[ad_1]

Fed begins injury controlFederal Reserve officers have hit the talking circuit for the primary time since Chair Powell’s dovish look in his post-FOMC assembly press briefing final week, in what appeared to be an try to steer markets away from aggressive charge lower expectations. New York and Atlanta Fed presidents, John Williams and Raphael Bostic, have been out in drive on Friday, pushing again towards bets of an early charge lower.

Williams instructed CNBC, “We aren’t actually speaking about charge cuts”, whereas talking in a radio interview, Bostic dominated out a charge lower earlier than the third quarter of 2024. Chicago Fed chief Austan Goolsbee who additionally spoke on Friday, was extra open to the opportunity of a lower as early as March. However Williams’ feedback got here throughout as extra deliberate and have been probably endorsed by Powell.

After sparking a market euphoria on Wednesday, sending out his high lieutenant may have been Powell’s approach of conducting some injury management. The issue is, having already added gasoline to the hearth, it’d require much more to include this irrational exuberance by buyers.

Markets hear however don’t take noteTreasury yields briefly jumped increased on Friday on the again of Williams’ remarks, boosting the US greenback, whereas shares on Wall Road dipped. However the strikes have been comparatively modest, and it didn’t take lengthy for them to be reversed. The 2-year yield appears to have reacted way more than the 10-year yield, which is sliding once more right this moment.

That is probably a sign that buyers are assured that inflation will quickly attain 2% and keep there and subsequently proceed to cost in nearly 150 foundation factors of charge cuts in 2024. It’s potential that Powell’s dovish tackle the coverage outlook was geared toward bolstering optimism for a comfortable touchdown. However markets didn’t actually need a serving to hand in that regard so will probably be attention-grabbing to see whether or not there will probably be extra backtracking within the coming days.

For now, although, there’s little signal of an imminent market correction and US inventory futures are marginally increased on Monday after modest positive aspects for the Dow Jones and Nasdaq on Friday, and a flat shut for the S&P 500.

In Europe, shares have had a blended begin to the final full buying and selling week of the 12 months earlier than Christmas as ECB policymakers have joined their Fed friends in pushing again towards early charge cuts.

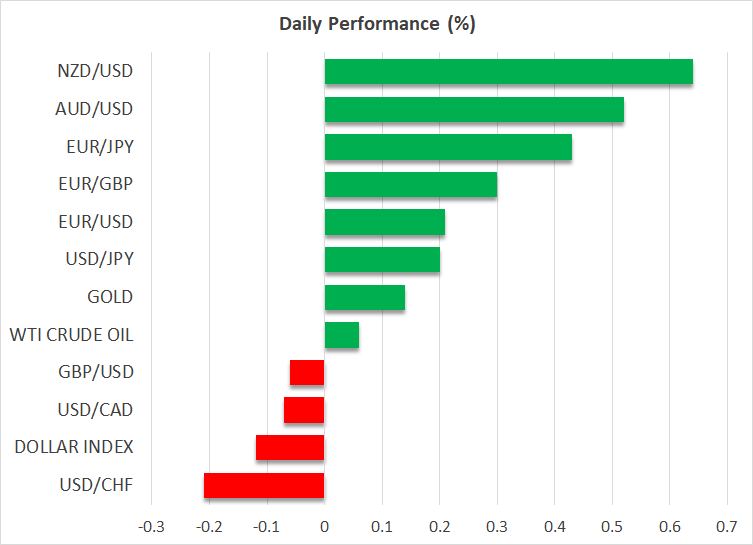

Euro boosted by hawkish ECB discuss, yen edges decrease forward of BoJHawkish remarks from the ECB’s Nagel and Muller earlier right this moment have lifted the euro, which is recouping a few of Friday’s steep losses. The Australian and New Zealand {dollars} are extending their bullish streak, climbing to close five-month highs versus their US counterpart amid renewed hopes that China will pump extra stimulus into its flagging financial system.

The yen bucked the development, nevertheless, softening to round 142.40 to the greenback throughout European buying and selling. After loads of hypothesis a couple of shock charge hike by the Financial institution of Japan in December, most bets now appear to be settling in the direction of an April liftoff, placing some draw back stress on the yen.

Now that bond yields are now not surging and the greenback’s rampage is over, the Financial institution of Japan can afford to attend. Governor Ueda has repeatedly hinted that the result of subsequent 12 months’s spring wage negotiations will probably be essential to any resolution on exiting unfavorable charges so no change in coverage is the probably end result of the BoJ announcement early on Tuesday.

The opposite large danger for the markets this week is the core PCE worth index out of the USA on Friday.

[ad_2]

Source link