[ad_1]

Most Learn: Japanese Yen Outlook & Market Sentiment: USD/JPY, EUR/JPY, GBP/JPY

The Federal Reserve will launch its March financial coverage announcement on Wednesday. Consensus estimates overwhelmingly recommend that the establishment led by Jerome Powell will maintain its benchmark charge unchanged at its present 5.25% to five.50% vary, successfully sustaining the established order for the fifth consecutive assembly. Furthermore, analysts extensively anticipate that the central financial institution will hold its quantitative tightening program intact for now, persevering with to cut back its bond holdings regularly.

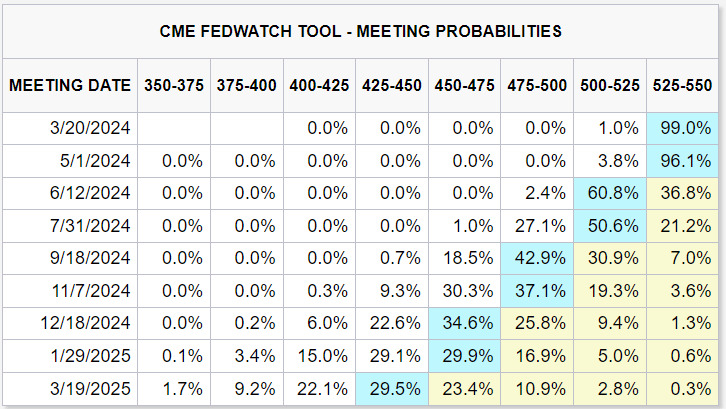

Whereas the choice on rates of interest themselves could not ship dramatic surprises, markets will probably be laser-focused on the ahead steerage. With that in thoughts, the FOMC could repeat that it doesn’t count on will probably be acceptable to cut back borrowing prices till it has gained larger confidence that inflation is converging sustainably towards 2 p.c – a transfer that might point out extra proof on disinflation is required earlier than pulling the set off. Present FOMC assembly possibilities are proven under.

Supply: CME Group

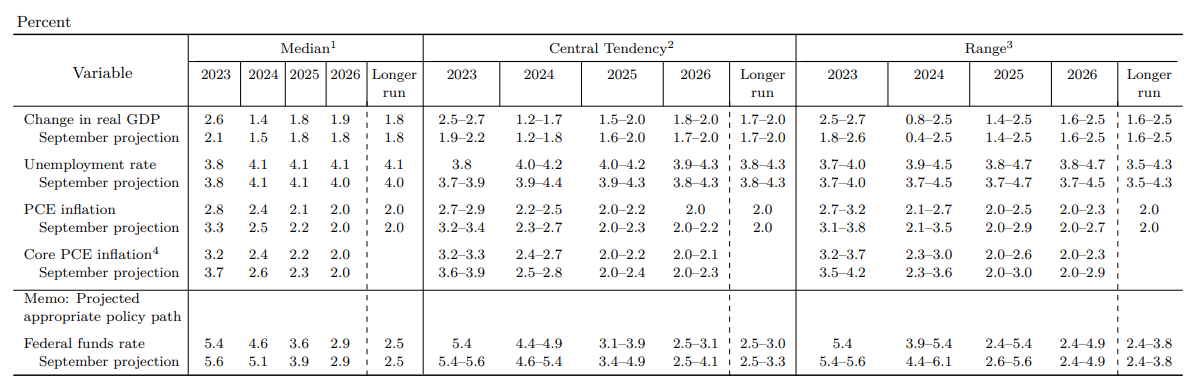

By way of macroeconomic projections, the Fed is prone to mark up its gross home product and core PCE deflator forecasts for the yr, reflecting financial resilience and sticky worth pressures evidenced by the final two CPI and PPI stories. The revised outlook might compel policymakers to sign much less financial coverage easing over the medium time period, probably scaling again the three charge cuts initially envisioned for 2024 to solely two (this data will probably be obtainable within the dot plot).

The next desk reveals projections from the December FOMC assembly.

For a whole overview of the U.S. greenback’s technical and basic outlook, seize a duplicate of our free quarterly forecast!

Really helpful by Diego Colman

Get Your Free USD Forecast

Supply: Federal Reserve

If the Federal Reserve alerts a larger inclination to train endurance earlier than eradicating coverage restraint and reveals much less willingness to ship a number of charge cuts, we might see U.S. Treasury yields and the U.S. greenback cost upwards within the close to time period, extending their current rebound. In the meantime, shares and gold, which have rallied strongly not too long ago on the idea that the central financial institution was on the cusp of pivoting to a looser stance, could possibly be in for a impolite awakening (bearish correction).

factor contained in the factor. That is in all probability not what you meant to do!

Load your software’s JavaScript bundle contained in the factor as an alternative.

[ad_2]

Source link

Add comment