, its dividend breakdown was as follows: 75% was labeled as odd earnings, and 25% was labeled as return of capital. When mixed with the 20% pass-thru earnings deduction, CLPR qualifies as a really tax-efficient supply of reliable earnings.

Click on right here to obtain our most up-to-date Certain Evaluation report on Clipper Realty Inc. (preview of web page 1 of three proven under):

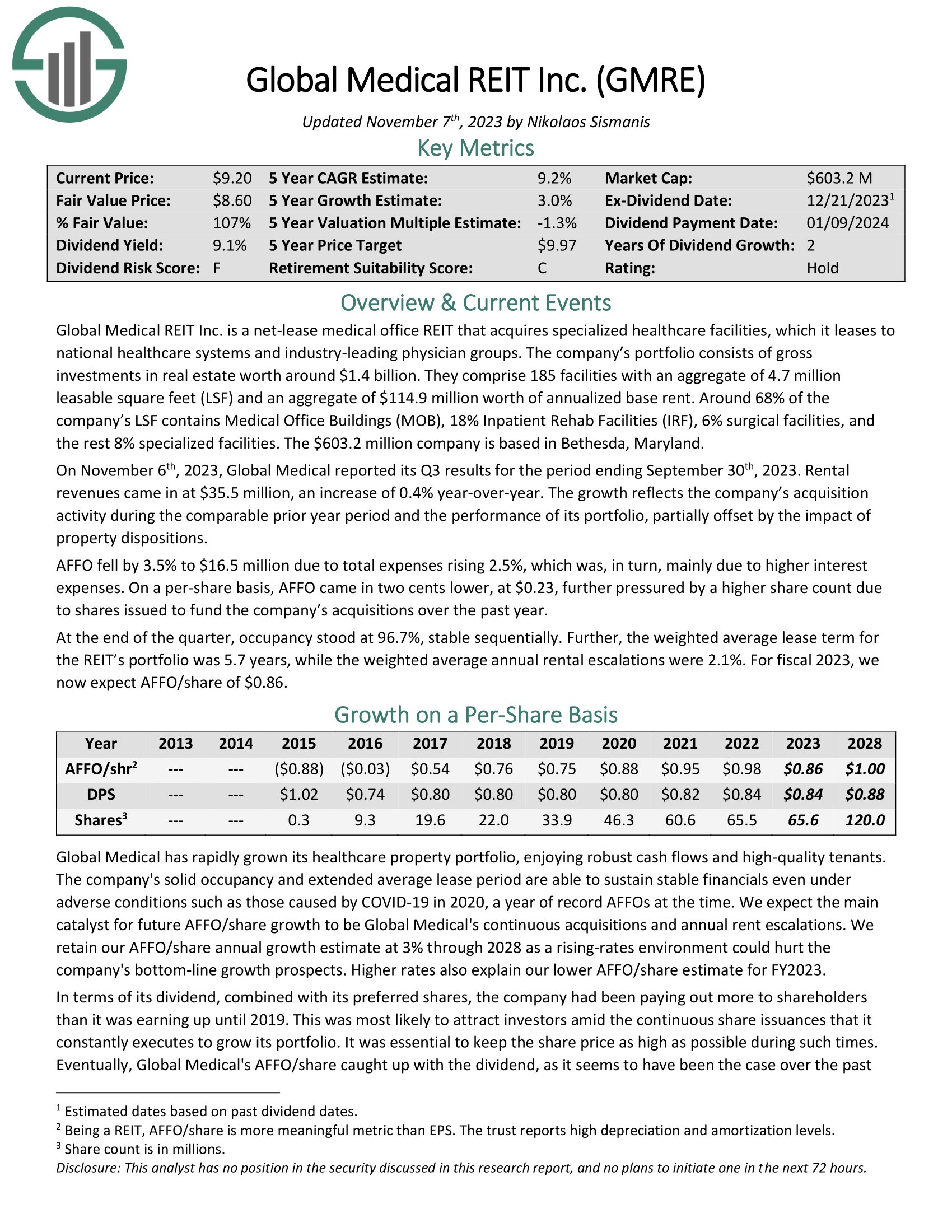

#7. World Medical REIT (GMRE)

GMRE is a net-lease medical workplace REIT that owns and leases out specialised healthcare services, together with medical workplace buildings, inpatient rehab services, surgical services, and different specialised services. Since going public in 2015, GMRE has seen its adjusted funds from operations per share enhance steadily.

The present annualized dividend payout is $0.84, and the present yield is 8.4%. The dividend payout is predicted to extend barely shifting ahead, making it an attractive selection for buyers searching for present earnings and at the least some progress.

In 2022, its dividend breakdown was as follows: 58% was labeled as odd earnings, and 42% because the return of capital. When mixed with the 20% pass-thru earnings deduction, GMRE qualifies as a comparatively first rate tax-efficient supply of reliable earnings, although not fairly as environment friendly as among the different choices introduced right here.

Click on right here to obtain our most up-to-date Certain Evaluation report on World Medical REIT (preview of web page 1 of three proven under):

Last Ideas

REITs are recognized for being very tax-efficient on the company stage, usually solely having to fret about paying property taxes and being solely exempted from the pricey company earnings tax. Moreover, pass-through entities get a 20% earnings tax exemption on their dividend payouts to shareholders, making them much more enticing as tax-advantaged investments.

On high of that, the true property depth of the enterprise mannequin usually signifies that they get to write down off a good portion of their rental earnings because the depreciation of their belongings. Whereas many REITs would not have a lot depreciation to write down off, some get to categorise a surprisingly massive share of their dividends as depreciation, making them remarkably tax-efficient even in a taxable account.

The draw back is that REITs solely reveal the tax classification of their dividends after they’ve been paid out, so it may be troublesome for buyers to know which REITs are finest to carry in a taxable account versus a tax-advantaged account like an IRA or 401k. In consequence, some could merely play it secure and maintain all REITs – particularly the highest-yielding ones – in a tax-advantaged account. That stated, when you discover {that a} particular REIT has developed a current sample of paying out a excessive share of its dividends as a return of capital, there’s a good likelihood that it’s going to stay that manner for the foreseeable future as this will likely merely be as a consequence of its distinctive enterprise mannequin.

In the end, REITs are most valued for his or her earnings, and buyers will usually be finest served by focusing totally on the dividend yield, valuation, administration, stability sheet energy, and underlying actual property high quality over the tax intricacies of the dividends. Nonetheless, it’s worthwhile for buyers in high-income tax brackets who personal a considerable REIT portfolio to attempt to maintain extra tax-efficient REITs in taxable accounts. Word that this isn’t tax recommendation, and readers are strongly inspired to do their due diligence earlier than investing.

You might also be searching for interesting shares from a sure inventory market sector to make sure applicable diversification inside your portfolio. If that’s the case, you will see that the next sources helpful:

You might also want to think about different investments inside the main market indices. Our downloadable record of small-cap U.S. shares will be accessed under:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to assist@suredividend.com.

[ad_2]

Source link