[ad_1]

Monty Rakusen

Expensive readers/subscribers,

I coated Healthpeak (NYSE:DOC) about 2 months in the past in our personal funding group, iREIT on Alpha. With its numerous portfolio of life science properties, outpatient medical care amenities, and persevering with care retirement communities, it has a really fascinating mixture of property, and is without doubt one of the extra fascinating healthcare REIT performs that we will see right here.

Like with many different REITs, this firm is unlikely to see vital AFFO progress within the close to time period – by that I imply {that a} sub-6% annual progress in AFFO is probably going. The mixed upside from these investments comes within the form of two issues – first off, the low valuation for the funding that they’re presently buying and selling at. Like different gamers within the area, on a historic foundation, PEAK is sort of undervalued to the place it sometimes trades.

Secondly, a superb yield. As PEAK trades now, it is over 6% yield, near 7% the truth is, and even at an elevated kind of risk-free price of round 3-4% relying on the place you make investments and the place you reside, that’s nonetheless a great yield with a really excessive price of security.

This can be a follow-up to my article, and since then the corporate has modified its image to DOC and nonetheless is at a really low kind of valuation. I’ve been growing my publicity to this REIT, as I view this as an overreaction, and I’ll present you why that’s.

Healthpeak – Why you need to make investments at near 7% Yield

DOC, because the image is now, is a high-quality healthcare play within the REIT sector. What do I imply by high-quality, and what do I imply by healthcare right here particularly?

Properly, like friends like Alexandria (ARE), this firm is within the section of healthcare and biopharma lab area – however in contrast to ARE, it additionally has a big portfolio of healthcare/hospital property. When it comes to combine, that is round 50% to life science, with solely 40% Outpatient medical care, and solely 10% persevering with care communities, which might by some be thought of the very best threat in these kinds of performs.

Properly, this firm has the least quantity of this and enhances this with an extra addition of high quality – if not essentially an addition of progress for the corporate (as I discussed, it appears that evidently progress is unlikely right here within the close to time period, with a same-store progress of solely 2-3% for the 2024 fiscal outlook) (Supply: DOC IR).

However there’s lots extra upside available for DOC – and plenty of extra arguments as to why it is a good funding.

Let’s start with what must be your first precedence when placing capital into any funding. Simply how secure is that this firm?

Whereas it is not possible for me to ensure the veracity or success of any funding, we will put ourselves in a great potential for outperformance by choosing above-average corporations. At a 5.2x Web debt/EBITDA for a REIT, this firm is among the many least leveraged on this sector. At $3B of liquidity, there’s loads of money for the corporate on the books right here, and being underwater in a fundamental funding over the previous 1-2 months presently (Intrum, a tough play with upside maybe in 4-5 years), I do know the worth of accessing loads of money.

The corporate proved simply how good its credit score is by just lately signing a 5-year $750M time period mortgage swap to a set price of 4.5%. That, for a REIT, is an indication of confidence on this market.

The most important set of stories for this firm, and the primary purpose for my replace on Healthpeak is the merger with Physicians Realty Belief lower than 2 weeks in the past.

DOC IR (DOC IR)

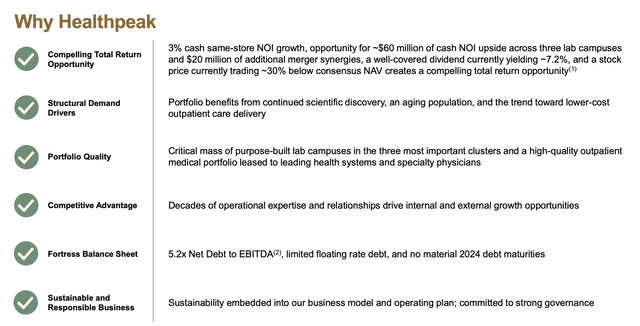

This merger now contains $40M price of merger synergies for this yr, with further administration internalization upsides, and likewise getting again $69M price in proceeds from repayments of vendor financing loans. The 2025E, which is in over a yr, has an upside of $60M NOI in money from untapped synergies and present downtime in trophy lab campuses. As well as, at these valuations, DOC may simply funnel a few of its incoming money pile into accretive buybacks of shares.

AFFO is anticipated to return in at $1.5-$1.56, which suggests it theoretically may are available under (barely) the 2023 degree. However at a dividend cost of $1.2, this leaves ample security within the equation, even when the 2024E progress estimate is unlikely to be all that good.

Why is that this maybe a great factor for traders?

It permits us the chance to get this firm at a really low-cost valuation – extra on that valuation later, however it’s an excellent upside should you enable any kind of premiumization for what is basically a BBB+-rated firm.

The brand new mixed administration group has over 200 years of mixed expertise. This expertise and this efficiency are confirmed by a really stable lease execution with 2023E above the 3-year common, with 5.1M sqft leased, marking report or near-record lease executions throughout a really tough time.

The corporate ends the fiscal with a same-store occupancy of over 92% in outpatient, and 90% of the lease executions within the lab area are executed with purchasers that have already got earlier relationships with DOC, displaying simply how necessary scale, know-how and relationships are on this subject. This isn’t your commonplace healthcare, nursing house play – and I hope that comes by way of right here.

The aforementioned $60M upside comes from varied new high-quality developments throughout the corporate’s portfolio – Portside, Vantage, and Gateway particularly, with $20M of further merger synergies, bringing the entire to round $80M.

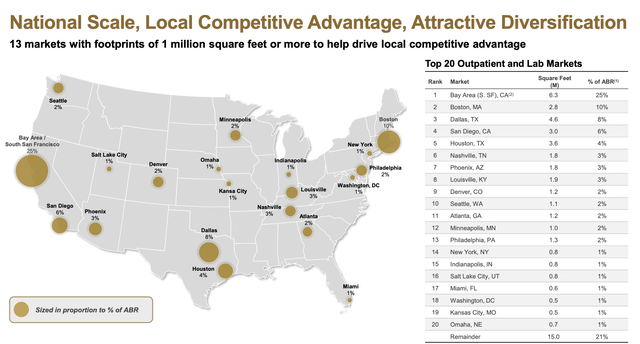

This additionally is not a very excessively concentrated REIT. Whereas some publicity exists to the SF/Bay space, this is not as scary as chances are you’ll suppose, given the quantity of buyer lab area on this space. I don’t at a positive outlook for California on the whole, however relating to this play, I take into account it an appropriate one.

DOC IR (DOC IR)

Merely put, what we’ve right here is $1.7B price of annualized base hire, or ABR, with the most important consumer being HCA Healthcare at 9%. Past that, the second-largest tenant is 3%, and after that, it is all 1% or under. So when it comes to diversification, loads of that right here.

The corporate has zero 2024 maturities. Even 2025E is lower than a billion. The corporate’s present liquidity is sufficient to cowl 2025, 2026 and virtually 2027 with no extra money wanted in any respect, and with a WAAR (weighted common rate of interest) of three.8%, it is a firm that has managed to maintain its debt very low.

Let’s take a look at the corporate’s valuation

The valuation for Healthpeak – the second compelling purpose for funding

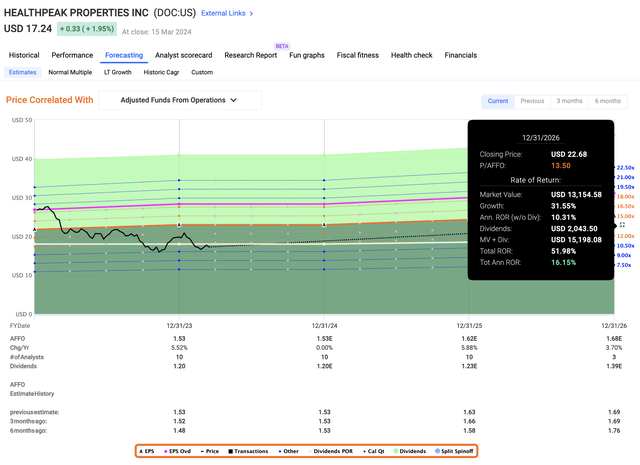

So, I hope I’ve proven you which you can take into account this firm a qualitative REIT with a gorgeous set of fundamentals, more likely to no less than be secure in its efficiency. When it comes to progress, DOC appears unlikely, as I see it, to generate any vital AFFO progress this yr. The midpoint within the estimate is $1.53 presently, and that’s primarily a progress of 0% presently.

Due to that, the share has taken an honest quantity of punishment and is presently hovering at 11x P/AFFO, which is sort of a low for a corporation that always has traded above 22-23x P/AFFO (Supply: FactSet).

From this time ahead, we may give the corporate a myriad of various estimates and expectations – however let’s begin on the low finish – let’s assume you are giving not more than a 13-14x P/AFFO. That may symbolize an over 10-25% low cost relying on what interval you have a look at, however sometimes this firm has commanded near 20x P/AFFO. Even on the longest-term estimate primarily based on historic numbers, you are solely discovering 16.5x P/AFFO – and again then, the corporate had a considerably completely different asset profile and purpose.

So once you say that you really want 13.5x P/AFFO as an estimate, you are going in at a really discounted price.

Healthpeak Upside (F.A.S.T graphs)

However even at that price, you are getting greater than 15% annualized. You possibly can the truth is go as little as 9x P/AFFO, and also you’d nonetheless come out with out shedding cash primarily based on a 3.4% annualized AFFO progress price till 2026.

Are you beginning to see the image?

In order that’s a base/bearish case – although I might nonetheless argue it is a very bearish case at 13.5x. But when we transfer to the opposite facet of the equation, we’re as an alternative forecasting a 10-year common of 17x P/AFFO. That is under the insane 22x+ ranges we noticed some yr or two in the past, however nonetheless at a valuation that I consider displays the underlying high quality of the property right here, in addition to the slight 3-4% annualized price of progress.

At 17x, you are getting 25% per yr inclusive of dividends, or 86% in ~3 years.

How seemingly is DOC to succeed in these targets?

Properly, the corporate doesn’t, ever, negatively miss estimates on a 1-year ahead foundation even with a ten% margin of error. The corporate both beats them – 25% of the time – or hits them. (Supply: FactSet)

Primarily based on this, I give Healthpeak a high-conviction “BUY” and present you why this 7%-yielding healthcare REIT is a big place in my portfolio, about 1% in private and business, and why I’ve added extra shares in the previous couple of weeks as the corporate dropped even additional.

I am additionally not at capability however might add extra as nicely.

I consider you may take into account the identical should you really feel that the corporate sits your funding profile.

My thesis for this firm is as follows.

Thesis

Healthpeak is without doubt one of the higher healthcare REITs on the market. Its portfolio is sound, its fundamentals are secure, the yield is extraordinarily well-covered, and the corporate has a gorgeous future prospect primarily based on each stability and slight progress of its prospects. The subsequent few years shall be powerful for REITs within the area, however I consider that PEAK shall be one of many REITs that survive and thrive.

Primarily based on this, I take into account this firm a gorgeous “BUY” at a great value, the place we will see a conservative double-digit upside. Ever since promoting off its senior portfolio, the corporate’s earnings capability has been declining from 2015 ranges – however it’s stabilizing, and I see a possible for progress within the subsequent few years.

I give the corporate a conservative P/FFO of no less than 15-17x, implying a long-term PT of $27/share, and an upside of no less than 15% right here. I preserve this as of this text.

PEAK is a “BUY” and a great one.

Bear in mind, I am all about:

1. Shopping for undervalued – even when that undervaluation is slight, and never mind-numbingly large – corporations at a reduction, permitting them to normalize over time and harvesting capital positive factors and dividends within the meantime.

2. If the corporate goes nicely past normalization and goes into overvaluation, I harvest positive factors and rotate my place into different undervalued shares, repeating #1.

3. If the corporate does not go into overvaluation, however hovers inside a good worth, or goes again right down to undervaluation, I purchase extra as time permits.

4. I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed here are my standards and the way the corporate fulfills them (italicized).

This firm is general qualitative.

This firm is essentially secure/conservative & well-run.

This firm pays a well-covered dividend.

This firm is presently low-cost.

This firm has a sensible upside primarily based on earnings progress or a number of enlargement/reversion.

Because of this the corporate fulfills each single one in every of my standards, now additionally being low-cost.

[ad_2]

Source link