[ad_1]

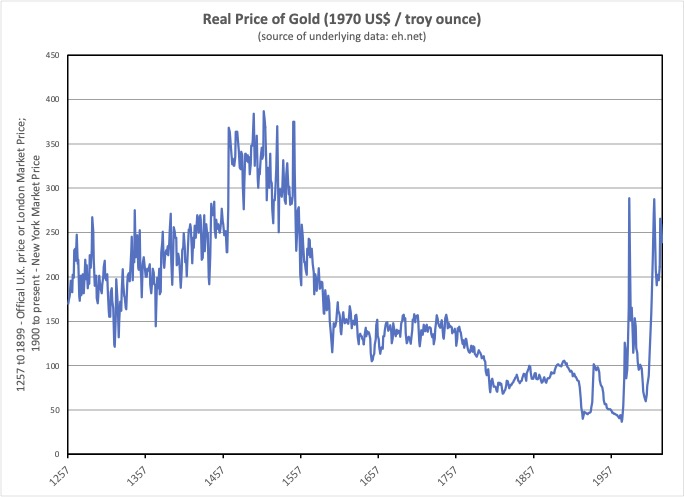

Gold is taken into account by many to be both an inflation hedge or an all-risk hedge. But, historical past — latest and long-term — exhibits that the true worth of gold has fluctuated considerably, even violently in latest instances. Right here I present the true worth of gold (the cash worth of gold divided by a shopper worth index).

Previous to the invention of the New World (and that the indigenous folks of this hemisphere didn’t have weapons), the true worth of gold was steadily rising. This would possibly mirror that in between discoveries of gold, its actual worth tended to extend. Then, with the cargo to Europe of gold and silver from the New World, the true costs of those metals fell. This phenomenon is known as the Worth Revolution by historians.

Following the Worth Revolution, the true worth of gold was steady for a few hundred years. Then, throughout the 18th Century, the true worth of gold began falling once more. This era, throughout which the true worth of gold fell from about 150 to about one hundred pc of its 1970 worth, has no particular identify. My guess as to the underlying reason for this decline in the true worth of gold was the expansion of fractional reserve banks, beginning with the Financial institution of Amsterdam. Fractional reserve banks enabled a roughly fixed provide of gold and/or silver to be multiplied into a bigger provide of cash.

Starting within the twentieth Century, following my shift of reference from London to New York, we see violent swings in the true worth of gold. The primary swing considerations the outbreak of WWI, and the suspension of the gold customary in Europe. The suspension of the gold customary in Europe resulted in gold flowing to New York, rising the availability of gold within the US, and driving down its actual worth.

The actual worth of gold recovered throughout the late Nineteen Twenties upon resumption of the gold customary in Europe. Because the US was then on a gold customary, this rise in the true worth of gold was related to deflation of shopper costs, waves of financial institution failures, and the Nice Melancholy.

Following WWII and the Bretton Woods Settlement, the true worth of gold fell once more. The Bretton Woods Settlement could be described as a gold change customary. Solely the US greenback was straight tied to gold. Different currencies had been tied to gold not directly, by being mounted of their change charges to the US greenback. This settlement allowed an enlargement of the worldwide cash provide enough to keep away from a post-war deflation.

In 1971, with the US embarking on a path of deficit spending, the Bretton Woods Settlement broke down. With the breakdown of the Bretton Woods Settlement, the US greenback “floated” in opposition to gold, which means that its worth sank in opposition to gold. The nation then moved just like the Titanic from iceberg to iceberg, in a bewildering sequence of ever worse cycles of inflation and recession. Then, Paul Volker got here in and, at the price of a extreme recession, guided the Federal Reserve to a path of “non-inflationary financial development.”

Because the above chart exhibits, throughout the years instantly following the breakdown of the Bretton Woods Settlement, the true worth of gold reached a degree not seen because the Worth Revolution. The demand for gold was fueled by ongoing inflation and fears of its acceleration. However, with the adoption of “non-inflation financial development” by the Fed, these fears weren’t realized, and the true worth of gold collapsed.

Lately, a brand new supply of uncertainty has been driving up demand for gold, and its actual worth. In 2020, the Trump Administration requested Congress for trillions of {dollars} to gradual the unfold of COVID. Since then, the Biden Administration has adopted go well with with further trillions of {dollars} of deficit spending.

Once more the true worth of gold has risen to historic highs. The worry fueling this enhance within the demand for gold is that the “unsinkable” ship of state has been so compromised by debt that it now dangers slipping below the waves.

One attainable prospect is for the US to undergo a long time of excessive charges of inflation resembling characterised Argentina below Juan and Eva Peron and their successors.

One other attainable prospect is for a crescendo of hyperinflation to completely destroy the center class and set the stage for a dictator resembling occurred in Germany throughout the Nineteen Twenties.

With such potentialities, wouldn’t it’s prudent to have some gold cash that you can sew into the liner of your coat, for when you need to make your escape?

I’ll shut with a narrative. As a highschool scholar a few years in the past, I attended a nationwide conference of younger conservatives the place I met an previous woman. She mentioned she was a youth in Russia on the time of the communist revolution there, however was lucky to flee, going to Cuba. Then, as a mature grownup, there was a communist revolution in Cuba. Once more she was lucky, this time escaping to the US.

“You in America,” she mentioned, “is not going to be lucky. As a result of the place are you able to go?”

Clifford F. Thies

Clifford F. Thies is a Professor of Economics and Finance at Shenandoah College, He’s the writer, co-author, contributor and editor of greater than 100 books, encyclopedia entries and articles in scholarly journals.

He’s a member of the editorial board of the Journal of Non-public Enterprise and is a former Bradley Resident Scholar on the Heritage Basis. He’s a previous president of the college senates of Shenandoah College and the College of Baltimore. He additionally served within the U.S. Military and the Military Reserve.

[ad_2]

Source link