[ad_1]

Eloi_Omella

Funding Rundown

The inexperienced power area is quickly rising and I believe having some sort of publicity to the sector and business is essential for a well-diversified portfolio. With Enlight Renewable Vitality Ltd (NASDAQ:ENLT) you might be getting a quickly rising enterprise benefiting from precisely a majority of these tailwinds. The corporate had its IPO this yr and the share worth has roughly come again to the identical stage after being on fairly a rollercoaster since February. One of many many positives of ENLT in comparison with different firms within the area is that they’re already worthwhile with a TTM internet revenue of $66 million, up from $11.2 million in 2021. With the manufacturing and enterprise scaling up quickly the premium it has in opposition to the sector appears justified as in a short while I believe it could actually develop into it.

By 2026 the estimates are the ENLT will attain an annual EPS of $3.57 which places them proper now at an FWD p/e of 4.8. With the utility sector buying and selling at a p/e of 16, I believe ENLT is an thrilling guess proper now. What buyers must account for is a few answer over the approaching years and seeing as ENLT had its IPO this yr in February, by subsequent yr I believe the lock-up interval might reveal some vital promoting potential as early buyers will need to get out, which is sort of widespread in loads of enterprise. This might weigh on the inventory worth within the brief time period however in my opinion isn’t one thing that deters me sufficient to price ENLT something decrease than a purchase.

Firm Segments

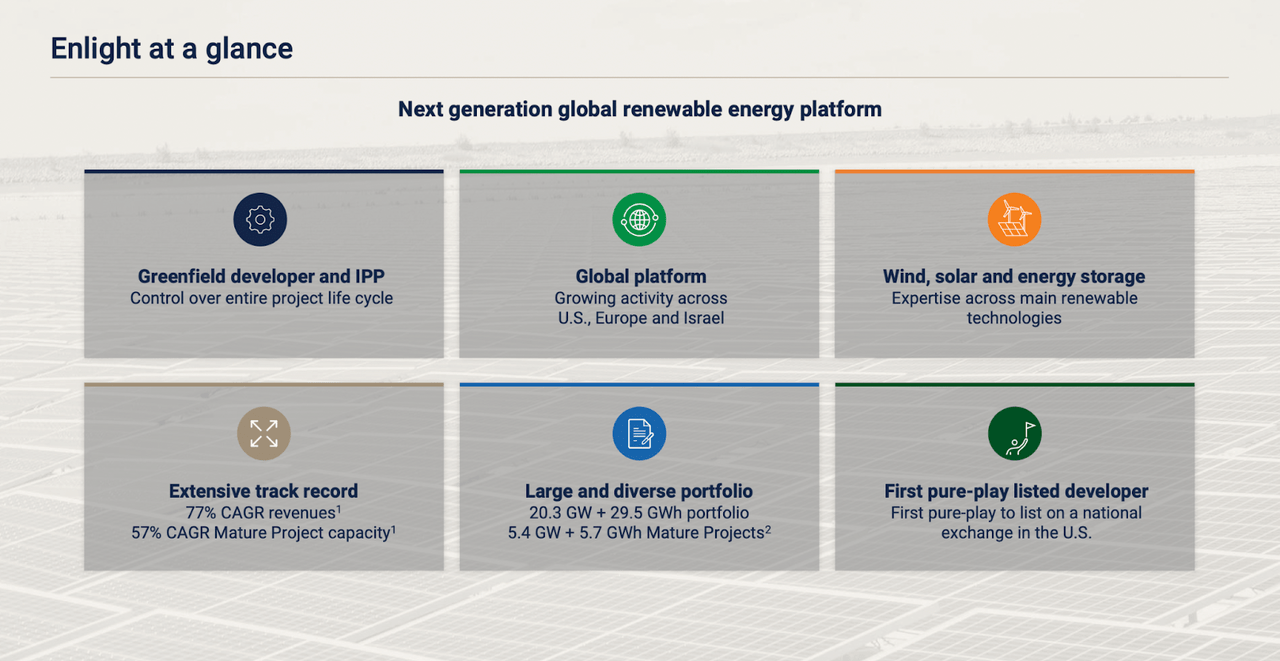

ENLT capabilities as a distinguished renewable power platform, each inside Israel and on the worldwide stage. The corporate is actively concerned in all the lifecycle of renewable power tasks—from initiation and planning to growth, building, and operation. Its portfolio encompasses a various vary of tasks centered on harnessing electrical energy from renewable sources, together with wind and photo voltaic power. Moreover, ENLT is engaged within the growth of power storage tasks to boost effectivity and sustainability within the quickly evolving renewable power panorama.

Overview (Investor Presentation)

The renewable power area is poised for vital development within the coming years, pushed by varied elements. There’s a world shift in the direction of cleaner and sustainable power options, spurred by rising consciousness of local weather change and environmental issues. Governments worldwide are implementing insurance policies and incentives to encourage the adoption of renewable power sources, contributing to the sector’s growth. Ongoing technological developments play an important position in enhancing the effectivity and cost-effectiveness of renewable programs. Photo voltaic and wind power, particularly, have develop into more and more aggressive with conventional fossil fuels, due to declining prices.

Progress Numbers (Looking for Alpha)

The expansion for ENLT over the previous few years has been superb and I believe it should proceed that approach as nicely for the foreseeable future. There are such a lot of investments going into this area and I believe ENLT will not discover it too troublesome to search out clients. ENLT engages it in rewarding tasks which have helped it develop a portfolio to almost 50GWh already leading to a 77% CAGR of revenues.

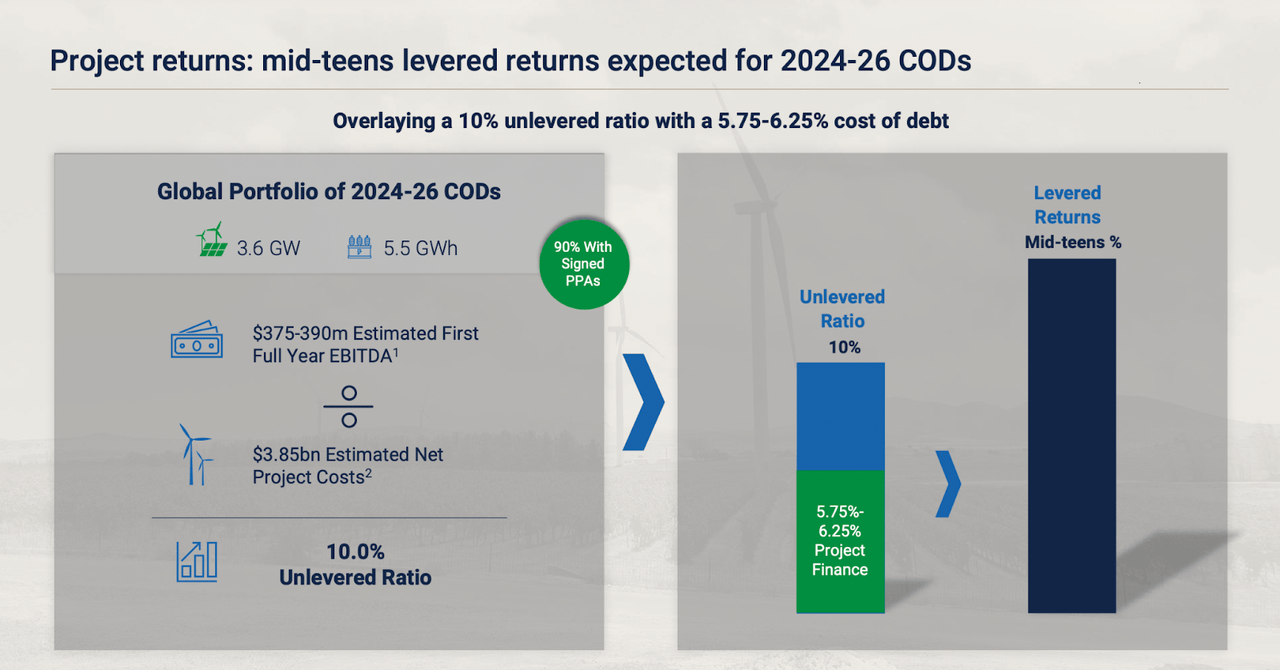

Undertaking Returns (Investor Presentation)

The corporate manages roughly 17.0 gigawatts of energy era tasks and possesses 15.3 gigawatt-hours of power storage capability, highlighting its substantial presence within the business. As of September 30, 2022, Enlight has secured vital investments amounting to a good market worth of $765 million in fairness. Notable contributors to those investments embody key monetary entities akin to Migdal Insurance coverage and Monetary Holdings, Harel Insurance coverage Investments & Monetary Providers, and Clal Insurance coverage Enterprises Holdings. With robust institutional investments, I believe the backing for ENLT proper now could be robust and can help them in additional increasing their portfolio right into a extra mature state.

Earnings Highlights

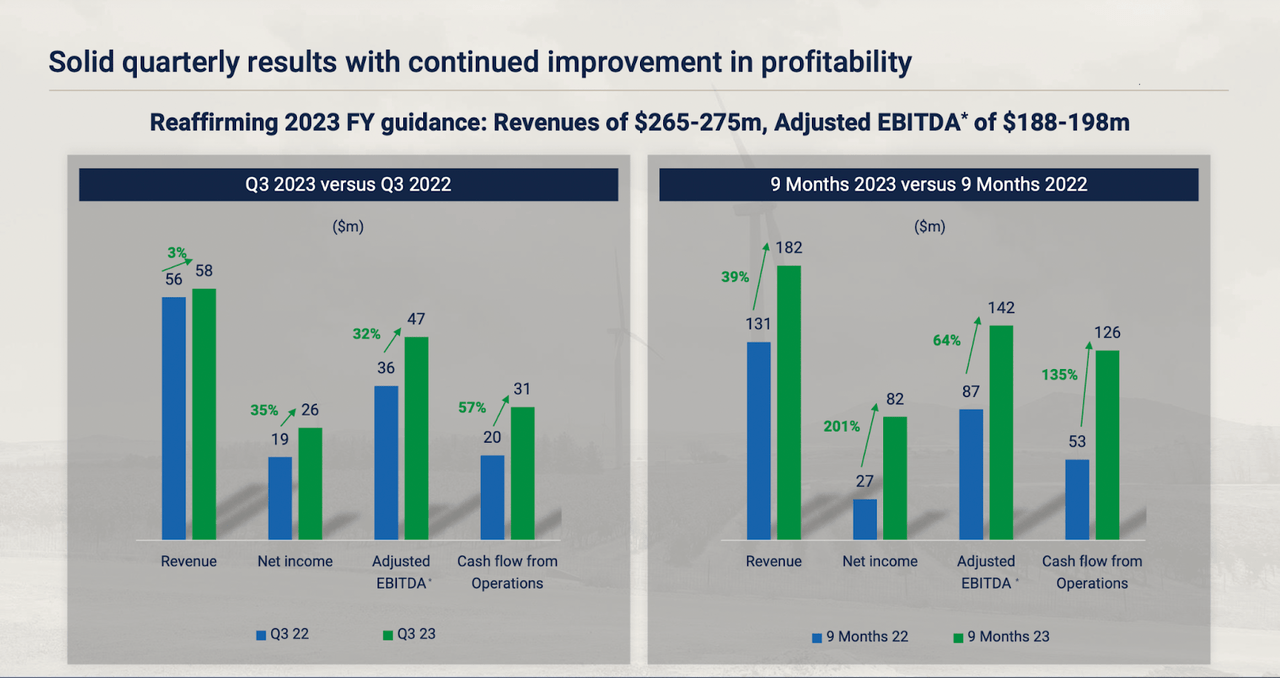

The final quarter for the corporate showcased robust outcomes because the administration reaffirmed the steerage set for 2023. One of many constructive traits that occurred final quarter although was the spectacular margin growth. While the revenues maybe did not present as robust development numbers as one would have hoped, simply up 3% YoY, the web revenue grew by 35% YoY. This shift was a lot because of the decline of commodities prices which made the tasks and merchandise the corporate makes much more worthwhile and cheaper.

Quarterly Outcomes (Investor Presentation)

As I discussed, the steerage for 2023 was reaffirmed at revenues of $265 – $275 million and adjusted EBITDA of $188 – $189 million. This places ENLT at an FWD p/s of seven.3 and an FWD p/e GAAP of 25. A number of the undertaking updates for ENLT have been very constructive in Q3. The definitive documentation was finalized for tasks in each the US and Israel with each transactions amounting to over $500 million. This has led the administration to count on round $300 million extra extra fairness to be returned to the corporate.

Market Overview (Investor Presentation)

I believe that the event the corporate has had within the US is likely one of the most essential. Seeing because the revenues from there are usually not that top and Western Europe being the very best means they’ve entry to an enormous market alternative nonetheless. The market measurement right here is over $269 billion which I definitely need to see ENLT transfer extra aggressively into within the coming decade.

Dangers

Contemplating the corporate’s location in Israel, the present geopolitical scenario provides a component of danger to its share worth. The continuing battle within the area places stress on the corporate’s infrastructure. Regardless of being within the renewable power sector with a strong status, the impression of the battle might pose challenges. On a constructive word, given the societal significance of progress in renewable power, there’s potential for help to assist rebuilding efforts. Nevertheless, buyers should acknowledge the inherent danger related to the corporate’s location and take into account this issue of their funding selections.

Shares Excellent (Looking for Alpha)

A number of the dangers which might be dealing with buyers embody the story of share dilution that ENLT has. I believe those that search a extra steady and extra shareholder-focused enterprise might need to look elsewhere as a substitute. However I’ve a powerful conviction that in time ENLT will be capable of effectively remodel right into a dividend-distributing enterprise that may additionally afford to allocate capital to purchasing again shares too. I believe that ENLT is, nonetheless, rising its backside line rapidly sufficient that the dilution is not having such a adverse impact on the enterprise however moderately allows it to extra aggressively develop and construct a strong portfolio of tasks.

Closing Phrases

The renewable power area is a really thrilling one to be part of and I believe one of many higher choices proper now could be ENLT. The corporate is working in a dangerous atmosphere proper now seeing because the battle in Israel and Gaza has escalated quickly during the last a number of weeks. I believe nonetheless that the chance/reward with the enterprise remains to be too good to cross up on. ENLT has confirmed itself able to rapidly rising each the highest and backside line and will probably be a really strong funding over the subsequent decade and past.

[ad_2]

Source link