[ad_1]

Berkshire Hathaway Chairman and CEO, Warren Buffett. Chip Somodevilla

Alongside Vice Chairman and his trusted enterprise associate Charlie Munger, Warren Buffett has reshaped the trajectory of Berkshire Hathaway (BRK.A)(BRK.B) since taking whole management over the corporate in 1965. The corporate has remodeled from a fledgling textile producer into probably the most highly effective funding holdings firm on the planet. Together with its $157 billion money steadiness as of September 30, Berkshire Hathaway’s funding portfolio is price roughly $513 billion as of November 17, 2023.

Munger has had a big impression on Buffett’s investing technique. Quite than shopping for truthful companies at great valuations that his mentor Benjamin Graham taught him, Buffett shifted gears. For many years now, the Oracle of Omaha has stood by the funding philosophy of shopping for great companies at truthful or higher valuations.

One enterprise that is proper up Berkshire Hathaway’s alley is the well-known grocery store chain Kroger (NYSE:KR). The holding firm owns a 7% stake within the retailer price $2.1 billion. For the primary time in over 4 years, let’s dig into what Buffett and firm noticed in Kroger and why I nonetheless assume the inventory is a purchase.

DK Zen Analysis Terminal

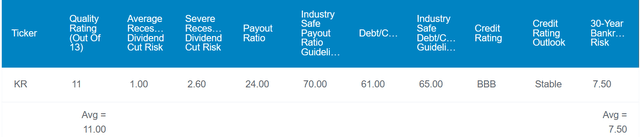

Kroger’s 2.7% dividend yield clocks in at almost twice the 1.5% yield of the S&P 500 index (SP500). As a testomony to simply how low cost we’ll discover this inventory to be, this above-average yield is not as a result of an elevated payout ratio, both. Kroger’s 24% EPS payout ratio is a couple of third of the 70% payout ratio that credit standing businesses take into account to be protected for the grocery retailer business.

The corporate additionally seems to be in superb monetary well being: Kroger’s 61% debt-to-capital ratio is just under the 65% debt-to-capital ratio that score businesses wish to see from its business. That is why the corporate earns an investment-grade BBB credit standing from S&P on a steady outlook. That suggests Kroger is at a nonetheless moderately low 7.5% chance of going bankrupt within the subsequent 30 years per Dividend Kings.

For these causes, it is not onerous to see why Dividend Kings estimates the danger of a dividend reduce from Kroger in a median recession is simply 1%.

DK Zen Analysis Terminal

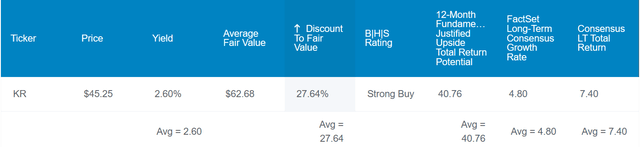

Whereas Kroger’s sound fundamentals are encouraging, the present valuation is equally engaging. Based mostly on historic dividend yield and P/E ratio, the inventory’s historic truthful worth is $63 a share. That implies Kroger is 33% discounted relative to truthful worth from its present $42 share worth (as of November 17, 2023).

If Kroger delivers earnings progress according to the consensus and returns to truthful worth, whole returns within the coming 10 years might be as follows:

2.7% yield + 4.8% FactSet Analysis annual earnings progress consensus + a 4% annual valuation increase = 11.5% annual whole return potential or a cumulative 197% whole return versus the 9% annual whole return potential of the S&P or a cumulative 137% whole return

Strong Outcomes For The Second Quarter

Based on Kroger, the typical individual makes 221 selections associated to meals every day. The corporate’s 2,700-plus supermarkets and multi-department shops in 35 states and the District of Columbia make it a number one choice for customers who need recent and reasonably priced meals selections. Kroger’s most well-known retailer banners embrace Choose ‘n Save, Metro Market, and the eponymous Kroger. This in depth presence of iconic shops all through the USA coupled with its rising private-label enterprise makes the corporate attention-grabbing.

Kroger FY Q2 2023 Earnings Press Launch

Kroger’s gross sales decreased by 2.3% year-over-year to $33.9 billion for the second quarter ended August 12, 2023. A gross sales decline is rarely what buyers need to see from their funding holdings. However these outcomes are removed from discouraging.

It isn’t a secret that though gasoline costs stay elevated in comparison with the place they had been just a few years in the past, they’re much decrease than they had been in Q2 2022. This was behind the general decline in Kroger’s gross sales through the second quarter. Factoring this out of the equation, gross sales would have grown by 1% in that interval.

Final September, Kroger introduced that it was ending its pharmacy supplier settlement with Specific Scripts. This was as a result of what the previous known as an unsustainable drug pricing mannequin. When excluding this impression on Kroger’s pharmaceutical enterprise from outcomes, gross sales would have elevated by 2.6% for the second quarter.

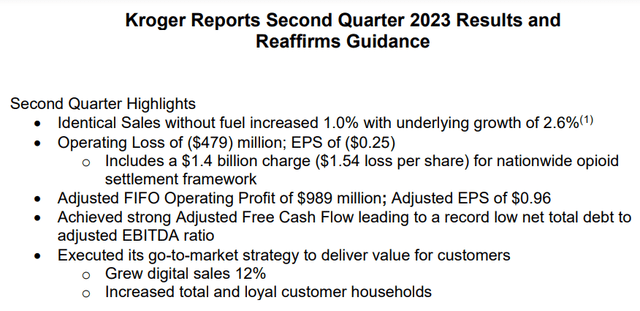

The corporate’s working loss per share was $0.25 through the second quarter. However backing out a $1.4 billion cost from the corporate’s settlement for its alleged function within the nationwide opioid disaster and merger prices with Albertsons (ACI), adjusted EPS was $0.96. This was up 6.7% over the year-ago interval.

Kroger’s monetary place was strong as nicely. As of August 12, the corporate’s internet whole debt to adjusted EBITDA ratio was 1.3 (monetary information sourced from Kroger Q2 2023 Earnings Press Launch). Nonetheless, it’s price noting that upon the closing of its merger with Albertsons anticipated in early 2024, leverage shall be going up past Kroger’s focused ratio of between 2.3 and a pair of.5. The excellent news is that with $1 billion in anticipated annual price efficiencies and aggressive deleveraging, the corporate thinks it may possibly return to its focused leverage ratio inside 18 to 24 months of closing.

The Dividend Has Room To Run

Having hiked its quarterly dividend per share by 107% up to now 5 years to the present charge of $0.29, Kroger has been an outstanding dividend progress inventory. The merger with Albertsons will certainly sluggish this dividend progress charge for the foreseeable future.

However make no mistake about it, Kroger is a free money movement machine that may afford to steadiness debt compensation and a rising dividend. It is because Kroger has generated $2.4 billion in free money movement by way of the primary two quarters of this fiscal yr. In opposition to the $376 million in dividends paid throughout that point, that is only a 15.6% free money movement payout ratio (particulars in accordance with web page 5 of 39 of Kroger’s 10-Q submitting). That is why I’d be stunned if dividend progress wasn’t no less than within the mid- single-digits yearly for the subsequent two to 3 years earlier than accelerating once more.

Dangers To Contemplate

Kroger is a superb enterprise, nevertheless it nonetheless has dangers that buyers ought to pay attention to earlier than shopping for.

As is the case with mega-mergers, warning is at all times warranted. That is as a result of even offers that make sense on paper similar to this one with Albertsons do not at all times pan out. On the small likelihood that Kroger cannot understand its price synergies as anticipated, the deal might not create worth for shareholders.

One other danger to Kroger is that it contributes to a number of multi-employer pension plans. If investments inside these pensions do not stay as much as expectations, the corporate may need to make extra contributions to fund any shortfalls. That might weigh on Kroger’s monetary outcomes.

Abstract: Kroger Is A Buffett-Owned Discount

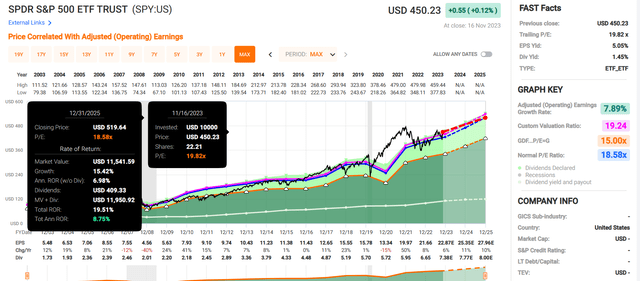

FAST Graphs, FactSet

FAST Graphs, FactSet

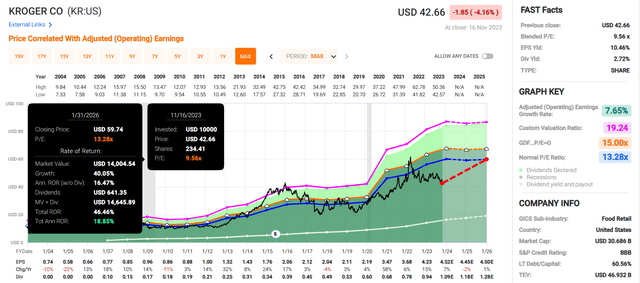

For dividend progress buyers who can deal with its danger profile, Kroger might be a wise purchase. The corporate’s 9.6 blended P/E ratio is way under the traditional P/E ratio of 13.3. If Kroger grows as anticipated within the subsequent two years and returns to truthful worth, it may produce 19% annual whole returns by way of early 2026.

That is greater than double the 8.8% annual whole returns which can be anticipated from the SPDR S&P 500 ETF Belief (SPY) in that point. That is why I consider shares of Kroger are at the moment a purchase.

[ad_2]

Source link