[ad_1]

Revealed by Bob Ciura on November 14th, 2023

The Dividend Kings are an illustrious group of firms. These firms stand aside from the overwhelming majority of the market as they’ve raised dividends for not less than 50 consecutive years.

We imagine that buyers ought to view the Dividend Kings as probably the most high-quality dividend progress shares to purchase for the long run.

With this in thoughts, we created a full checklist of all of the Dividend Kings. You possibly can obtain the complete checklist, together with vital monetary metrics resembling dividend yields and price-to-earnings ratios, by clicking the hyperlink under:

This group is so unique that there are simply 53 firms that qualify as a Dividend King. United Bankshares (UBSI) just lately elevated its dividend for the fiftieth consecutive 12 months, becoming a member of the checklist of Dividend Kings.

This text will focus on the corporate’s enterprise overview, progress prospects, aggressive benefits, and anticipated returns.

Enterprise Overview

United Bankshares was shaped in 1982 and since that point, has acquired greater than 30 separate banking establishments. This concentrate on acquisitions, along with natural progress, has allowed United to broaden right into a regional powerhouse within the Mid-Atlantic with about $29 billion in whole property, and annual income of about $1 billion.

United posted third quarter earnings on October twenty fifth, 2023, and outcomes had been considerably weaker than anticipated. Earnings-per-share got here to 71 cents. Income was $262 million, off 4.1% year-over-year. Internet curiosity revenue was up $992 thousand, or lower than 1%, from this 12 months’s Q2.

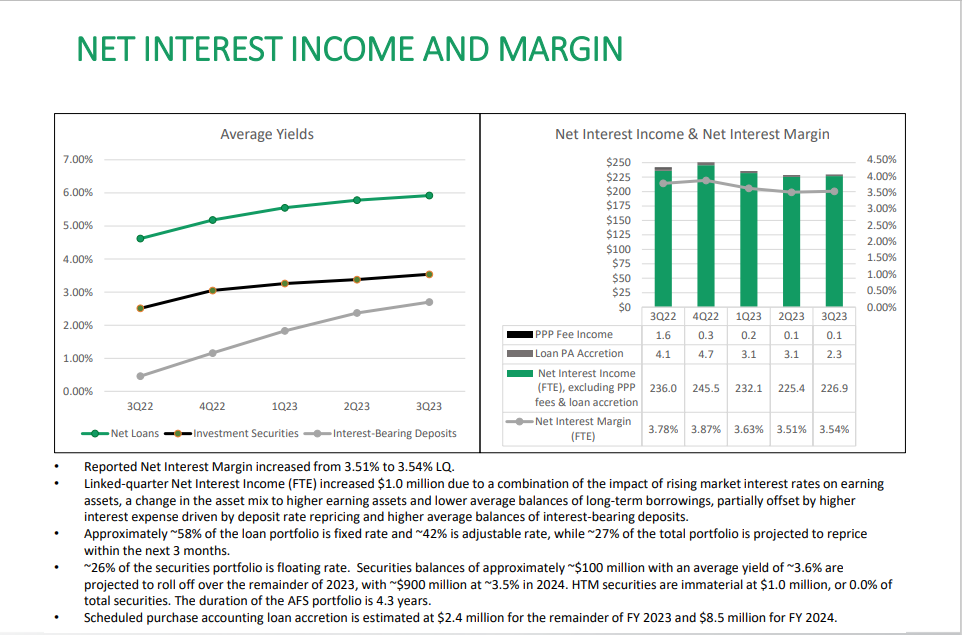

Supply: Investor Presentation

Q3 outcomes benefited from rising market rates of interest on incomes property, a change within the asset combine to increased incomes property, and decrease common balances of long-term borrowings. This was partially offset by increased curiosity expense, which was pushed by the affect of deposit charge balances.

The yield on common incomes property rose 19 foundation factors to five.52%. Internet curiosity margin of three.54% was a rise of three foundation factors from Q2. Provisions for credit score losses had been $5.9 million, down from $11.4 million for Q2. The decrease quantity of provisions had been resulting from changes on assumptions of future macroeconomic circumstances, partially offset by further bills accrued resulting from mortgage progress.

Progress Prospects

Earnings-per-share have been flat for just a few years now, as the corporate has struggled with translating asset and mortgage progress into income. We now see -2% annual earnings progress. We be aware the comparatively excessive base in earnings for 2023 as making future progress more difficult.

United has at all times grown via acquisition, and we don’t imagine that can change. Nonetheless, its internet curiosity margin goes to be in danger within the coming quarters because the fast decline in charges in 2020 produced an enormous decline in the price of funds. Charges moved favorably for banks in 2021, and moved sharply increased in 2022.

Assuming charges stay elevated, United will probably be topic to probably a lot increased funding prices, which can see its NIM deteriorate if it can not produce commensurate positive factors in lending yields. Lending margins rose fractionally in Q3, which is a constructive flip from Q2 outcomes.

Aggressive Benefits & Recession Efficiency

United’s aggressive benefit is in its robust market place within the areas it serves. It’s headquartered in West Virginia the place competitors is comparatively gentle, and it’s increasing into extra densely populated areas like northern Virginia.

That doesn’t make it immune from recessions, however its efficiency in 2008 and 2009 was exemplary, and held up in very difficult circumstances in 2020, and thrived in 2021.

Beneath are the corporate’s earnings-per-share outcomes throughout, and after, the Nice Recession:

2007 earnings-per-share: $1.32

2008 earnings-per-share: $1.52 (15% enhance)

2009 earnings-per-share: $1.51 (~1% lower)

2010 earnings-per-share: $1.81 (20% enhance)

The corporate grew its diluted earnings-per-share in 2008, adopted by only a minor decline in 2009, which was the worst of the recession. Fortis then rapidly rebounded with 20% earnings progress in 2010.

Valuation & Anticipated Complete Returns

We count on United Bankshares to generate earnings-per-share of $2.80 for 2023. On the present share value, UBSI inventory trades for a price-to-earnings ratio of 11.9.

We see honest worth at 12 occasions earnings, given the place peer valuations are at current. We see elevated threat for United given the comparatively weak efficiency traditionally of the corporate’s internet curiosity margin and we predict buyers can pay barely much less for the inventory in consequence. Shares are barely undervalued in the intervening time.

An increasing P/E a number of may increase annual returns by 0.2% over the subsequent 5 years. Dividends may even increase shareholder returns. UBSI inventory yields 4.5% proper now.

These returns will probably be offset by anticipated EPS decline of two% per 12 months via 2028. Due to this fact, UBSI is predicted to return 2.7% yearly via 2028. It is a comparatively weak anticipated charge of return, making UBSI inventory a maintain.

Last Ideas

United is now anticipated to provide 2.7% annual returns within the coming years. The yield is engaging at 4.5% and may stay secure for years to return, so United could possibly be value a search for revenue buyers.

Shares earn a maintain ranking as we see the street forward being very robust from a progress perspective for quite a lot of causes, however the inventory is affordable and has a sexy yield.

The next articles comprise shares with very lengthy dividend or company histories, ripe for choice for dividend progress buyers:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to help@suredividend.com.

[ad_2]

Source link