[ad_1]

Up to date on January twenty seventh, 2024

Buyers searching for high-quality dividend development shares ought to take a better have a look at the Dividend Aristocrats, a gaggle of 68 corporations within the S&P 500 Index with 25+ consecutive years of dividend will increase.

With this in thoughts, we created a listing of all of the Dividend Aristocrats.

You may obtain the total spreadsheet of all 68 Dividend Aristocrats, together with a number of vital monetary metrics comparable to dividend yields and price-to-earnings ratios, by clicking on the hyperlink under:

Disclaimer: Certain Dividend shouldn’t be affiliated with S&P International in any means. S&P International owns and maintains The Dividend Aristocrats Index. The data on this article and downloadable spreadsheet relies on Certain Dividend’s personal overview, abstract, and evaluation of the S&P 500 Dividend Aristocrats ETF (NOBL) and different sources, and is supposed to assist particular person traders higher perceive this ETF and the index upon which it’s based mostly. Not one of the data on this article or spreadsheet is official knowledge from S&P International. Seek the advice of S&P International for official data.

We overview every of the Dividend Aristocrats yearly, and the following inventory on this 12 months’s version is client merchandise large Kimberly-Clark (KMB).

Kimberly-Clark has raised its dividend for 52 consecutive years. It is usually a member of the much more unique Dividend Kings record.

The inventory additionally at present has a 4% dividend yield, which is greater than double the ~1.6% common dividend yield of the S&P 500 Index.

This text will focus on Kimberly-Clark’s enterprise mannequin, development potential, and whether or not the inventory is at present buying and selling at a pretty valuation.

Enterprise Overview

Kimberly-Clark traces its beginnings again to 1872. 4 younger businessmen, John A. Kimberly, Havilah Babcock, Charles B. Clark, and Frank C. Shattuck, got here up with $30,000 of start-up capital to kind Kimberly, Clark and Co.

As we speak, Kimberly-Clark is a world client merchandise firm that operates in 175 international locations and sells disposable client items, together with paper towels, diapers, and tissues.

It operates by way of two segments that every home many well-liked manufacturers: Private Care Phase (Huggies, Pull-Ups, Kotex, Rely, Poise) and the Shopper Tissue section (Kleenex, Scott, Cottonelle, and Viva), producing over $20 billion in annual income.

Supply: Investor Presentation

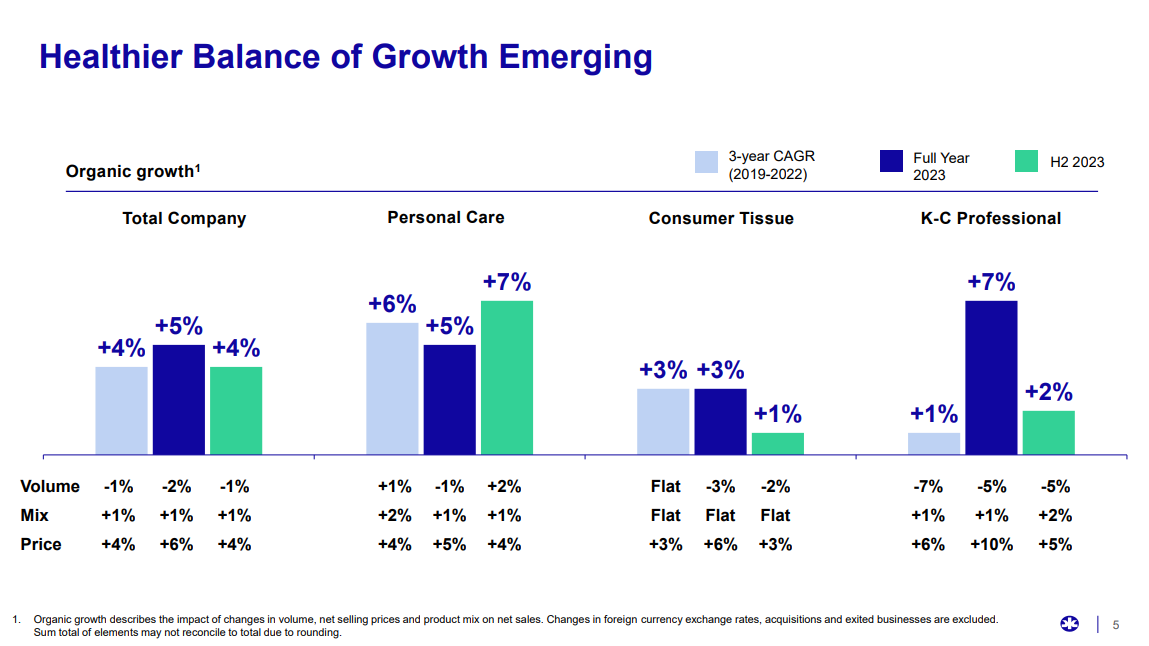

Kimberly-Clark posted fourth quarter and full-year earnings on January twenty fourth, 2024. Adjusted earnings-per-share got here to $1.51, which was three cents gentle of estimates. Income was flat year-over-year at $4.97 billion. Natural gross sales had been up 3% in the course of the quarter, attributable to a 2% achieve in pricing and a 1% tailwind from favorable product combine.

Development Prospects

Kimberly-Clark has dedicated to elevating its core manufacturers as one of many three pillars of development within the coming years. It’ll do that by launching totally different product improvements through extensions of current traces and completely new merchandise. The corporate can even proceed to handle its income through pricing and blend in addition to promotional methods.

The second development pillar is accelerating development in its growing and rising (D&E) markets, which comprise a good portion of the corporate’s gross sales.

KMB will give attention to its private care {and professional} segments particularly, with its most vital alternatives coming from locations the place it has low class penetration and frequency of utilization.

Kimberly-Clark additionally continues to pursue value financial savings. Kimberly-Clark’s administration group has repeatedly prolonged this initiative, aiming for one more $1.5 billion of cumulative financial savings over a three-year interval.

We count on 5% annual earnings development within the years to come back, as we count on volumes to stay largely regular.

Aggressive Benefits & Recession Efficiency

Kimberly-Clark’s most vital aggressive benefits are its manufacturers and world scale. The corporate enjoys a management place throughout its model portfolio and, certainly, the world over.

It retains its aggressive benefits by way of advertising and innovation. This enables the corporate to remain forward of the competitors. Given its dedication to its development pillars, we count on this can solely enhance over time.

As well as, Kimberly-Clark’s world attain supplies the corporate with the effectivity to maintain prices low. The continuing value discount program is an instance of its means to successfully handle prices, at the same time as income grows.

Kimberly-Clark stays extremely worthwhile, even throughout recessions. For instance, it carried out properly by way of the Nice Recession of 2007-2009. Its earnings-per-share by way of the Nice Recession are proven under:

2007 earnings-per-share of $4.25

2008 earnings-per-share of $4.06 (4.5% decline)

2009 earnings-per-share of $4.52 (11% enhance)

2010 earnings-per-share of $4.45 (1.5% decline)

As you’ll be able to see, whereas Kimberly-Clark did see earnings decline in 2008 and 2010, it additionally registered a double-digit development fee in 2009. The explanation for its sturdy efficiency over the course of the recession is that the corporate sells merchandise that customers want no matter financial situations.

Customers will all the time want private care merchandise, whatever the situation of the financial system. This provides Kimberly-Clark a sure stage of product demand every year, even throughout recessions.

Valuation & Anticipated Returns

Primarily based on adjusted earnings-per-share of $6.85 for 2024, Kimberly-Clark trades for a price-to-earnings ratio of 17.7.

Excluding outlier years, Kimberly-Clark has traded at a mean price-to-earnings ratio of ~18 over the past decade. That is additionally our estimate of honest worth for the inventory. Subsequently, shares seem like barely undervalued proper now.

If the inventory valuation expands from 17.7 to 18 over the following 5 years, it should enhance annual returns by 0.3% per 12 months.

As well as, future returns can be generated from earnings development and dividends. Given the corporate’s sturdy manufacturers and development catalysts, common annual earnings development of 5% is an affordable expectation. The inventory additionally has a 4.0% dividend yield.

In complete, we see annual returns of 9.3% over the following 5 years. It is a strong anticipated fee of return, however is just under our purchase threshold of 10%.

Ultimate Ideas

Kimberly-Clark is a high-quality firm with a various portfolio of sturdy manufacturers. It has constructive development prospects shifting ahead, and it’s an especially dependable dividend inventory. Rising markets, value reductions, and share repurchases will spotlight future earnings development.

Kimberly-Clark has elevated its dividend for over 50 years in a row and at present has a dividend yield of 4%. It, due to this fact, meets our definition of a blue-chip inventory, and it ought to proceed to ship regular dividend will increase every year.

In case you are excited about discovering extra high-quality dividend development shares appropriate for long-term funding, the next Certain Dividend databases can be helpful:

The key home inventory market indices are one other strong useful resource for locating funding concepts. Certain Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to help@suredividend.com.

[ad_2]

Source link