[ad_1]

Inflation might not change that rapidly, however inflation expectations can change very abruptly — like this week, when a hotter-than-expected CPI quantity lastly pushed the market over the sting and satisfied buyers to cease anticipating a charge reduce in March, or 5+ charge cuts this yr. That comparatively small shift in sentiment, with the market already at a excessive valuation and with excessive progress expectations pushed by the AI mania, created big promoting strain as merchants pulled again rapidly after the lovable pet bit them on the hand. About the one inventory that might combat by to a “inexperienced” day on Wednesday was NVIDIA, which isn’t precisely an ideal signal.

Effective for NVIDIA, in fact, holy cow has that continued to climb — however most likely provides extra gas to the “that is like Cisco in 2000” arguments, and with each big leap increased for NVIDIA it turns into tougher and tougher to quiet the voice behind my head that claims, “this gained’t finish nicely.” (And I acted on that voice’s message somewhat bit… extra on that in a second.)

However then, whaddya know, by the subsequent day virtually all was forgiven, and the market was going up once more. Woe betide ye who tries to foretell the route of the market in any given week or month.

And we heard from fairly a number of of our firms this week… beginning with one which I bought a bit of final week, WESCO (WCC), and the market had a fairly wild response to that earnings report, so let’s have a look at that first.

I bought a portion of my WESCO (WCC) holdings final week as a result of I assumed the valuation was now not compelling, and it had fairly nicely confirmed my thesis appropriate over the previous three years, leading to a pleasant double. As I famous on the time, there have been each optimistic and pessimistic eventualities for the way it could play out for this inventory this yr, and I didn’t have plenty of confidence in guessing which was extra possible. They’re a distributor {of electrical} and communications gear, primarily, and people markets are anticipated to proceed to develop over the subsequent 5 years — so in concept, at the least, WESCO has a superb progress runway, spending on broadband and electrical infrastructure and enormous manufacturing tasks and information heart growth ought to proceed to go up, incentivized partly by the assorted authorities stimulus packages for extending broadband and re-shoring manufacturing, together with semiconductor manufacturing.

However as this quarter indicated, it doesn’t go up in a straight line — partly as a result of plenty of that funding has nonetheless not hit the top markets, and can be easing out of the federal government step by step over 5 years, and partly as a result of the remainder of the top markets will not be all booming. Maybe extra importantly, the provision chain chaos of the previous few years has lastly eased, and prospects can once more get “simply in time” shipments of virtually something they want all over the world, which implies they don’t must hoard provides or pay premium costs any longer, all of which benefitted WESCO by front-loading demand and elevating end-user costs (and due to this fact WESCO margins) by at the least somewhat bit through the 2020-2022 interval.

And a number of the new federal spending, on stuff like broadband growth, has been actually trickling out at this level. CFO David Schulz on this week’s convention name put it this fashion: “based mostly on buyer and provider enter, we don’t anticipate to see a restoration in broadband till late 2024 earlier than turning to progress in 2025.”

They’re nonetheless doing rational issues — their money move is enhancing, although not as rapidly final yr as they’d predicted, they’re getting concerned with huge tasks and prospects which can be protecting their backlog giant and fairly steady (although probably not rising, even though in addition they mentioned it “ticked up” in January), and they’re going to enhance the dividend by 10%, a superb signal as they enter their second yr as a dividend-paying firm.

And the inventory might be valued fairly rationally after this post-earnings drop, so the inventory is once more at ~10X ahead earnings estimates… it’s simply that these estimates got here down from $17 to under $15 this week, because of WESCO’s much-lower-than-expected steering — going from 12X $17 in anticipated earnings to 10X $15 in anticipated earnings means an enormous drop for the share worth, regardless that it was a “worth” inventory each earlier than and after the announcement.

2023 gross sales at WESCO ended up rising by 5%, however their gross margin fell and their working margin fell, and there’s no signal of an abrupt restoration being significantly possible. The fourth quarter was significantly gradual, with decrease gross sales of their regular stock objects in addition to delays in “sure tasks” (we’ve all seen that plenty of huge manufacturing and warehouse tasks have hit delays of late, together with the large semiconductor foundry tasks in Ohio and Arizona, however WESCO didn’t name out a selected mission).

They usually anticipate 2024 to convey progress on the highest line, however simply barely, the forecast is for slower progress than 2023 — they’re guiding buyers to anticipate 1-4% gross sales progress, so they’re both “guiding low” or they actually don’t see a surge in authorities spending hitting their prospects… or at the least, they don’t see it being excessive sufficient to offset slowing demand in different areas, like OEM and broadband and normal development.

So that they’ve been spending extra on SG&A (which is generally “folks”), they usually’re seeing their gross margins slip as suppliers supply fewer reductions and finish customers are extra worth acutely aware and fewer more likely to over-order or hoard provides. They did find yourself with $444 million in free money move final yr, which was in enchancment on previous years however decrease than the $600 anticipated… however most of it got here within the second half, and they’re predicting $600-800 million in free money move for 2024, which might imply {that a} LOT extra of their predicted earnings are actual money earnings — $700 million can be $13.72 per share in free money move, and WESCO’s adjusted earnings steering for 2024 is now that they are going to be in a spread of $13.75-15.75 per share. So that might imply “increased high quality” earnings in 2024 than they’d final yr… but additionally maybe decrease earnings.

The brief reply right here is that each the 2023 earnings and the 2024 earnings steering from WESCO got here in roughly 15% under what was anticipated by analysts, and point out that the adjusted earnings per share will most likely at greatest be flat over the approaching yr, and will decline for the second yr in a row. And that doesn’t assume any sort of actual big-picture financial slowdown or recession, in fact. There’s more likely to be a good quantity of skepticism from analysts about how successfully WESCO can predict their monetary leads to any given yr, since they got here in nicely in need of the steering they’d offered final Spring and Summer time. It is probably not cheap to guage them for being far off in predicting their gross sales, margins, earnings and free money move throughout a interval when these issues are fairly far off — however they nonetheless made the predictions, and included a fairly wide selection, and missed that vary fully.

It was reassuring to see that fairly particular outlook on the time, too, as I recall, so I don’t blame analysts for following that steering — it appeared cheap and rational, significantly after they reduce it in August, however right here’s how issues have gone for WESCO over the previous yr:

A yr in the past, in February of 2023, their 2023 outlook was: 6-9% gross sales progress, $600-800 million in free money move, $16.80-$18.30 in adjusted earnings per share. They repeated that steering in Could, gross sales progress was nice at that time, although money move wasn’t coming but they usually mentioned to anticipate that to be late within the yr, all was sunny and vibrant.

Six months in the past, in August, they downgraded the steering after a weak quarter — their new 2023 outlook was: 5-7% gross sales progress, $500-700 million free money move, $15-16 adjusted EPS. Unhealthy information with the large drop, however nonetheless strong numbers for what was then a $170-180 inventory (~12X earnings, nonetheless anticipating to develop earnings for the yr).

November introduced reassurance with the third quarter outcomes, with good free money move era (a lot of the money they generated in 2023 got here in that quarter), and a few buybacks and speak about optionality and powerful execution, together with cost-cutting and enhancing margins. The precise quarterly earnings had been flat with the year-ago quarter, they usually did warn that October gross sales had been beginning out gradual, however they RAISED the steering — gross sales progress would are available in at 5% for the yr, they mentioned, not the 5-7% beforehand guided, however they caught with $500-700 million in free money move they usually raised the earnings forecast, to $15.60-16.10. Analysts obliged by placing their forecasts close to the highest finish of that steering vary, at about $15.90, as you’d anticipate. Analysts virtually at all times do as they’re advised.

And after what will need to have been an unpleasant finish to the yr for them, gross sales progress for the yr ended up being solely about 3%, free money move ended up at $444 million and the precise earnings per share got here in at $14.60.

In order that’s the problem, actually — do we now have any belief of their earnings steering, or of their skill to manage their margins or their prices in an unsure gross sales surroundings, given their way-too-optimistic forecasts over the previous yr, together with that “steering increase” simply three months in the past, in November?

They actually acknowledge the challenges, and talked rather a lot about how that fourth quarter was “unacceptable” on the decision, and that they are going to be extra assertive in reducing prices to match their decrease gross sales, nevertheless it’s additionally true that they don’t have plenty of management over what the demand surroundings appears like amongst their prospects, or when gross sales will come by.

Right here’s how they described the problem, that is CFO David Schulz on the decision:

“Just like the third quarter, progress in utility, industrial, information facilities and enterprise community infrastructure was greater than offset by declines in broadband, safety, OEM and development. We skilled buyer destocking in our shorter-cycle companies within the second and third quarters. Within the fourth quarter, we noticed a step-down in demand versus our expectations, significantly in December….

“As we moved into the fourth quarter and as we talked about on the earnings name in early November, we anticipated to see an acceleration of gross sales from October to November and once more into December, primarily pushed by the cargo of tasks from the backlog.

“As a substitute, we skilled an additional slowdown in our inventory and move gross sales, together with some mission delays, primarily inside our CSS enterprise. We had been anticipating natural gross sales to stay flat and as a substitute, they had been down roughly 3%.”

And issues haven’t bounced again but, which is why the steering was so surprisingly low — they mentioned that they continued to see gross sales declining in January, although from their feedback on the convention name the backlog did “tick up” to start out the yr.

I’m not in a rush to eliminate my WCC place, they usually’re now all the way down to a valuation of solely about 10X their anticipated free money move for 2024 (or if you would like actual numbers and never firm forecasts, 17X their free money move in 2023), however I’m extra more likely to promote down my place additional than I’m to purchase extra — as I famous final week, this was by no means a place that I thought of to be a “top quality” or “ceaselessly” inventory, I purchased with the intention that this could be a 3-5 yr commerce on realizing worth from their Anixter merger and benefitting from elevated electrical and telecom infrastructure spending. We’ve received the merger worth realized now, that three-year integration is full and was profitable, with their “synergy” targets all exceeded and the debt slowly starting to return down (the used debt to purchase Anixter, which was good for shareholders, partly as a result of debt was very low-cost again then, and have claimed nice ‘deleveraging’ since, although that principally means their money move covers the debt stage higher, because of rising earnings because the merger, not that the precise debt stage has come down). Nonetheless, although, a lot of the anticipated demand progress has not but actually materialized of their finish markets, although they nonetheless anticipate “secular progress” in these areas and it ought to be true that authorities incentive spending continues to be on its manner… we’ll see how issues cool down after this abrupt drop.

Right here’s what I mentioned again in August, after they had been getting the shock of a downward reset in expectations for 2023 (now downward sufficient, it turned out):

“I lean towards having some confidence that the enterprise is more likely to plateauing, not collapsing, and that there’s room for some margin enchancment and a resumption of some cheap low-single-digit income and high-single-digit earnings progress if we don’t undergo a significant down-cycle within the financial system, typically talking. Given quite a lot of uncertainties, now that they’ve “missed” two quarters in a row and that’s more likely to result in extra analyst and investor warning, significantly as they begin to speak extra about repaying their first tranche of debt (in 2025), I’ll pencil in a decrease “most well-liked purchase” now — over the previous decade the underside has been roughly 8X earnings, and if we use the decrease firm forecast for 2023 earnings ($15.50) as a substitute of the upper trailing earnings ($16.42 in 2022), that will get us a a lot decrease “most well-liked purchase” stage of $124. I don’t know if the inventory will fall that far, principally as a result of I don’t know whether or not they’re disappoint once more subsequent quarter, nevertheless it’s a superb quantity to search for. That might even be about 10X free money move, which is never a foul worth to pay until the corporate is in perpetual decline, and I don’t see any purpose to anticipate that’s the case right here.”

Properly, that free money move hasn’t fairly proven up but — but when they’re proper in projecting at the least $600 million in free money move for 2024 (their vary is $600-800 million, so, to be truthful, the forecast is actually $700 million the way in which most of Wall Road thinks about these issues), then 10X free money move can be $6 billion, or simply about precisely $117 per share. They’re now forecast to earn $14.67 in 2024, given the lowered earnings steering, and 8X that might even be about $117. I’ll bump down the “most well-liked purchase” to that stage (it was beforehand $124). I’ve held the “max purchase” at 11X earnings lately, and the bottom quantity we now have obtainable on that entrance, the forecast of $14.67 per share in earnings for 2024 (trailing GAAP earnings for 2023 had been all the way down to $13.84, however adjusted EPS got here in at $14.60 final yr, too, roughly the baseline stage they now anticipate for this yr). That might set “max purchase” at about $160, in order that’s most likely about probably the most you’d need to pay if WCC goes to develop at concerning the charge of inflation, pay a rising dividend, and purchase again some shares. The inventory might go increased, in fact, however that depends upon folks believing it to be a progress story once more — or on proving out the expansion potential over the subsequent couple years.

WESCO believes they’re a model new firm, and have come by a wild interval of dramatic shifts within the provide chain however at the moment are again on observe with roughly the pattern they had been on pre-Anixter, in 2019… and that yr, they traded in a spread of about 8-11X earnings, too. Perhaps that’s the rational stage if they’ll’t enhance their margins or change into extra of a value-added distributor, we’ll see.

For me, I’m keen to be considerably affected person and I don’t typically go “all in” or “all out” on an organization in a single fell swoop, however I believe the expansion potential for WCC is just not significantly compelling, and it’s most likely close to the highest finish of what a rational valuation may be in the event that they’re not going to develop, within the 10-11X earnings vary. It’s a greater firm than it was pre-Anixter, nevertheless it’s received the identical administration workforce, we’ve reaped a superb chunk of that reward already, and I’m not seeing rather a lot from administration that makes me change my thoughts about this being a shorter-term commerce in an organization that has been traditionally mediocre.

And that is what I mentioned again in that August replace about my huge image expectations:

As was the case 1 / 4 in the past, I believe WESCO within the $120s and $130s is a fairly clear shopping for alternative for the 2-4 yr infrastructure spending cycle we ought to be beginning proper now… and in the event you assume we will do this with out a significant industrial recession within the US, then you possibly can pay extra. I’m just a bit much less assured concerning the excessive finish numbers I used to be utilizing six months in the past, significantly after two quarters the place the enterprise has been harm worse than administration anticipated. I used to be considering lightening up this place somewhat bit after seeing the preliminary numbers, since that is at present a max allocation holding for me (about 4% of my particular person fairness dedication is to WCC), however after going by the financials extra totally and listening to the convention name, I really feel a bit extra reassured concerning the 2-3 yr prospects. I’m holding.

That ceased to be the case every week in the past, as I bought 1 / 4 of my shares… and following the final two quarterly updates and their new outlook for 2024, which signifies no actual anticipated progress or constructive outlook within the subsequent yr, and no signal that the gradual progress of Federal stimulus goes to be sufficient to offset slowness in different elements of the enterprise, I’m again to “much less assured”. Anticipating single-digit earnings progress throughout a interval of stimulative spending appeared cheap, significantly given how lengthy it has taken for that stimulus to really change into spending, however now that six extra months have handed, and extra tasks have been additional delayed than have moved ahead and change into orders, I don’t just like the trajectory.

If we’re taking a look at zero progress and a low valuation, as now appears extra possible, then I believe we now have some higher firms to contemplate today, so it’d make sense to decide on one with a stronger model, or a traditionally extra worthwhile enterprise that gives extra upside potential and the chance of margin growth sooner or later. Deere & Co. (DE) involves thoughts from our watchlist, since that’s a world chief whose earnings have stagnated of late and pushed the valuation all the way down to about 10X trailing earnings, an identical present valuation to WESCO, with each providing a weak 2024 forecast this week. I believe it’s extra possible that Deere will ultimately get better and create worth for buyers once more, regardless of the present projection that their earnings will dip about 20% this yr after which get better slowly from that time, than I’m that WESCO will present significant earnings progress and attain the next valuation within the subsequent couple years.

So I bought one other chunk of my WESCO shares as we speak, half of my remaining stake, at simply over $150, now that I’ve had a while to assume it over, the market has evened out a number of the preliminary overreaction to the dangerous quarter, and my buying and selling embargo from final week has lifted. I’m extra more likely to proceed to promote down that place over time than I’m to purchase extra, however I’ll attempt to preserve an open thoughts. That’s sufficient to ensure a revenue for this place, since I’ve now taken out about 10% additional cash than I put in, which is why it reveals up with a adverse adjusted value foundation within the Actual Cash Portfolio spreadsheet.

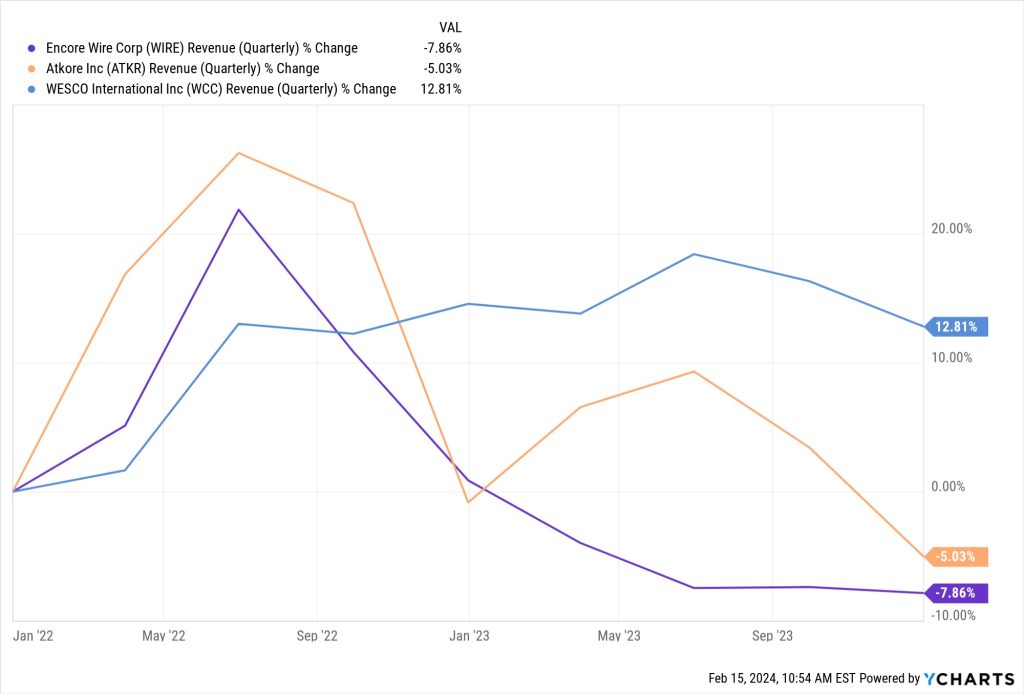

By the way, Encore Wire (WIRE), which like Atkore (ATKR) is a producer and provider of kit into these identical industries (ATKR principally sells conduit, WIRE principally sells copper wire, each are profoundly impacted by commodity costs), had a greater quarter than WESCO — their CEO mentioned, “Our workforce shipped a file variety of copper kilos within the fourth quarter as a consequence of constant sturdy demand for our copper wire and cable merchandise, representing the strongest quantity quarter over the course of the complete yr. Our skill to capitalize on this demand and ship unmatched velocity and agility in serving our prospects is a testomony to our single-site, build-to-ship mannequin, an vital aggressive benefit. We skilled sustained, elevated copper wire and cable demand from mid-2023, which continued by the fourth quarter.”

Nonetheless, although, due to shifting commodity costs, that quantity progress didn’t result in income progress — that is what the income of all three of these firms has seemed like over the previous two years, all of them surged in 2022, largely as a result of pricing and demand image benefitting from the provision chain disruptions, however have been been drifting down over the previous two quarters as that normalized:

*****

Then we received right into a bunch of principally high-growth shares reporting this week, the place outcomes are presupposed to be much more unstable (not like WESCO, which you wouldn’t assume ought to be inclined to those dramatic 25-30% post-earnings strikes, however has generally, together with this week, bounced round like a jumpy tech inventory).

The Commerce Desk (TTD) had truly a slight earnings “miss” final evening, analysts had overestimated earnings by a number of cents… however they guided for (continued) huge income progress within the first quarter, the income steering was about 6% increased than the analyst estimates, which might imply year-over-year income progress of at the least 25% subsequent quarter, and that received everybody excited, with the inventory immediately popping virtually 25% increased after earnings final evening (since settled all the way down to a ~18% achieve or so).

That’s awfully nutty, in fact, it’s powerful to argue that the earnings outcome, strong although it was, meant that all of the sudden TTD turned virtually $10 billion extra precious, and it got here again down rapidly after that overreaction, however suffice to say that TTD buyers had been happy. The precise adjusted earnings for the quarter got here in at 41 cents, roughly the identical because the analyst estimate, in order that was 23% earnings progress for the quarter, and income got here in at $605 million, about 4% increased than the forecasts and, as occurs with just about each fourth quarter, that was their greatest quarter ever.

That is so typically the sport with The Commerce Desk — it’s been an ideal progress firm since inception, with glorious income and earnings progress virtually each quarter, and clear scalability as their advert shopping for community, information and software program answer has continued to draw extra advert consumers, leavened by the truth that they’re one of many worst offenders within the “stock-based compensation” class. The inventory tends to react violently to ahead steering, so it dropped 20% after they supplied weak steering final quarter… after which surged this quarter after they beat that steering and supplied what was seen as optimistic steering for 2024. The money image has steadily improved, they usually’re beginning to develop sufficient to start to offset their big stock-based compensation, however the valuation continues to be very wealthy, regardless of the way you have a look at it.

I nonetheless like Jeff Inexperienced, and he has been constantly clear and fairly correct together with his outlook on the state of the promoting market — the convention name is at all times price listening to, however right here’s how he says issues are going now:

“Whereas there’s a lot to have fun about 2023, I’m much more enthusiastic about 2024 and past. I’ve by no means felt extra assured heading into a brand new yr. I consider we’re uniquely positioned to develop and achieve market share, not solely in 2024 however nicely into the long run, no matter a number of the pressures that our business is going through, whether or not it’s cookie deprecation, rising regulatory deal with walled gardens, or the quickly altering TV panorama….

“Typically folks taking a look at our huge international business regularly overlook considerably totally different strengths, weaknesses and alternatives for various kinds of firms. Some wrongly assume solely huge firms win, and smaller firms like us don’t. That paradigm is totally improper. Basically, the present shifts will assist firms with authenticated customers and site visitors, which additionally sit subsequent to great amount of advertiser demand.

“These macro adjustments harm these, particularly content material house owners and publishers who don’t have authentication. So this yr, CTV and audio have huge alternatives forward, and the remainder has pockets of winners and losers. However almost everybody can be both higher off or worse off. And I consider 2024 is a yr of volatility for the worldwide promoting market. And for many who are ready, like The Commerce Desk, it is a chance to win share. Our platform is ready as much as take advantage of any sign that may assist advertisers drive relevance and worth. Our platform now sees about 15 million promoting impression alternatives per second. And we successfully stack rank all of these impressions higher than anybody else on this planet based mostly on chance of efficiency to any given advertiser with out the bias or battle of curiosity that plague most walled gardens.

“With UID2, Kokai, and advances in AI in our platform, we now do that extra successfully than ever earlier than. And our work in areas corresponding to CTV, retail information, and id are serving to construct a brand new id and authentication cloth for the open web. So, no matter how the surroundings evolves round us, we’ll at all times have the ability to assist advertisers discover the proper impressions for them.”

So TTD continues to develop somewhat sooner than the general digital advert market, because it has principally accomplished for years, and administration may be very optimistic concerning the coming yr — they’re often optimistic, however I’d say that they had been qualitatively extra so this time round. In addition they elevated their buyback authorization to $700 million, although that’s not massively significant — at greatest, we will hope that they’ll use buybacks to offset a lot of the stock-based compensation.

It is a inventory the place the scalability is so clear that I’m keen to pay a stiff premium valuation, and have grudgingly accepted using “adjusted” numbers that ignore stock-based compensation, because the market has fairly clearly signaled that it doesn’t care about that in any respect. The scalability comes from the truth that they get a slice of every greenback spent on their platform, however primarily promote software program and information, that are inherently scalable as soon as the R&D and gross sales prices are absorbed, so earnings progress ought to outpace income progress fairly considerably over time.

However I additionally typically maintain out for dangerous days to purchase TTD, it’s not a inventory I’ve typically been in a position to justify when issues look rosy and buyers are excited. The extent I search for as a “max purchase” with TTD has been 40-45X ahead adjusted earnings, tied to what I see as very possible and sustainable common earnings progress of 20% going ahead — analysts haven’t but up to date their forecasts for 2024 earnings, however I’d guess that these estimates can be bumped as much as someplace within the $1.50-1.55 vary, maybe somewhat increased (they had been $1.45 earlier than the convention name). Probably the most optimistic quantity I can justify is 45X ahead adjusted earnings, in order that’s now $69… and it’s rather a lot simpler to justify one thing like 30X earnings, which is often my “most well-liked purchase” stage for this inventory, in order that’s about $47. TTD may be very unstable, as befits a inventory that at present trades at 25X revenues, a stage only a few firms have ever been in a position to justify for lengthy, and it’s very possible that buyers will discover one thing to fret about and we’ll see sub-$70 costs once more in some unspecified time in the future… however, in fact, there are by no means any ensures concerning the future.

And in the event you’re in search of a purpose to be cautious, stock-based compensation stays nutty, previous to this quarter TTD was utilizing new share issuance to cowl roughly a 3rd of their whole prices (together with the price of items, SG&A bills, all of the working prices). An enormous slice of that goes to Jeff Inexperienced personally, nevertheless it’s an enormous quantity general — stock-based compensation was lately operating at about $500 million a yr, and whole income for 2023 of $1.95 billion. That’s why GAAP earnings for final yr had been $0.36, whereas their adjusted EPS got here in at $1.26. Their buyback authorization would possibly heal a number of the dilution that comes from this, and it places their surplus money to work, nevertheless it’s actually extra like capitalizing payroll — it is smart as a enterprise proprietor if buyers are keen to disregard it, and if it incentives your workers to do nicely, nevertheless it’s not precisely a transparent approach to account in your working bills. It was once that just about each tech firm targeted on their adjusted earnings, however now, at the least, a lot of the huge guys (Alphabet, Apple, Amazon, and so forth.) have stopped reporting adjusted earnings and have gone “all in” with GAAP and accepted that stock-based compensation is an expense, not a approach to create “free” labor. TTD will most likely be embarrassed into becoming a member of them in some unspecified time in the future, however perhaps not quickly — if we’re fortunate, they’ll have progress that overwhelms this problem and makes it moot, as occurred with NVIDIA, one other serial abuser within the stock-based compensation area, over the previous yr, with NVDA lastly seeing its GAAP earnings come near catching as much as “adjusted” earnings.

*****

Roku (ROKU) outcomes had been about as anticipated, with income barely increased than forecasted. Energetic account progress was sturdy within the fourth quarter, as anticipated (numerous new Roku customers with new TVs), and streaming hours continued to develop, however the dangerous information was that they’d one other decline in common income per consumer (ARPU), with that quantity dropping under $40 for the primary time in a pair years (it had been within the low $40s since mid-2021, after a interval of dramatic progress by the early days of the pandemic), and their steering was not significantly optimistic — sort of the flip facet of TTD, and each do have some frequent drivers since they each basically experience on the again of the promoting business, with specific publicity to the migration of advert {dollars} from linear TV to streaming TV (although ROKU is much much less simply scalable, and arguably has stronger and extra worrisome opponents rising). They had been additionally the flip facet of TTD final quarter, when TTD disenchanted and ROKU excited buyers with their ongoing money move restoration and a few bumps up of their key efficiency indicators (like that ARPU quantity) which have turned worrisome once more now.

That weaker outlook presumably did rather a lot to trigger the large drop after hours final evening, once I glanced on the ticker it was down greater than 15%, within the excessive $70s, and it received worse because the morning trundled alongside, so it’s now round $72. ROKU has not been in a position to make that leap into actual profitability, although it’s enhancing on that entrance with extra value reducing, so with none sort of revenue quantity to lean on, there’s not a lot of a basis for the inventory when sentiment shifts. The inventory has bounced round fairly a bit with these sentiment adjustments, it has seen each $50 and $100 over the previous yr.

The price-cutting they’ve talked about has been working, although it required decreasing their R&D spend, which may be worrisome in terms of holding their market share sooner or later, and their units gross margin was nonetheless adverse, however a lot much less adverse than the earlier vacation season (they’re keen to promote units — TVs and streaming packing containers — at a loss to construct the consumer base), and the core platform enterprise did fairly nicely, with 13% gross revenue progress over the yr in the past interval as advert income picked up somewhat (“platform” means promoting and gross sales commissions for streaming companies, principally), nevertheless it didn’t develop as quick because the lively accounts or the streaming hours, or the digital streaming market as a complete, in accordance with The Commerce Desk, so that they’re not getting a lot leverage to the size of utilization of Roku TVs at this level. They did finish the yr with two quarters in a row of constructive money move and free money move, and constructive Adjusted EBITDA, although that was to be anticipated with the promoting restoration and their value reducing.

I discover the market outlook for Roku extra worrisome than I did in previous years, as a result of opponents have lastly begun to get some traction in constructing out competing working programs for good TVs — ROKU continues to be the chief, however Amazon is closing in, and Walmart is rumored to desire a bigger function on this area as they consider perhaps shopping for Vizio, a TV maker who has continued in constructing its personal working system (although it’s nonetheless trivially small, so most likely wants an even bigger associate to get any promoting traction). Roku’s system continues to be higher than the competitors, and is way stronger amongst lower-income customers due to their superior “free TV” choices, which ought to give them somewhat extra publicity to promoting spend… however the opponents who Roku lapped final time in taking management of this market a decade in the past haven’t given up, they usually’re coming again for one more battle.

The large distinction between final quarter and this was simply the extent of optimism within the outlook — final quarter they had been on the way in which up, they usually overshot analyst estimates and advised analysts to extend their numbers… this quarter they nonetheless beat these numbers, however successfully advised analysts to convey their future numbers down somewhat — this was how they acknowledged their steering this time:

“We plan to extend income and free money move and obtain profitability over time. On the identical time, we stay conscious of near-term challenges within the macro surroundings and an uneven advert market restoration. Whereas we’ll face troublesome YoY progress charge comparisons in streaming companies distribution and a difficult M&E surroundings for the remainder of the yr, we anticipate to take care of our This fall 2023 YoY Platform progress charges in Q1. This can end in Complete web income of $850 million, whole gross revenue of roughly $370 million, and break-even Adjusted EBITDA in Q1. Persevering with our efficiency from 2023, we anticipate to ship constructive Adjusted EBITDA for full yr 2024.”

2023 was higher than 2022, and 2024 ought to be higher nonetheless… nevertheless it nonetheless gained’t be almost nearly as good as 2021, when the streaming wars and COVID lockdowns turned Roku right into a profit-generating machine. I believe they’re stepping into the proper route, and I’m keen to be affected person as we see if they’ll maintain on to their market share with their new TVs, partly as a result of I’m actually impressed with the way in which that Roku got here out of nowhere to beat Apple, Alphabet, Amazon and so many others on this area the primary time round, and I just like the aggressive targets of founder/CEO Anthony Wooden… however I don’t have to make this a bigger place, not whereas we’re nonetheless ready to see how streaming tv evolves and the place the earnings find yourself settling. I’m protecting my valuation numbers the identical for ROKU, given the failure to develop ARPU this quarter, so “max purchase” stays at $68, “most well-liked purchase” at $46, and this stays roughly a 1% place for me… sufficiently small to comfortably take up the volatility and proceed to be affected person. I nonetheless just like the enterprise, however I don’t see any goal purpose for the numbers to enhance dramatically this yr.

*****

Kinsale (KNSL) reported one other walloping beat of the earnings estimates, they’d $4.43 in earnings per share within the fourth quarter, in order that’s 53% earnings progress… and for the complete yr, that meant $13.22 in earnings, which was simply shy of 100% progress (analyst had forecast $12.04). That they had very low catastrophe-related claims within the quarter, which was frequent to a lot of the insurance coverage firms I observe, and the quarter had a mixed ratio of 72.1%, which was sufficient to convey the full-year ratio all the way down to 75.4%. Outstanding profitability and progress for an underwriter, which is, in fact, why it trades at a a lot increased valuation than just about every other underwriter. Because of increased rates of interest, the funding revenue that was basically a rounding error in 2022 doubled in 2023, so it’s starting to change into an actual contributor (underwriting revenue was $270 million for the yr, funding revenue $102 million).

In the event you haven’t adopted Kinsale, they write non-standardized insurance coverage, referred to as “extra and surplus strains” protection, so that they cowl issues that different insurers can’t or gained’t cowl simply in “admitted” markets (which usually have their pricing regulated by states, with extra standardized insurance policies). A lot of stuff is shifting into the surplus and surplus markets as protection will get trickier, or as insurers abandon totally different risk-prone areas, and Kinsale has specialised in utilizing its expertise and information to extra rapidly underwrite E&S insurance policies, particularly for smaller prospects who’ve a tough time getting quick solutions from bigger underwriters. In CEO Michael Kehoe’s phrases, on the decision:

“Kinsale focuses completely on the E&S market, and on writing smaller accounts. We offer our brokers with the broadest danger urge for food and the perfect customer support within the enterprise. And we use our low expense ratio to supply our prospects competitively priced insurance coverage, whereas additionally delivering best-in-class margins to our stockholders.

“Since a lot of this expense benefit relies on our superior programs and our workforce of world class expertise professionals, we consider the aggressive benefit of our expertise mannequin not solely has sturdiness to it, however has the potential to change into much more highly effective within the years forward.

“As we now have famous during the last a number of years, the E&S market continues to profit from the influx of enterprise from normal firms and from charge will increase pushed by inflation and comparatively tight underwriting situations.”

You would possibly say that $10 billion (Kinsale’s market cap) is rather a lot to pay for an insurance coverage firm with somewhat over $300 million in web revenue, and also you’d be proper — KNSL is buying and selling at somewhat over 30X earnings today and greater than 12X e-book worth, a wealthy valuation, roughly twice that of the second-richest-valuation amongst comparatively giant insurance coverage firms (that might be Progressive (PGR), which is at about 5X e-book worth and 28X earnings)… nevertheless it’s additionally clearly separated itself from the pack, performance-wise, over the previous couple years. Extra & Surplus strains insurance coverage, which is all Kinsale does, is getting extra vital as extra common insurers drop protection of sure enterprise strains or geographic areas and as dangers get extra uncommon, and Kinsale clearly has an enormous benefit in the way in which they worth and promote their protection. No person else appears to be even shut, and Kinsale nonetheless has lower than 2% of the E&S market, so there ought to be alternative for them to proceed to develop.

It’s not going to get much less dangerous, although — there’s a purpose why insurance coverage firms (virtually) by no means commerce at these sorts of valuations, and it’s principally simply that they’re within the enterprise of judging and taking danger, and generally they get stunned. Kinsale is doing extremely nicely, however we shouldn’t assume they’re excellent — one thing might dramatically upset their underwriting and make it clear that they wildly mispriced a danger in one among their bigger strains (they write principally legal responsibility protection, but additionally some property, significantly in dangerous areas — like Miami skyscrapers), and there could possibly be some extent the place they lose fairly a bit of cash. Hasn’t occurred but, they usually shouldn’t have plenty of long-tail danger in comparison with some insurers (who’ve reserves to cowl insurance policies they wrote many years in the past, in some circumstances, as danger perceptions change or new liabilities seem), however whereas I’ve accepted that Kinsale clearly has constructed an edge, and may be valued like a progress inventory, I additionally preserve my allocation considerably restricted as a result of there’s the looming danger that one thing shocking might upset their black field danger calculations… and, in fact, the chance that buyers will change their thoughts after a foul quarter, and determine Kinsale doesn’t need to commerce at an enormous premium to the opposite E&S underwriters. This sturdy quarter brings Kinsale to new all-time highs once more, over $500, they usually proceed to say that they’re optimistic concerning the progress persevering with — with submissions for quotes rising greater than 20% final quarter, which was accelerating progress on that metric.

And whereas there’s at all times some potential danger, they’ve diversified nicely, partly by specializing in smaller prospects, they usually do say that they consider they’re over-reserving — right here’s how Kehoe put it within the Q&A, when requested concerning the rising tendency of juries handy out giant awards in insurance coverage circumstances:

“Kinsale is an E&S firm. We make frequent use of protection limitations to assist us management our publicity to loss. We additionally are likely to deal with smaller accounts, which most likely insulates us somewhat bit. And I believe we run a really disciplined underwriting operation. We’ve received actually good programs, which interprets into strong information to handle profitability. So it’s one thing that creates, I believe, a problem for the business. However I believe Kinsale is superb at staying forward of adjustments within the tort system.

“Once you add to that the conservatism and the way we method reserving, once more, I believe buyers ought to have plenty of confidence within the Kinsale steadiness sheet.”

So I’m fairly assured, however the valuation means issues must proceed to go very well, if not essentially completely.

I pencil in 25X ahead earnings as my “most well-liked purchase” stage for Kinsale, and 40X trailing earnings because the “max purchase,” given how unpredictable their earnings should be. With $13.20 now within the books for 2023, that might be a “max purchase” of $528 — that appears bold, nevertheless it’s more likely to be OK so long as Kinsale can continue to grow income and earnings by at the least 20% a yr, which is my baseline expectation… and that’s additionally fairly near the place the inventory is buying and selling in the mean time, after the 20% post-earnings pop within the share worth (income progress has been nicely above that 20% progress stage for all however two or three quarters since they went public in mid-2016,… earnings progress has been extra unstable however has averaged way more than 20%, each income and earnings per share have grown at a compound common charge of 37% since that IPO, virtually eight years in the past).

My “most well-liked purchase” stage settles in at $360 now, which can be roughly the place the shares had been buying and selling six weeks in the past, and fairly near my final purchase within the $340s. I think about issues will proceed to be unstable, and the inherent danger of their enterprise, which shouldn’t have the ability to develop this quick ceaselessly and will, at this sort of valuation, convey a 50% in a single day drop within the share worth in the event that they’ve made a vital underwriting error someplace and report a horrible quarter sometime, means I’ll proceed to cap my publicity right here to a few half-position (roughly 2% of my fairness capital), however Kinsale has steadily been incomes this sort of valuation so I’m at the least completely happy to let it experience, and can possible proceed to nibble if costs keep in my vary as I add extra capital to the portfolio. The danger of a horrible consequence fades as they proceed to execute so nicely, and because the Extra & Surplus Traces market continues to be completely arrange for them to take share, however I don’t need to change into too complacent in assuming that can ceaselessly be the case sooner or later. I’ve drunk the Kinsale Kool-Ade, and I’m loving it… however I can at the least inform the bartender to carry off after half a cup.

And after we noticed the large underwriting problem Markel had final quarter, it was at the least somewhat reassuring to listen to this from Michael Kehoe within the convention name:

“… there’s plenty of firms popping out saying, hey, we have to take an enormous cost as a result of we didn’t put sufficient away in previous years. And we’re making an attempt to present our buyers confidence and say, that’s not coming right here.”

And the investor response would possibly fairly be, “at 12X e-book worth and 40X earnings, it higher not.”

*****

Toast (TOST) is without doubt one of the less complicated tech shares I personal — with its big market share in restaurant POS programs, it basically acts like a royalty (between 0.5-1%) on restaurant gross sales. They’ve invested closely in a gross sales pressure to push their cost programs out to increasingly eating places, concentrating on constructing max focus in geographic areas, which then ought to construct as much as a community impact of kinds, letting them proceed to develop with much less “gross sales” funding, they usually’ve been making an attempt to construct on the success of the funds platform by promoting extra add-on software program modules to Toast eating places. There’s competitors on this area, so the problem is that they’ve spent rather a lot on constructing that gross sales pressure, and must preserve spending on R&D to maintain the platform interesting to their prospects, at the same time as there’s at all times some churn as a result of plenty of eating places fail… however the relentless progress of that “royalty” over time makes the potential for distinctive returns engaging, as soon as they start to essentially scale as much as constant profitability and, most probably, big revenue progress within the coming 5-10 years if the general shopper financial system avoids an enormous recession.

Info leaked out yesterday, earlier than the earnings launch, that Toast had laid off about 10% of its workforce, becoming a member of the parade of tech firms who’ve a newfound curiosity in effectivity and profitability, however that didn’t inform us a lot about who was being laid off, or what which may imply for the corporate… for that, we needed to wait till they really reported earnings final evening. Was it as a result of they’d reached self-sustaining scale in gross sales, they usually didn’t want as giant a gross sales pressure? Was it as a result of gross sales had been weaker than anticipated, they usually needed to reduce prices? Only a realization that they’d over-hired, like many tech firms in recent times? Toast is the corporate that’s bodily closest to Gumshoe HQ, they’re in Boston and I’m solely about 100 miles away, and I think about most of us most likely know a restaurateur that makes use of the platform, however I’m afraid that didn’t led me to any nice perception on what these layoffs would possibly imply. Which is OK, we don’t must commerce on each bit of reports… I resolved to attend a full 12 hours earlier than I had extra data. I do know it’s silly, however today, sadly, that generally looks like some Warren Buffett/Charlie Munger stoicism and persistence. Ready for actual data? How quaint!

Properly, turned out that this was a “restructuring” the board agreed to, which principally sounds smart. And the outcomes had been fairly strong, Toast added one other 6,500 areas within the fourth quarter, so that they’re as much as 106,000 now, and their annualized recurring income run charge grew 35% over the previous yr to now $1.2 billion (that’s from each their cost processing “royalty” on a stream of gross cost quantity that’s now over $33 billion a yr, and the extra worthwhile, however smaller income, software program subscriptions). That they had mildly constructive EBITDA and constructive money move, as has been the case for a pair quarters, however are nonetheless shedding cash on a GAAP foundation… they usually nonetheless have loads of money, that enduring legacy of the truth that they lucked out by going public when valuations had been silly, in late 2021.

They anticipate adjusted EBITDA to stay constructive and develop, reaching $200 million this yr (the comparable quantity was $61 million final yr, which was their first yr with out a adverse quantity in that column). They usually made some giant offers, increasing into bigger enterprises — they’re going into Caribou Espresso with their Enterprise Options, and into Alternative Accommodations (for eating places at Cambria and Radisson lodges, at the least, and perhaps extra), so they’re encroaching on the large prospects which can be slower to vary, which is nice information (although it’s arguably mildly adverse information for PAR Know-how, our different small restaurant POS supplier, since huge chains are their core enterprise… I believe there’s loads of room for each, significantly given PAR’s big benefit with the bigger quick meals chains, however in some unspecified time in the future the competitors will most likely tighten with these two and the opposite new and legacy suppliers).

That’s roughly the sort of adjusted EBITDA that ROKU analysts expect, apparently sufficient, although ROKU is projected to be 2-3 quarters behind in reaching that levle, and the 2 are anticipated to have fairly comparable progress as nicely, and are comparable in measurement (market cap $10-12 billion), however I’m much more assured in projecting the long run profitability ramp for Toast, given the stickiness of their prospects and the stableness of their funds and subscription income — partly as a result of it’s rising the consumer base sooner and the income line and gross revenue a lot sooner. Roku’s solely actual benefit in that comparability is that their finish market is way bigger… however Toast continues to be removed from saturating their market, they usually’ve barely begun to maneuver abroad. Not that the 2 are immediately comparable, however generally it’s price evaluating two unprofitable progress firms to see if one clearly stands out as extra hopeful or extra predictable, and on this case Toast appears much more compelling due to that extra predictable future.

Toast is just not fairly as straightforward a purchase now because it was final Fall, when buyers had been frightened about their final quarter and I added to my holdings, nevertheless it’s nonetheless in a fairly cheap valuation vary given the fairly predictable income progress, so long as you’re keen to attend for that progress to change into actual earnings as they scale back prices and proceed to scale up their consumer base over the subsequent few years. I haven’t modified my valuation considering, for me TOST continues to be price contemplating as much as a max purchase of $26 and is extra interesting under my “most well-liked purchase” stage of $18, and we’re proper in the midst of these two numbers after a superb post-earnings “pop” as we speak. It’s a bumpy experience, they usually aren’t clearly or abundantly worthwhile but, which implies they have an inclination to get bought down each time buyers are feeling fearful, so being affected person can work… however this is without doubt one of the few speedy progress firms the place I personal and the inventory reported nice outcomes and an optimistic outlook, together with the cost-cutting from these layoffs and a brand new buyback authorization, and the inventory popped a lot increased (a 15% leap this time), and but the inventory stays under my “max purchase” quantity. In order that’s one thing.

*****

Some extra minor updates…

BioArctic (BIOA-B.ST, BRCTF) reported its ultimate 2023 outcomes, with no actual shock — for many who don’t recall, BioArctic was the unique developer of what Eisai and Biogen became Leqembi, the one authorised disease-modifying remedy for Alzheimer’s Illness, and the rationale we personal it’s as a result of though BioArctic continues to develop different early-stage therapies for mind ailments, with their most superior new molecule being in Parkinson’s Illness, the corporate itself is actually a small R&D store which, if Leqembi turns into an enormous and long-term hit as an Alzheimer’s remedy, take pleasure in huge royalties on these gross sales. It’s slow-developing, principally as a result of this primary formulation of Leqembi is difficult to prescribe and exhausting to supply, so Biogen and Eisai have needed to do plenty of affected person and supplier training and construct out an infrastructure to serve them, however dosing is ongoing within the US and Japan, and can start in China later this yr, so there stays potential for this to be a blockbuster drug… significantly if the subcutaneous model will get authorised within the comparatively close to future, making dosing a lot simpler (at present, it must be infused). My intent was to attend at the least a yr or so to see how the ramp-up of Leqembi gross sales proceeds, and I could have to attend longer than that, given the gradual begin, however from what I can inform every little thing continues to be continuing simply tremendous. Right here’s their press launch with the most recent outcomes, if you would like the specifics, nevertheless it doesn’t imply a lot — we’re nonetheless simply ready for the large potential affected person base to get entry to Leqembi, and, given the valuation of BioArctic, I don’t assume we’re risking a ton as we wait… however any unbelievable returns would possibly nicely be a number of years down the highway, and are removed from sure.

Royal Gold (RGLD) launched its full earnings replace, and was proper consistent with the preliminary outcomes they shared in January, so my estimate of money move was fairly shut (I figured they’d have working money move of $414 million, the reported $416 million), they usually supplied top-line steering for GEOs (gold equal ounces) to be about the identical within the first quarter because it was final quarter (47-52,000 GEOs — final quarter it was 49,000). Ultimately, web revenue for 2023 was about the identical as 2022, however they did increase the dividend a bit and enhance the steadiness sheet. They didn’t give any steering going additional out, however they most likely will achieve this subsequent quarter — and given their income sources (76% gold, 12% silver, 9% copper final yr), the inventory will presumably rise or fall with gold costs. They don’t have fairly the identical single-property danger that we’ve seen from Sandstorm Gold (Hod Maden) and Franco-Nevada (Cobre Panama) over the previous yr, at the least within the eyes of buyers, so the shares are holding up fairly nicely over the previous yr (not doing in addition to Wheaton Valuable Metals, higher than FNV or SAND)… so RGLD nonetheless has a greater valuation than every other giant gold royalty firm aside from Sandstorm (which stays less expensive, since folks hate it proper now following their at-least-temporarily-dilutive acquisitions), and it has a greater possible income/earnings/money move progress profile than FNV or SAND, with progress more likely to be about nearly as good as WPM (which is much costlier).

No change to my evaluation at this level, RGLD can be the best purchase among the many huge royalty firms, with historic stability and a fairly discounted valuation and a few possible manufacturing progress… however Franco-Nevada is near being “buyable”, given the disastrous crunch they took from the Cobre Panama closure final yr (they don’t report till early March, so I’m hoping they’ll disappoint and take a beating once more, FNV has at all times been price shopping for when it trades just like the ‘common’ royalty firms, and people moments have been pretty uncommon). Sandstorm is so hated that it’s exhausting to know when issues would possibly flip, we’re actually ready for Nolan Watson to show he meant it when he mentioned that Sandstorm’s progress is “in development” now, they usually’re basically accomplished with their huge acquisitions… in that case, and if their assortment of mines comes on-line roughly as anticipated, they need to outperform all of the others, however that is still an enormous “if.”

And Sandstorm Gold (SAND), which likewise had preannounced a few of its 2023 numbers, reported final evening — right here’s what I mentioned final month, after we received their top-line numbers:

Development is just not going to be nice within the subsequent yr or so until the gold worth goes meaningfully increased, since their bigger progress properties (new mines) gained’t be coming on-line immediately, however there are some new mines and a few growth tasks within the works, and manufacturing ought to develop barely. Assuming that Sandstorm CEO Nolan Watson has realized some classes from his aggressive acquisitions, and is genuinely keen to sit down on his arms and cease issuing shares, Sandstorm will have the ability to spend the subsequent couple years paying down debt and letting the precise money move lastly start to compound, so there’s nonetheless a superb path to a really sturdy return over the long run, if gold costs don’t collapse — nevertheless it’s comprehensible that buyers are sick of ready, given Sandstorm’s critical underperformance relative to its bigger gold royalty friends, and the truth that they took some dilutive steps backward on the “capital effectivity” stairway in 2022 as a way to increase their asset base and enhance their future progress profile.

The ultimate numbers had been a hair decrease than their preliminary ones, since precise accounting income of $180 million fell in need of the $191 million “whole gross sales” quantity they’d preannounced, however the important thing metrics don’t change that a lot (working money move was $151 million, and I had anticipated $155-160 given their top-line steering). They continued to speak about delevering this yr, promoting non-core property to pay down debt, and being disciplined about ready for the expansion to emerge from the portfolio they already personal, which is constructive in my e-book. My “max purchase” is 20X working money move for SAND, too, although I additionally web out their debt (because it’s appreciable), and that might nonetheless be $9 — very, very far-off, partly, I believe, as a result of buyers don’t actually belief Watson to essentially cease making these huge acquisitions that gained’t bear fruit for a few years. “Most popular purchase” stays about half of that, so would imply shopping for the corporate at near a ten% money move yield (working money move is just not the identical as free money move or earnings, however I did web out the debt steadiness, and also you get the final thought).

I’ve been too cussed with SAND, and both RGLD or FNV might be a safer funding due to the size of time it has taken for Sandstorm’s progress property to be constructed, however these property are nonetheless very more likely to be developed (or accomplished, for those in improvement), and I believe SAND administration has absorbed the exhausting lesson of their too-ambitious acquisitions and can let the portfolio develop organically. Which ought to imply that Sandstorm has way more progress potential than the opposite gold royalty firms if we see one other gold bull market, as a result of they need to take pleasure in each income progress from new mines coming on-line and a number of growth as they catch again up with the extra beloved gamers on this area…. however that’s been true for a number of years, and I wouldn’t blame you for being skeptical.

*****

Teqnion (TEQ.ST) experiences tomorrow morning, following the Berkshire Hathaway mannequin (problem monetary experiences on the weekend, so folks can assume them over when the inventory isn’t shifting round), so we’ll see how that goes — enthusiasm has risen for this inventory once more, as extra buyers have found it, which implies the inventory has hit new all-time highs this week within the absence of every other information about their subsidiaries (or any new acquisitions lately), so it’s at a tough-to-justify valuation of about 35X earnings in the mean time… however that’s OK. I’ve fairly nicely purchased into the plan from Daniel and Johan, and I intend to be affected person with this one.

Berkshire ought to report every week from tomorrow, by the way, and has bumped up above my “max purchase” worth for the primary time in a really very long time, so it’s going into this subsequent earnings report as an awfully standard inventory… we’ll see what occurs, however the underwriting and funding earnings will most likely be fairly distinctive. And perhaps they’ll lastly inform us what inventory they’ve been secretly shopping for, with waivers from SEC disclosure, over the previous two quarters (Berkshire has been constructing at the least one place, most likely within the monetary sector, that they’ve requested the SEC to allow them to not reveal of their final two 13F filings — which isn’t that uncommon, Berkshire has accomplished the identical a pair occasions prior to now, although two quarters in a row is somewhat shocking and means they need to nonetheless be shopping for no matter it’s, so it could possibly be a big place of one thing huge, although they must disclose if it reaches 5% possession in anybody firm).

*****

I received a reader query about NVIDIA (NVDA) and SoundHound AI (SOUN) this week, and thought others may be within the reply… since for most likely silly regulatory causes, and as a consequence of a scarcity of economic training amongst monetary writers, it turned NEWS this week that NVIDIA owns somewhat little bit of SoundHound. That ship the inventory of SOUN up virtually 70%.

What truly occurred? Right here’s an expanded model of what I wrote in a remark to that reader:

NVIDIA has owned somewhat slice of SoundHound because it was a enterprise funding a very long time in the past — perhaps 2017? I must verify to make certain, however the date doesn’t actually matter. There was a flurry of curiosity this week due to NVIDIA’s disclosures a few handful of small enterprise investments it owns… however I consider none of these are new, it’s simply that NVIDIA didn’t beforehand have sufficient worth in outdoors investments that it was required to file a 13F.

What modified? ARM Holdings (ARM) went public, and that’s NVIDIA’s largest funding by far (presumably a remnant of after they tried and failed to amass Arm Holdings from Softbank a pair years in the past, although it’s attainable they purchased extra). I’m guessing that because the IPO was within the final days of the third quarter, NVIDIA most likely was presupposed to file a 13-F in mid-November to acknowledge that holding as of the third quarter, as a result of their whole funding portfolio was most likely price greater than $100 million at the moment, for the primary time (I believe “managing $100 million” is the cutoff for being required to file a quarterly 13-F of your US fairness holdings, however the quantity might have modified since I final checked), however there could also be technical the explanation why they didn’t have to take action at that time, perhaps they get somewhat grace interval after an IPO or one thing. Now they do must file the 13F, although, due to their positions in ARM and RXRX, which now add as much as a bit over $300 million. Except the values of these positions drop under $100 million, or they promote these (comparatively) bigger stakes in ARM or RXRX, NVIDIA will now be submitting 13Fs every quarter.

I might not purchase something simply because NVIDIA was pressured to file the main points of their possession stakes in 5 firms that they’ve invested in on a enterprise stage or have possession stakes with as a consequence of a partnership (like Recursion (RXRX), which is their second-largest funding after ARM, and the one different one among significant measurement). NVIDIA’s holdings in ARM are at present price somewhat over $200 million, and in RXRX just below $100 million, so these are barely rounding errors for an enormous agency like NVIDIA… however NVIDIA’s stakes in Soundhound, TuSimple (which is delisting and on its approach to changing into much more irrelevant, most probably), and Nano X Imaging (NNOX), the one different three publicly traded firms they maintain some shares in, are all lint on the shoulder of the rounding error. All these stakes are nicely beneath $5 million.

Extra importantly, I’d say that none of these symbolize a brand new dedication of capital by NVIDIA this quarter, or a strategic endorsement of these companies by the main AI chipmaker. If I had been buying and selling Soundhound, I’d take into account this a present horse price promoting after that surge, although you probably have causes you need to personal it for the long run (I don’t), this surge may be irrelevant in a decade.

So NO, NVIDIA did NOT simply purchase SOUN or TuSimple (TSPH), it doesn’t matter what you learn. They only disclosed these tiny holdings for the primary time. Even the bigger holdings in ARMH and RXRX are irrelevant to NVIDIA and to ARMH, although I assume because the RXRX funding by NVIDIA was simply final yr, and it’s a much smaller firm, I assume you may argue that RXRX is impacted by NVIDIA’s strategic funding within the firm (although that’s additionally not new, the funding was made again in July and despatched RXRX shares hovering to shut to $40… they’re round $13 now, regardless of a pop on this 13F launch, so NVIDIA is to date shedding cash on that — although, once more, it’s a trivial amount of cash for NVIDIA, basically only a approach to seed one other buyer with somewhat money to assist transfer AI drug uncover analysis alongside, and create extra of a marketplace for NVIDIA’s chips sooner or later).

I’m not going to become involved with any of those shares, to be clear, however I’d be tempted to guess in opposition to TuSimple, SoundHound or Nano X after this foolish NVIDIA-caused pop of their shares this week, to not purchase them. Normally when unprofitable and story-driven shares leap for no purpose, they arrive again down fairly rapidly when sanity prevails… although all of us noticed GameStop (GME) a number of years in the past, and different nutty tales just like the Reality Social SPAC, Digital World Acquisition (DWAC) this week, so one can by no means be all sure about when or if sanity will prevail.

That stage of inanity in TSPH, SOUN and NNOX this week is yet one more signal of the approaching apocalypse for the “AI Mania” shares, I’m afraid, and the sort of factor that conjures up visions of this being one other “dot com bubble.” It would or may not be, in fact, we will’t predict the long run, and in some ways the valuations of the largest AI-related shares (NVIDIA, MSFT, GOOG, and so forth.) are FAR extra cheap than the valuations of the largest dot-com shares earlier than the crash in 2000, however the rhymes are sounding increasingly acquainted.

Probably the most cheap counter-argument to that’s not that this isn’t a foolish and excessive valuation bubble for the AI-related story shares… no, the perfect counter-argument, I believe, is that it’s not excessive sufficient but, and that is extra like 1998 than 2000, so we’d simply be getting began on our approach to a really loopy bubble. There could also be extra mania to return.

A reminder of the apocryphal bumper stickers in Silicon Valley circa 2004 or so, “Please God, Simply One Extra Bubble.”

NVIDIA earnings forecasts preserve going up, and analyst worth targets preserve rising, so there’s nonetheless no expectation available in the market that their income progress will decelerate markedly, or, extra importantly, that this slowdown can be related to a significant drop in revenue margins as slowing demand (ultimately) cuts into their pricing energy. I mentioned again in December, following the final earnings replace, that I might rationally justify a spread of valuations from $300 to about $680, however was extra more likely to take earnings close to $500 (the place it was then) than to purchase extra wherever close to that stage. For at the least a short while this week, NVIDIA, with ~$20 billion in working revenue during the last 4 quarters, turned bigger than both Alphabet (~$85 billion in working revenue) or Amazon ($37b). Buyers love progress, and over the previous 5 years NVIDIA’s income progress (whole 318%) has actually been a lot increased than virtually every other very giant firm (AMZN was 138%, GOOG 117%, solely Tesla (TSLA) actually competes on that entrance with 328% income progress — although as a producer, their margins are dramatically much less spectacular) .

Since my final remark, the analyst forecasts for the subsequent two years have gone up a bit, with none actual information from NVIDIA however with normal rising optimism about A.I. spending from the tech titans over the previous few weeks… so we’re heading into earnings now with analysts anticipating $18.32 in GAAP earnings over this fiscal yr that’s simply beginning now (FY25), up from $17.79, and $21.50 subsequent fiscal yr (FY26), up from $20.76. (The adjusted earnings numbers are increased, although as I famous the expansion has closed the hole, they’re at $20.71 and $25.17, however I can’t significantly think about using much more optimistic numbers for a corporation that’s already flying on optimism, not after they’ve received a $1.8 trillion valuation. and commerce at 40X trailing revenues.)

I’m nonetheless holding on to a significant stake in NVIDIA, having owned the inventory however traded it poorly for a few years, so let that be a lesson to you in the event you’re following my portfolio in any element — generally I commerce fairly badly, and that has been extra true with NVDA than with a lot of the shares I’ve owned over the previous decade. With that caveat, I’m keen to carry on to see how this performs out… however after the mania represented by these SoundHound trades as we head into NVDA earnings subsequent week (they report after the shut on Wednesday), and because the inventory crests 40X gross sales, I can’t resist shaving off somewhat extra of my revenue.

So I bought 10% of my NVIDIA shares because it toyed with $740 as we speak, going into subsequent week’s earnings replace. It’s solely attainable, and even rational, to mission that the demand for his or her GPUs will preserve hovering for a pair years, the get together will preserve going, and that NVDA will see $1,200 a yr from now… nevertheless it’s additionally solely attainable that demand softens just a bit, and margins get again to one thing extra like regular, resulting in a lot decrease earnings than anticipated, and NVDA falls to $300 over the subsequent yr (or additional, if there’s a real crash within the tech shares — although I don’t assume that’s significantly possible). The one factor analysts have been constant about is that they’re at all times very improper in estimating NVIDIA’s earnings, much more so than with most firms — and that’s true when issues all of the sudden get surprisingly worse, simply as it’s when issues get surprisingly higher.

In order that’s what I did this week… taking some partial earnings on each a fairly low-cost inventory (WCC) and a wildly costly one (NVDA), for various causes. I didn’t put any of that money to work simply but, however I’ll let once I achieve this.

And that’s greater than anybody individual ought to must learn, and I need to get this out to you earlier than the market shut, since some people have requested what I’m doing with these WESCO shares, specifically, so there you’ve gotten it… questions? Feedback? Simply use our completely happy little remark field under… and thanks, as at all times, for studying and supporting Inventory Gumshoe.

P.S. I’ll be on a diminished schedule subsequent week as I take a while to loll within the solar with the household through the youngsters’ trip break, so there may not be many new articles for a number of days, however I’m positive I’ll provide you with one thing to share by the point your subsequent Friday File is due.

Disclosure: Of the businesses talked about above, I personal shares of NVIDIA, Berkshire Hathaway, PAR Know-how, WESCO, Kinsale Capital, The Commerce Desk, Atkore, Roku, Toast, Alphabet, Teqnion, Royal Gold, Sandstorm Gold, BioArctic, and Amazon. I can’t commerce in any coated inventory for at the least three days after publication, per Inventory Gumshoe’s buying and selling guidelines.

Irregulars Fast Take

Paid members get a fast abstract of the shares teased and our ideas right here. Be a part of as a Inventory Gumshoe Irregular as we speak (already a member? Log in)

[ad_2]

Source link