[ad_1]

Ltd. - [GBPJPY,H4] 12_13_2023 9_40_23 AM (2)")

Information studies indicating a fall in UK wages in October prompted Sterling to say no, however draw back dangers have been restricted as this information is unlikely to alter the Financial institution of England’s coverage stance on Thursday (14/12).

Payrolls fell barely by -13k in November, in comparison with October. Comparatively to November 2022, paid employment rose by 1.1% y/y or 333k. In the meantime, month-to-month wages elevated by 5.3% y/y, slowing from 6.2% y/y. Within the three months to October, the unemployment fee was unchanged at 4.2% y/y. Common earnings development (together with bonuses) slowed from 8.0% y/y to 7.2% y/y, under expectations of seven.7% y/y. Common earnings development (excluding bonuses) slowed from 7.7% y/y to 7.3% y/y, under expectations of seven.4% y/y. Supply: ONS.

Following the information, cash market charges present merchants are actually totally anticipating the Financial institution of England’s first reduce of 25bp for June, whereas the primary reduce was anticipated in August earlier within the week. The Pound Sterling has weakened because of continued fee reduce hypothesis.

The Financial institution of England is of the opinion that wages, that are a significant factor in home inflation, are nonetheless too excessive to be in step with decreasing inflation to the two.0% goal. Whereas this might be a optimistic end result, the BOE is anticipated to maintain rates of interest at 5.2% for a while primarily based on the information.

The chance of the BOE being extra ‘hawkish’ in its assertion on Thursday stays low, as this wage information suggests a looser labour market, beginning to result in slower wage development. The financial institution believes it’s on observe to decrease inflation, however wish to see an extra decline in wage pressures earlier than contemplating a fee reduce.

In the meantime, Japan’s PPI slowed from 0.9% y/y to 0.3% y/y in November, however beat expectations of 0.1% y/y. Nonetheless, it was nonetheless the weakest tempo since February 2021. November marked the eleventh consecutive month that the tempo slowed. Export costs have been unchanged at 0.9% y/y. The decline in import costs slowed from -12.7% y/y to -9.7% y/y, remaining damaging for the eighth month. On a month-to-month foundation, PPI rose 0.2% m/m. Import costs rose 0.7% m/m. Export costs fell -0.2% m/m. Producer value development remained under the newest shopper inflation determine for the third month. Client value development excluding recent meals edged as much as 2.9% in October.

JPY has seen a pointy decline, falling under 180.00 in opposition to GBP, fuelled by a shift in investor sentiment concerning a possible fee hike from the BOJ. Traders, who initially guess on a possible BOJ fee hike, are actually reconsidering their positions. BOJ officers seem like in no hurry to implement coverage tightening, until there may be clear proof of considerable wage development that helps sustainable inflation. This cautious strategy has buyers questioning the timing and extent of future coverage changes. This, in flip, might imply that the yen’s strengthening is just momentary.

The latest surge within the Yen was triggered by Governor Kazuo Ueda’s feedback, which signalled the potential for the central financial institution abandoning its damaging rate of interest coverage sooner than anticipated. Nevertheless, this optimism was short-lived as market dynamics rapidly modified.

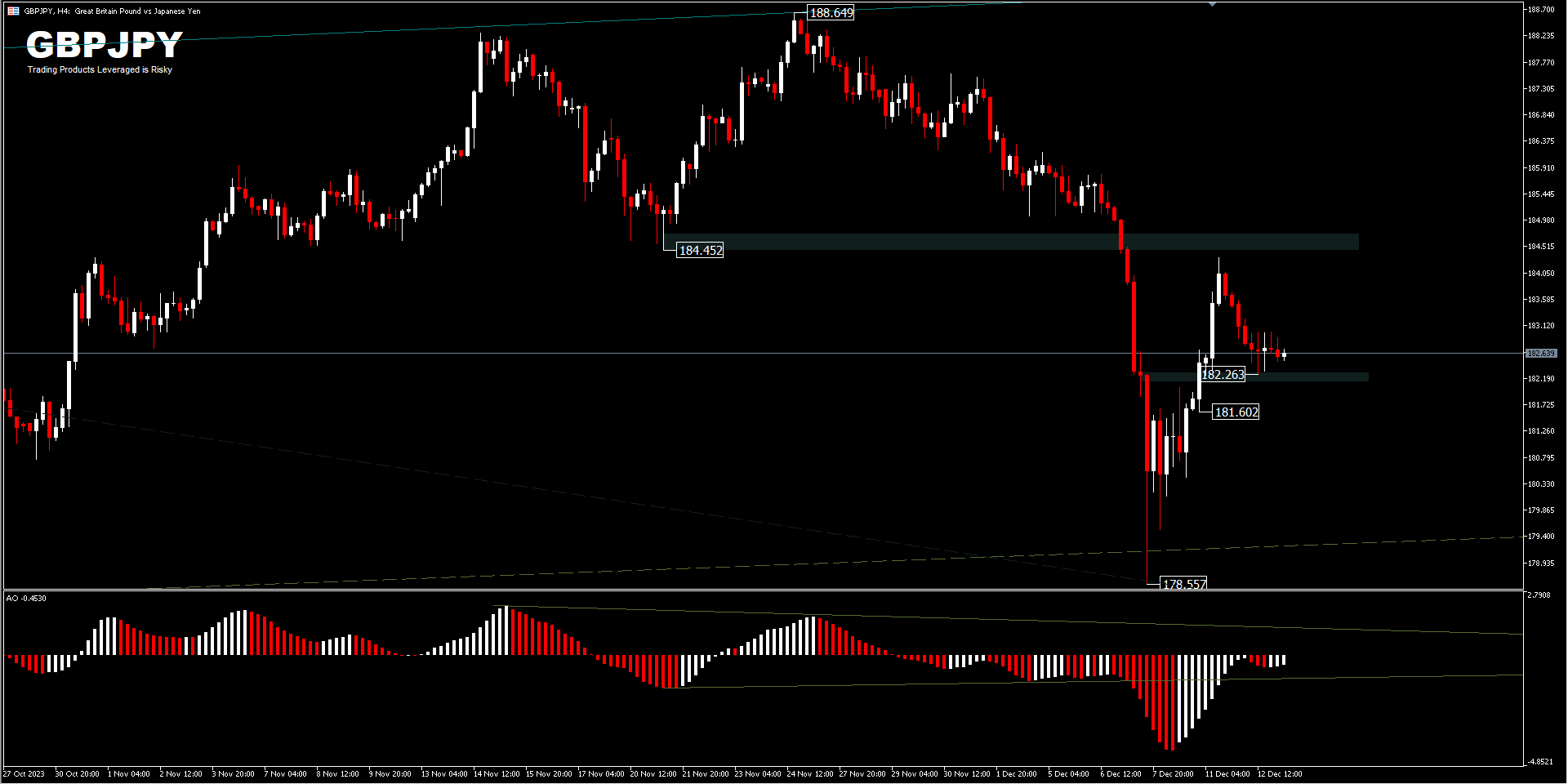

Within the FX market, GBPJPY’s decline was contained on the 200-day EMA and swiftly bounced again to the neckline vary. Technically, the decline that occurred final week doesn’t totally point out a change in pattern, till it’s confirmed that the pair has moved under 176.29 help. If, certainly, that’s the case, then costs are projected to FE100 from 188.64-178.55 drawdown and 184.31 at 174.22. In the meanwhile, nonetheless, GBPJPY value stays in an upward value trajectory.

In the meantime, the intraday of the GBPJPY cross pair turned impartial with the present pullback. On the draw back, a break of 182.26 minor help is prone to check 181.60 help and can point out that the rebound is full. The intraday bias will return to the draw back to retest the 178.55 low. The general outlook will stay bearish so long as the 184.45 neckline generated from the double prime sample holds, as in any other case a retest of 188.65 nonetheless stays.

Click on right here to entry our Financial Calendar

Ady Phangestu

Market Analyst – HF Instructional Workplace – Indonesia

Disclaimer: This materials is supplied as a basic advertising and marketing communication for data functions solely and doesn’t represent an impartial funding analysis. Nothing on this communication incorporates, or needs to be thought of as containing, an funding recommendation or an funding advice or a solicitation for the aim of shopping for or promoting of any monetary instrument. All data supplied is gathered from respected sources and any data containing a sign of previous efficiency will not be a assure or dependable indicator of future efficiency. Customers acknowledge that any funding in Leveraged Merchandise is characterised by a sure diploma of uncertainty and that any funding of this nature entails a excessive degree of danger for which the customers are solely accountable and liable. We assume no legal responsibility for any loss arising from any funding made primarily based on the knowledge supplied on this communication. This communication should not be reproduced or additional distributed with out our prior written permission.

[ad_2]

Source link