[ad_1]

tiero

Please observe that this week is the quarterly Grasp Record fundamentals replace. Each quarter, after earnings, I replace all essential fundamentals for the DK 500 Grasp Record, which allows valuation-based scores to function routinely in actual time.

Thus, that is the motive for only one article this week.

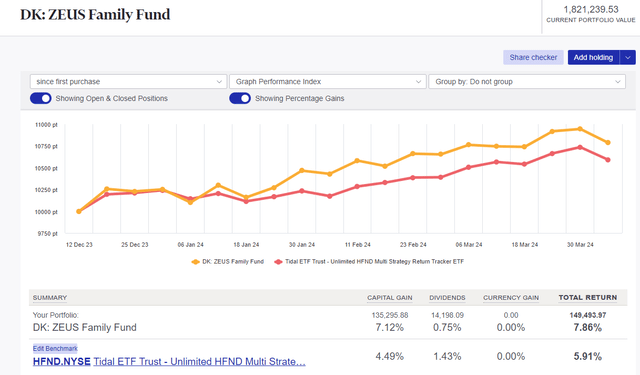

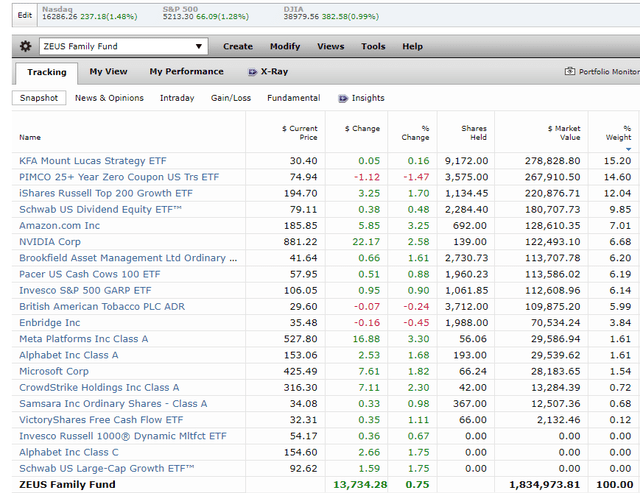

This is my ZEUS Household fund holdings’ weekly financial replace and actionable concept.

ZEUS Household Fund Abstract: A Unhealthy However Fully Anticipated Week

This week, rising rates of interest prompted the market to expertise a micro dip, and it is important at all times to make use of percentages to maintain issues in context.

ZEUS Charity Hedge Fund

Portfolio Worth $1,821,240 Historic Draw back Seize 0.6266 Report Excessive Date 4/1/24 Report Excessive Revenue $156,576 Under Report Revenue $38,928.13 Distance From Report Excessive 2.14% Whole Revenue $117,648 Month-to-month Revenue $28,644.70 Weekly Revenue $7,161.17 Each day Revenue $1,023.02 Hourly Revenue $42.63 Minute Revenue $0.71 Second Revenue $0.01 Click on to enlarge

When the fund launched in December, Morningstar estimated a possible 26% essentially justified acquire within the first 12 months, equating to roughly $480,000 in earnings or roughly $9,230 weekly.

For the general technique, together with outdoors cash accessible to speculate later. 14% undervalued = 16% upside to honest worth + 8.5% weighted earnings progress +3.5% dividends

What’s so outstanding is that the ZEUS Household Fund has been following the essentially justified whole return potential path like a rail.

That is very uncommon, because the inventory market is understood for its volatility, which is why shares are thought-about a “danger asset.”

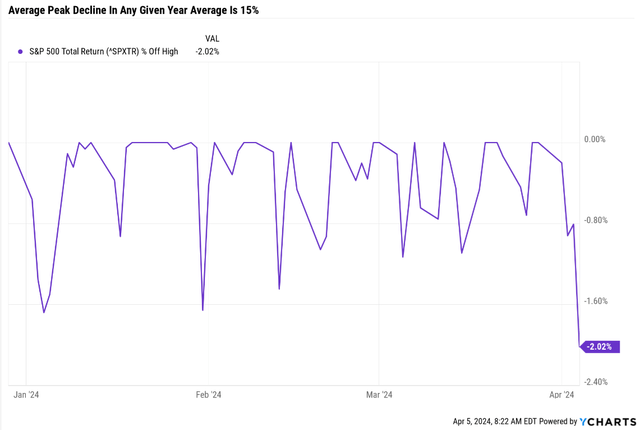

Ychart

The S&P has skilled solely a 2% peak decline this 12 months.

The typical historic intra-year decline is 15%.

Shares are up 76% of the time in any given 12 months, and in any given 12 months, they common a 15% peak decline sooner or later on the best way to traditionally common 10% positive factors.

The typical annual return in an up 12 months is 22%, and the typical decline in a down 12 months is -12%.

Sharesights

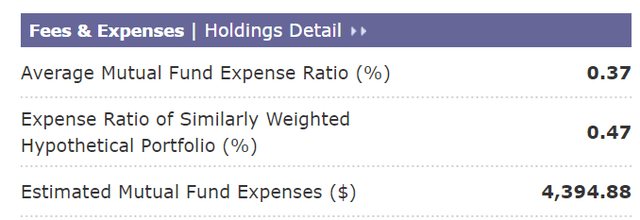

HFND is the DBMF of hedge fund ETFs. It is run by former Bridgewater head of Macro analysis Bob Elliott, who makes use of AI machine-learning algos to estimate your entire hedge fund business’s positioning in a single “low-cost” ETF.

A 2% expense ratio is 60% decrease than what the hedge fund business prices it is 5X increased than the 0.38% that my household is paying for ZEUS.

Morningstar

In HFND, we would be paying $37,000 in annual charges.

Dividend King ZEUS Portfolio Tracker

HFND is designed to earn 8% post-fee whole returns in the long run, beating the 60-40’s historic 7% with barely decrease volatility.

ZEUS Household fund is designed to generate SCHD-like yields with far superior returns to the hedge fund business and 8X decrease charges.

I am making an attempt to show that the hedge fund business’s use of complicated methods, like world macro, lengthy/quick, personal credit score, event-driven investing, and so on., is pointless for good outcomes.

Traditionally, 67% of hedge fund web earnings come from development following, in line with AQR.

Simplicity is the last word sophistitication.” – Lenardi Da Vinci

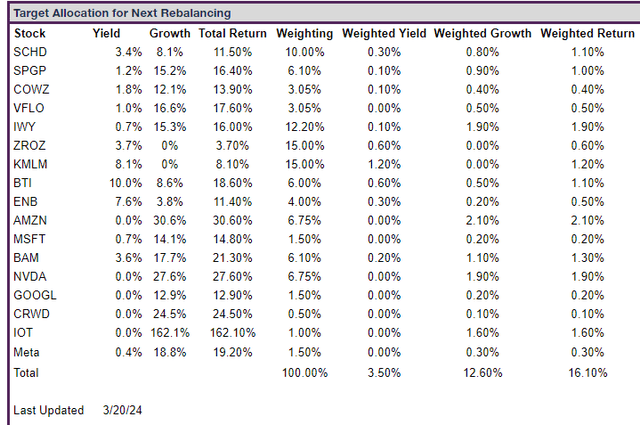

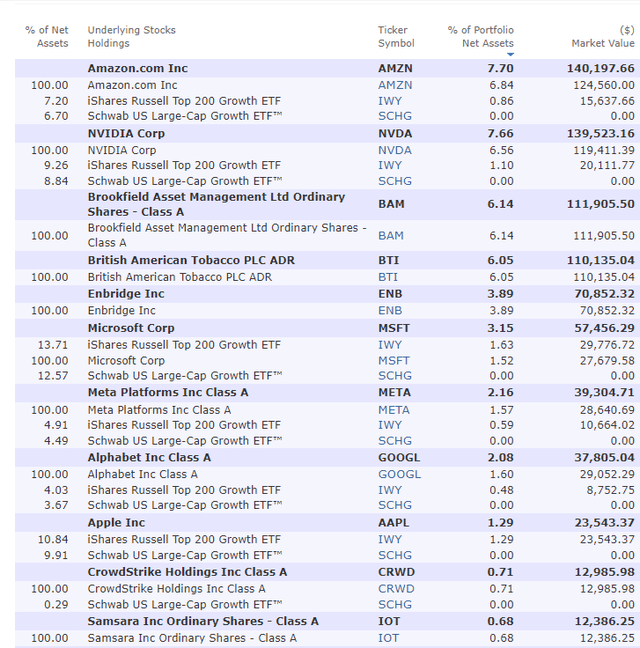

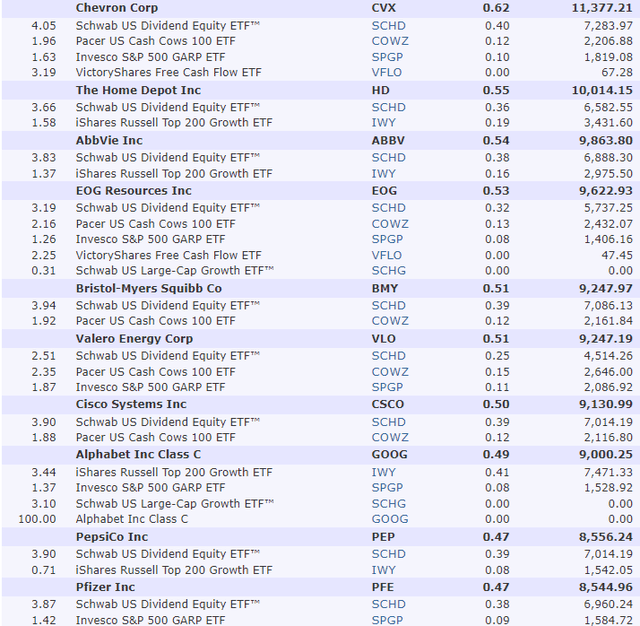

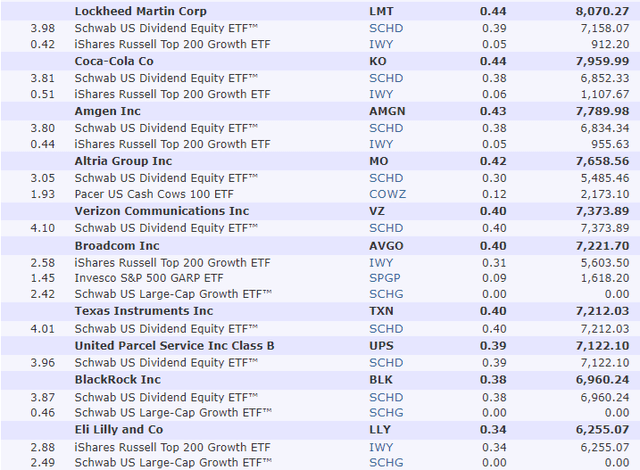

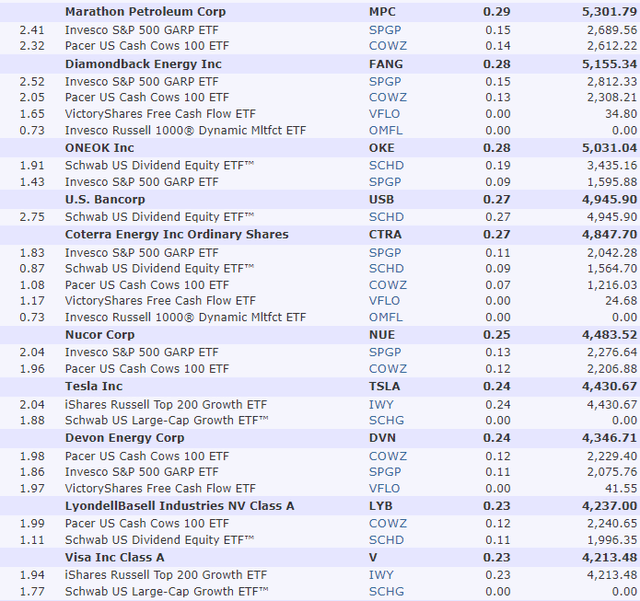

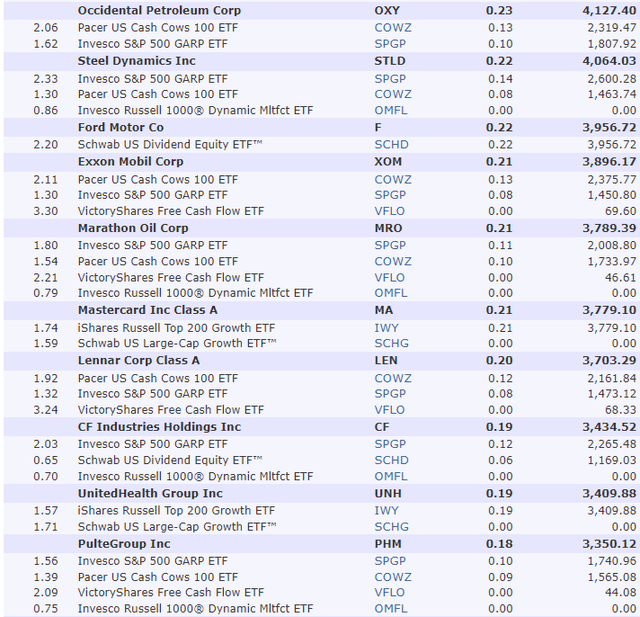

What ZEUS Seems to be Like Now

Morningstar

10 Largest Holdings: 41.32% Of Portfolio vs. 32% S&P 500

20 Largest Holdings: 47.19% Of Portfolio vs. 42.1% S&P 500

30 Largest Holdings: 51.63% Of Portfolio

40 Largest Holdings: 54.21% Of Portfolio

50 Largest Holdings: 56.27% Of Portfolio

Morningstar

Morningstar

Morningstar

Morningstar

Morningstar

Morningstar

We’re invested in 4 asset courses courtesy of ETFs like KMLM.

Properly balanced between progress, worth, yield, and 17% publicity to small and mid-cap firms.

Which profit most from financial accelerations.

Morningstar

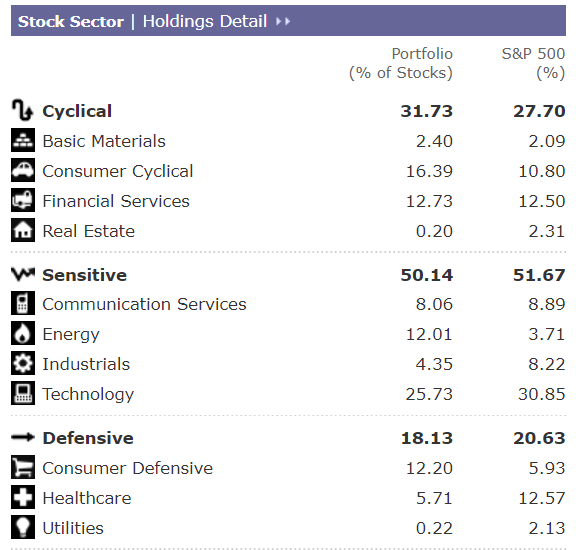

Tilted towards tech however good sector diversification total.

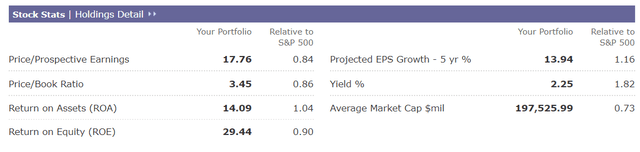

Inventory Fundamentals

Morningstar

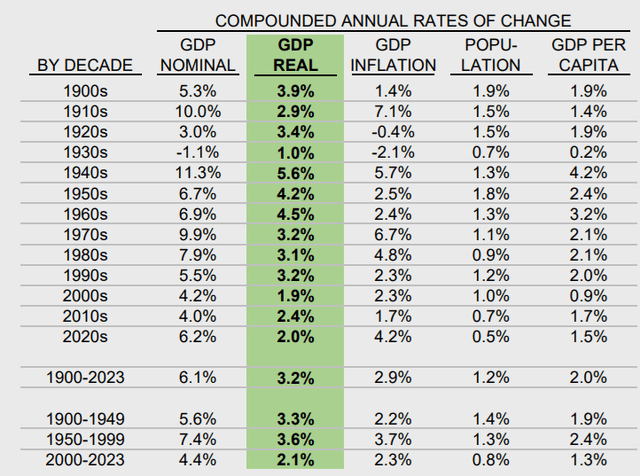

For context, the S&P is buying and selling at a ahead PE of 21.1, and Morningstar’s analysts estimate its earnings will develop by 12% over the following 5 years.

S&P PEG ratio: 1.76 (1.18 cash-adjusted) 20-year common PEG: 3.54 (2.17 cash-adjusted)

ZEUS Household is buying and selling at a PEG of 1.27 and adjusted for money on our firm’s stability sheet it falls to underneath 1.

Progress at an inexpensive value or GARP.

Market Outlook/Valuation: What The Bears Are Getting Incorrect

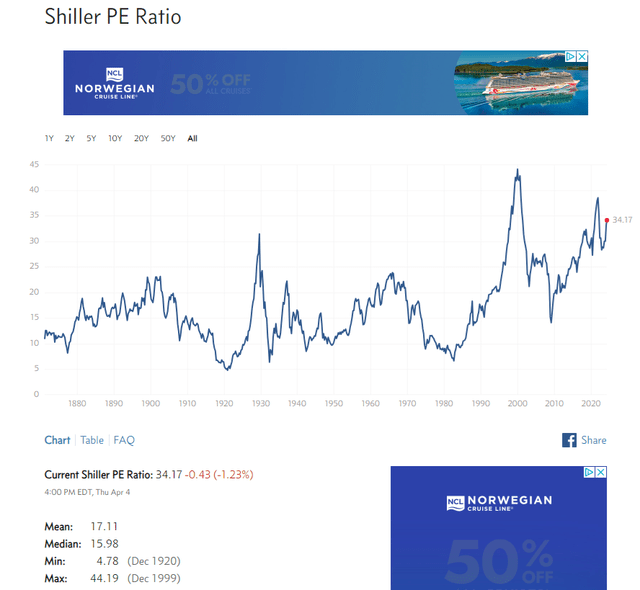

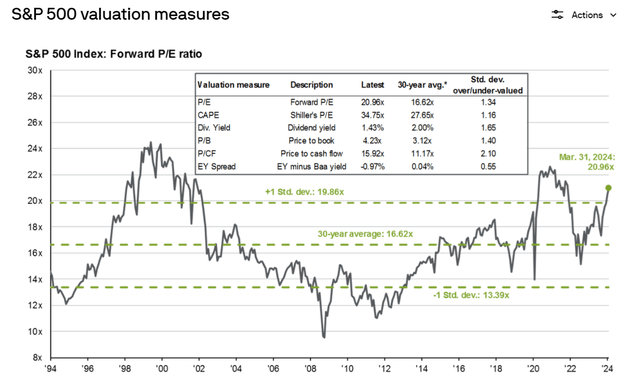

You would possibly hear about Shiller PE, PE, ebook worth, dividend yield, and plenty of valuation metrics.

Multipl

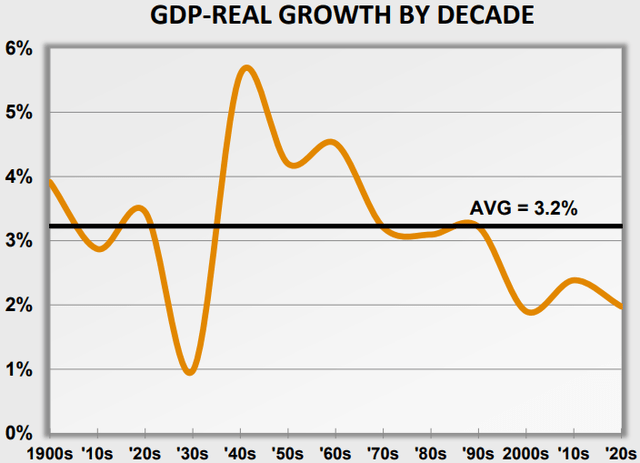

Wanting again to 1871 for a way of the place US shares ought to be valued right this moment is inaccurate for a lot of causes.

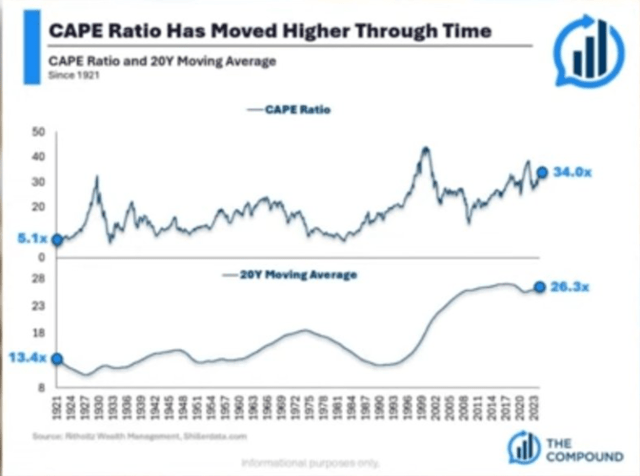

Ritholtz Wealth Administration

Guess what the 20-year common CAPE is? 26X, lots much less scary.

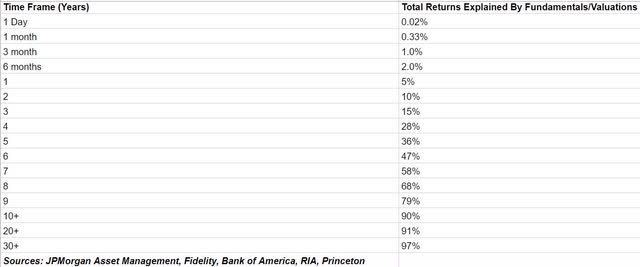

Dividend Kings S&P 500 Valuation Software

And what’s the proportion of returns defined by fundamentals over 20 years? 91%.

In different phrases, when you get to 10-30 years, you’ve sufficient historic knowledge to make a 90%-97% likelihood that regardless of the valuations we have seen are the market-determined honest worth shares will return to.

The likelihood that bubbles can final 30+ years is 3% The likelihood bubble can final ten years is 10%

Ritholtz Wealth Administration

US inventory PEs have been rising for many years, lengthy earlier than charges peaked in 1980 and trended decrease for 40 years.

The rise of retail buyers. The introduction of 401Ks within the Nineteen Eighties (automated circulation of money into shares each two weeks). International buyers are actually capable of purchase US shares. Rise of huge tech (wider moat, increased margin, increased high quality firms).

Ritholtz Wealth Administration

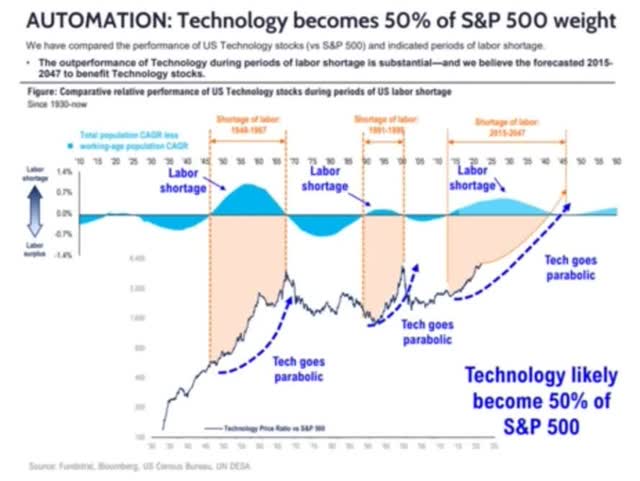

Based on Tom Lee at Fundastrat, a secular labor scarcity by 2047 might trigger know-how, whose AI productiveness increase will clear up that scarcity, to develop earnings so rapidly that by 2047, the S&P will go from 30% know-how to 50%.

Together with GOOG, Meta, and AMZN (which aren’t formally tech shares), probably round 75%.

In 1900, 66% of the US inventory market was railroads, not industrials, simply railroads.

Tech is extra worthwhile than industrials, and right this moment’s tech shares supply utility-like services and products that create month-to-month recurring income. That is why S&P PEs rising steadily are each anticipated and justified by fundamentals.

Why Skilled Cash Managers Aren’t Anxious About An Imminent Crash

JPMorgan Asset Administration

Shares look much less overvalued when considered in additional affordable 10—to 30-year time frames (90% to 97% statistically vital).

Pacer

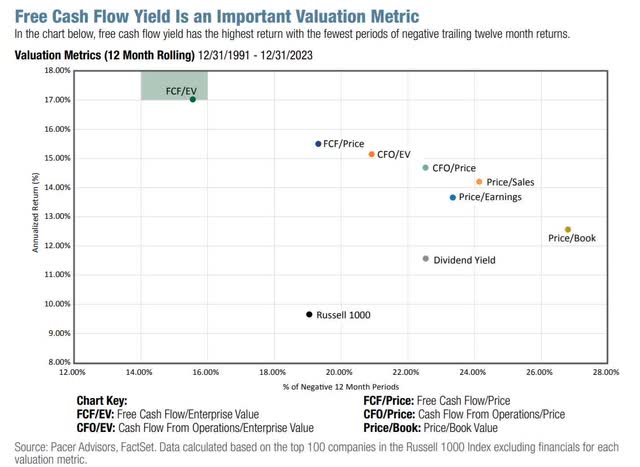

Once we take a look at probably the most correct metric of the final 33 years, enterprise worth/money circulation, the market is barely overvalued.

Enterprise Worth = market cap + debt – money (the price of shopping for the corporate)

S&P EV/EBITDA

Week 14 % Of Yr Executed 2024 Weighting 2025 Weighting 26.92% 73.08% 26.92% Ahead S&P EV/EBITDA (Money-Adjusted Earnings) 10-Yr Common (90% statistical significance) Market Overvaluation 14.00 13.46 4.41% S&P Truthful Worth Decline To Truthful Worth 4,948.27 4.22% Click on to enlarge

(Supply: Dividend Kings S&P Valuation Software)

And guess what? There’s one other very important issue to contemplate in valuation, as Peter Lynch’s progress at an inexpensive value factors out.

PEG ratio = PE (or any EV/money circulation)/future earnings progress

The 25-year common EV/EBITDA/Progress (cash-adjusted PEG) for the S&P is 2.17.

In the present day, the S&P’s EPS progress estimate from Morningstar is 12%, 2X the historic charge (and 3X sooner than the final 25 years).

1.17 cash-adjusted PEG vs. 2.17 25-year common.

Morningstar’s analysts are bullish on the S&P as a result of rise of huge tech, which is rising at 15%.

FactSet Backside-Up Progress Consensus (3,500 Analysts)

FactSet Analysis Terminal

The FactSet bottom-up consensus (92% accuracy charge during the last 20 years, in line with FactSet’s John Butters) is for 12.5% EPS progress by 2026, just like Morningstar’s bottom-up analyst estimate.

Prime-down estimate: Analysts “guess” S&P earnings progress based mostly on the financial system. Backside-up: Take each firm within the S&P 500 EPS consensus progress and weight by the identical weighting within the S&P.

May earnings progress be incorrect? Certain. However even when the S&P’s earnings develop 50% as quick as anticipated, the S&P will nonetheless solely be about 4% traditionally overvalued.

Financial Replace: One other Blowout Jobs Report

FactSet Analysis Terminal

3-month rolling common: 260K. Final month’s revised estimate: 270K. This month: 303K.

Moody’s considers 225K month-to-month jobs in step with 1.8% GDP progress and 250K a “robust financial system.”

Wage progress got here in at 4.1% year-over-year, forward of CPI and Trulfation’s real-time inflation estimate.

Trulfation

Truflation makes use of 10 million knowledge factors, up to date each day, to estimate real-time inflation. 97% correlation with CPI since 2012.

The Fed desires to see wage progress of three.5% and inflation of two% for a 1.5% actual wage progress.

Actual wage progress: wage progress – inflation.

The month-to-month wage progress of 0.3% is 3.7%, approaching the Fed’s goal.

Wages – productiveness = inflation. 4.1% YOY – 3.2% productiveness = 0.9% CPI potential (if right this moment’s knowledge continues to carry). 3.7% annualized wage progress – 3.2% productiveness = 0.5% CPI potential.

Digging Into The Numbers: What The Media Would not Inform You Issues That Does

Development jobs (a number one indicator of recession)

Development added 39,000 jobs in March, about double the typical month-to-month acquire of 19,000 over the prior 12 months. Over the month, employment elevated in nonresidential specialty commerce contractors (+16,000).” – Bureau of Labor Statistics

Essentially the most economically delicate industries are producing jobs at a wholesome charge. The housing market, normally, seems to be recovering, which is a tailwind for the financial system.

Word 16K month-to-month development job progress with 8% mortgages. The genius of American capitalism is we adapt and overcome and simply continue to grow within the face of what would possibly appear to be overwhelming odds.

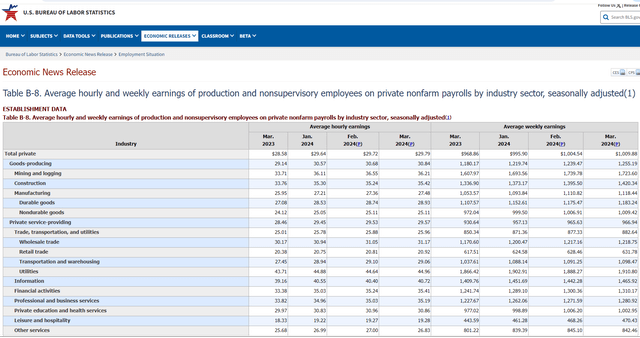

Non-supervisory wages (80% of Individuals)

Bureau of Labor Statistics

4.25% annual wage progress and 4.25% weekly earnings (wages X hours labored).

So, it’s barely higher than 4.1% total wage progress and three.7% annualized.

The Fed will likely be blissful that is trending decrease however sooner than inflation.

3-Month rolling common of job progress

The change in whole nonfarm payroll employment for January was revised up by 27,000, from +229,000 to +256,000, and the change for February was revised down by 5,000, from +275,000 to +270,000. With these revisions, employment in January and February mixed is 22,000 increased than beforehand reported.” – Bureau of Labor Statistics

The three-month rolling common on job progress is now 277K, trending increased.

608K in 2021 (Pandemic restoration) 400K in 2022 (additionally Pandemic restoration) 258K in 2023 (earnings, housing, industrial recession, highest charges in 20 years) 277K in 2024 YTD vs 171K 2010 to 2020

We’re creating web jobs at a charge of three.3 million per 12 months, 1.2 million extra annual web jobs than from 2010 to 2020.

We’re creating jobs at a 38% sooner progress charge than Pre-pandemic ranges.

What does this probably imply for GDP progress?

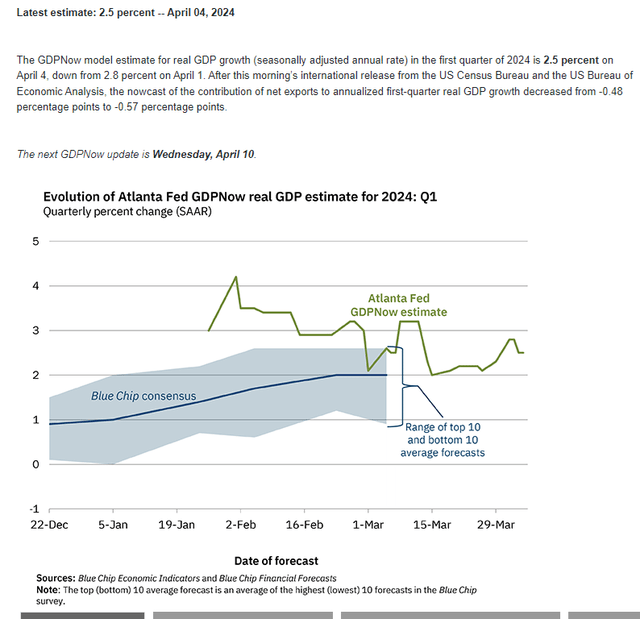

Atlanta Fed

The blue-chip economist consensus thinks progress is at the moment 2%, and the Atlanta Fed’s mannequin says 2.5%.

Not together with right this moment’s blowout jobs report.

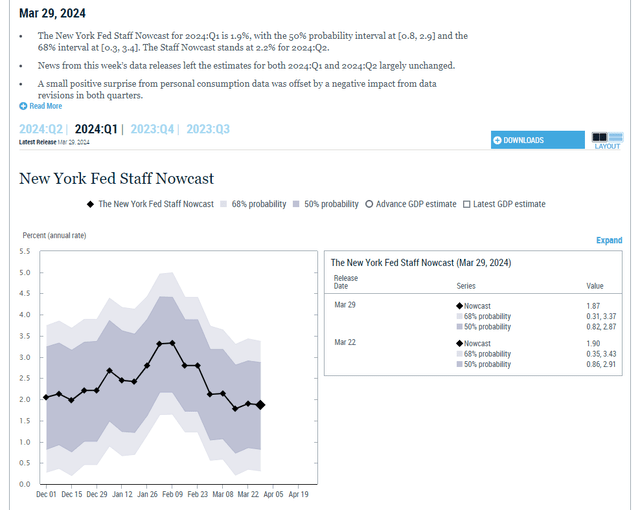

New York Fed

The New York Fed’s mannequin additionally estimates round 2% progress this quarter.

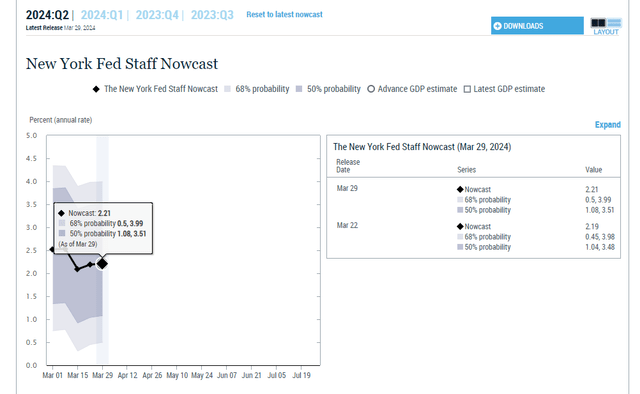

New York Fed

The New York Fed expects a modest 0.3% GDP progress acceleration in Q2, and that is earlier than right this moment’s blowout jobs report is factored in.

How briskly might GDP progress attain based mostly on right this moment’s fundamentals?

The present web migration charge for the U.S. in 2024 is 2.768 per 1000 inhabitants, a 0.73% enhance from 2023.

The labor power is rising at 0.6% per 12 months, 2X the speed JPMorgan anticipated this decade.

GDP progress = Productiveness progress (3.2%) + labor power progress charge (0.6%) = 3.8%

In different phrases, if present productiveness progress charges maintain and our workforce retains rising on the present charge (folks rejoining the workforce or immigrants getting jobs), the US financial system might proceed accelerating from 2% to 2.5% progress now to three.8%.

Crestmont Analysis

Crestmont Analysis

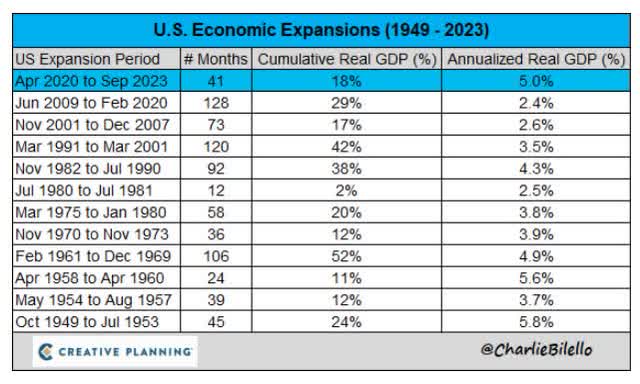

How has the US financial system been rising for the reason that Pandemic ended? The quickest charge in 83 years.

Charlie Bilello

And whereas progress is prone to gradual, McKinsey thinks that GDP progress would possibly speed up from 4.2% to six.5% due to AI.

Most individuals overestimate what they’ll obtain in a 12 months and underestimate what they’ll obtain in ten years.” – Invoice Gates

What about inflation and rates of interest? What does a possible re-acceleration of US financial progress to three%, and even 4% or extra, imply for inflation and rates of interest?

Inflation/Curiosity Fee Replace: PCE Report As Anticipated However Bond Market Reacting To Hawkish Fed Speak

Though the market was closed for Easter final Friday, the Private Consumption Expenditure (PCE) inflation report was launched.

FactSet Analysis Terminal

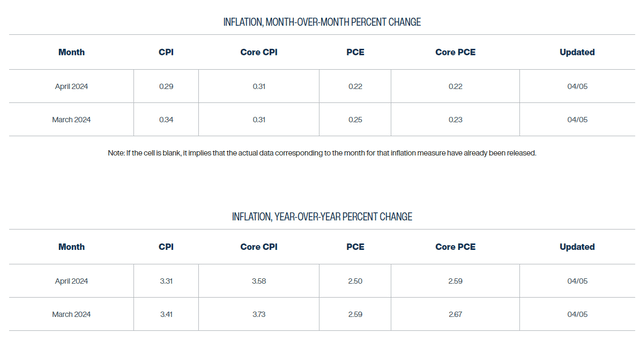

As anticipated, the core PCE was 2.8% final month, down from 2.9% the earlier month.

Cleveland Fed Each day Inflation Mannequin

Cleveland Fed

The Cleveland Fed’s real-time mannequin predicts that Core PCE will fall to 2.7% on the finish of April and a pair of.6% on the finish of Might.

As Powell has indicated, the month-over-month charge is anticipated to maintain drifting decrease at a crawl however probably give the Fed the quilt it wants to start out reducing later this 12 months.

Powell advised the Senate he desires to chop in July. The Fed Chairman often will get his method.

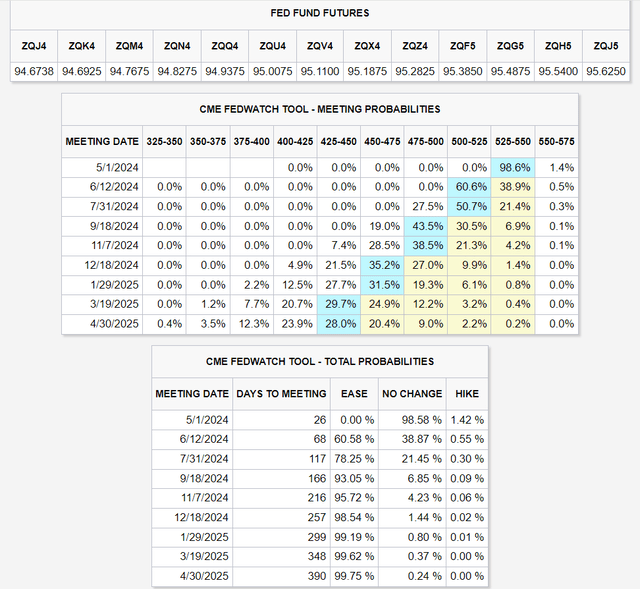

CME Group

The bond market is beginning to value within the chance that the Fed would not reduce till September.

Since 2008, in line with the Fed futures market, the Fed has at all times finished what was an 80%-plus likelihood.

The bond market thinks three cuts are coming this 12 months, simply because the Fed’s Dot plot says.

Fed’s Dot plot exhibits median forecasts for rates of interest by all 19 FOMC members.

There’s now a slight probability that the Fed would possibly hike charges once more, simply 1.4%.

A-credit score = 2.5% danger of chapter The danger of one other Fed hike is 50% lower than House Depot going bankrupt within the subsequent three a long time.

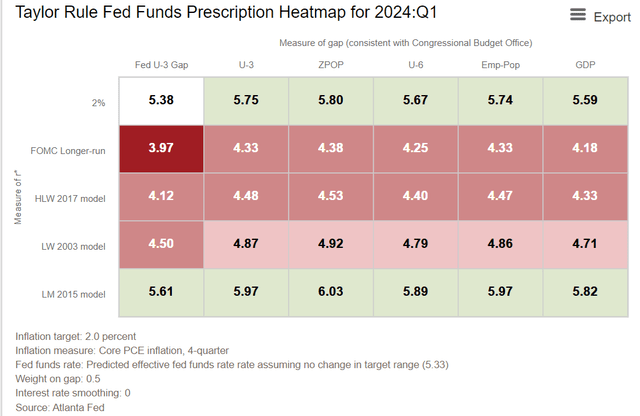

Atlanta Fed

In a “worst case” charge state of affairs, the Fed may need to hike twice and depart charges at 5.75% to six% for years.

This could probably imply that two-year yields would rise to five.5% to six%, 10-year yields would rise to six% to six.5%, and 30-year yields might probably attain 7%.

Would not that be catastrophic for shares? No, not going.

Investing Lesson Of The Week: Good Information Is All the time And Endlessly Good Information

There isn’t any wage-price spiral or vital commodity disruption just like the Seventies twin oil shocks.

The one method inflation stays above 3% or hits 4% (forcing the Fed to hike to round 6% and maintain charges there) is a booming financial system.

Productiveness progress from know-how is deflationary.

So, the place would possibly inflation come from?

70% of the financial system is shopper spending, and shoppers are spending.

Pandemic plus worst inflation in 42 years, plus quickest rate of interest will increase in a long time, plus 8% mortgages plus worst bond bear market in historical past, two bear markets in 4 years…and 25% annual returns for purchase and maintain buyers.

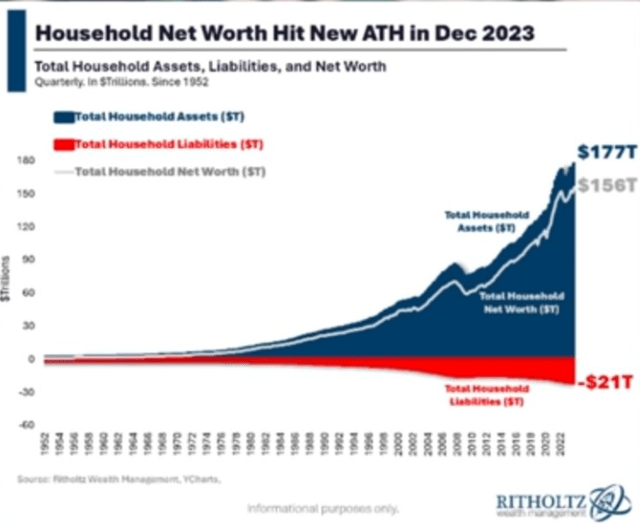

Ritholtz Wealth Administration

That is the genius of American capitalism in all its splendor.

Ritholtz Wealth Administration

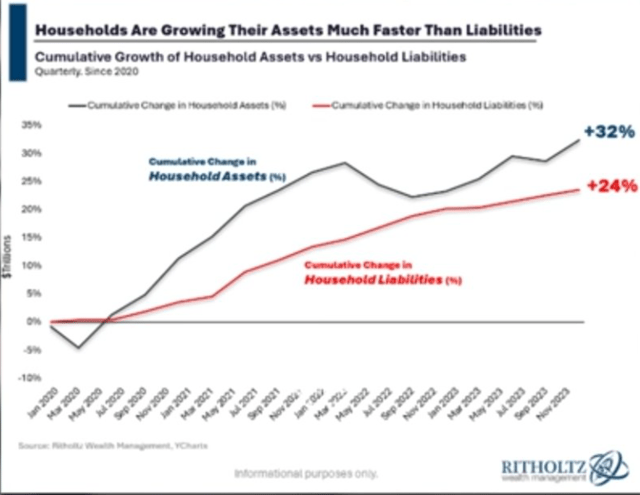

Individuals are wealthier than ever, and the job market is the most effective since 1951 and appears to be getting stronger.

Internet price is rising at an accelerating charge, together with $33 trillion in residence fairness that, when mortgage charges lastly do fall, might unleash trillions in cash-out refinancing and House Fairness Strains of Credit score borrowing.

If US shoppers borrow 1% of their residence fairness, $330 billion = 1.5% GDP increase.

Ritholtz Wealth Administration

$33 trillion in residence fairness and $57 trillion in inventory market property, all of which shoppers can borrow towards, regardless that charges are excessive.

Do not let anybody let you know the financial system ought to weaken so charges come down.

Each day Shot

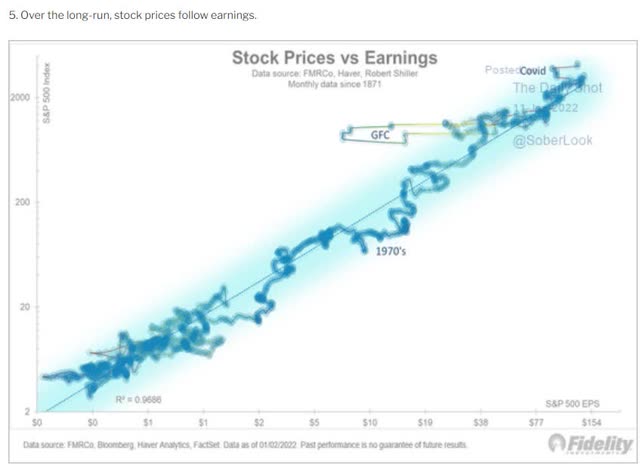

Since 1991, together with the tech bubble and 15 years of “free cash without end,” 97% of S&P returns are defined by dividends and earnings progress.

Since 2010, 87% of market positive factors have been defined by fundamentals.

Each day Shot

Since earnings and dividends clarify 1871, 97% of US inventory returns.

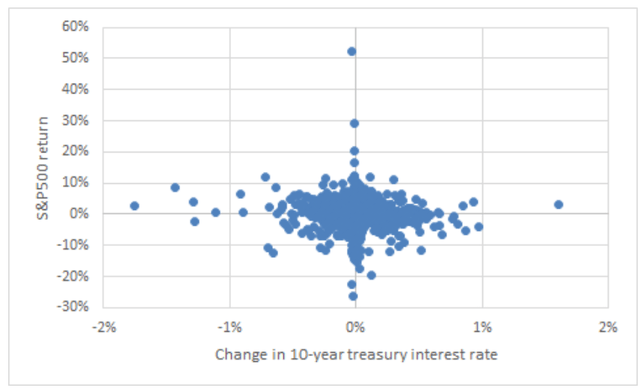

How essential are rates of interest? The ten-year yield is a proxy for long-term “risk-free” rates of interest, which mortgage charges and company borrowing prices benchmark towards.

Over the previous 60 years there’s mainly no relationship between the typical degree of yields and S&P 500 returns, at the very least at a quarterly frequency,” says Stuart Kaiser, head of fairness buying and selling technique at Citi.” – Reuters

Paris Dauphine College

Merchants care about charges; long-term buyers care about earnings.

Excellent news is at all times and without end excellent news for long-term buyers.

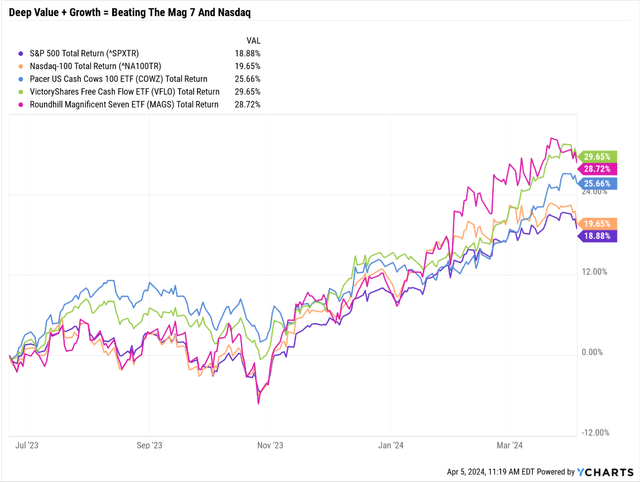

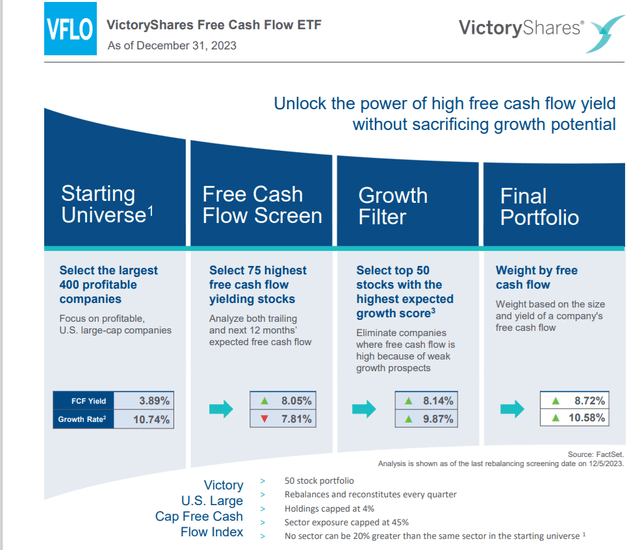

Investing Concept Of The Week: VFLO, My Favourite ETF Concept For In the present day’s Financial Local weather And Past

In an accelerating financial system, deep-value cyclical firms are inclined to do very nicely.

Ycharts

This week, I purchased some extra VictoryShares Free Money Circulation ETF (NASDAQ:VFLO) as a result of it is steadily proving that its deep worth Buffett-style strategy of deep worth high quality and progress is not only outperforming COWZ but additionally the S&P, Nasdaq, and Magazine 7.

VFLO: 5 Causes I am Shopping for This Dividend ETF For My Retirement Portfolio

Right here’s the 30-second elevator pitch for VFLO.

VictoryShares

Since 1991, the technique this ETF has been utilizing has generated 17.6% annual returns or 151X enhance in wealth, in comparison with the S&P’s 9.8% or 22X enhance.

VictoryShares

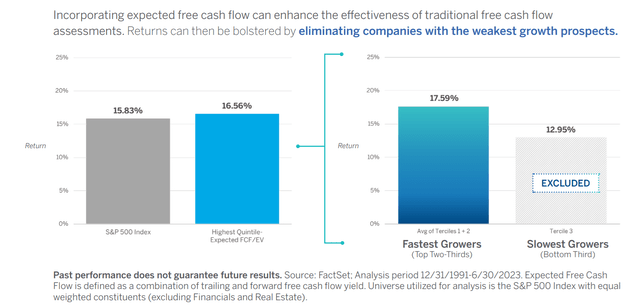

VFLO makes use of a rules-based technique to create a concentrated (although nonetheless diversified sufficient) portfolio of top of the range, deep worth with good progress.

Think about the identical progress because the S&P 400 however with a 3X higher valuation. That secret sauce powered virtually 18% annual returns for 33 years, leading to over 30% since inception.

FactSet Analysis Terminal

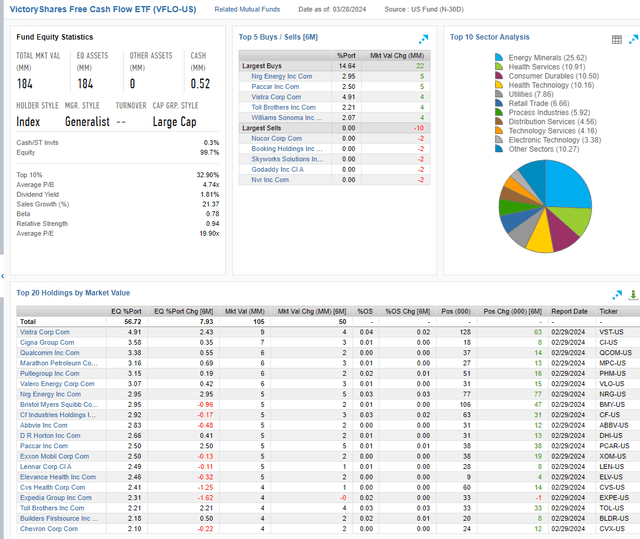

In an accelerating financial system, industries, vitality, and healthcare are prone to thrive, and that is why VFLO is obese.

FactSet Analysis Terminal

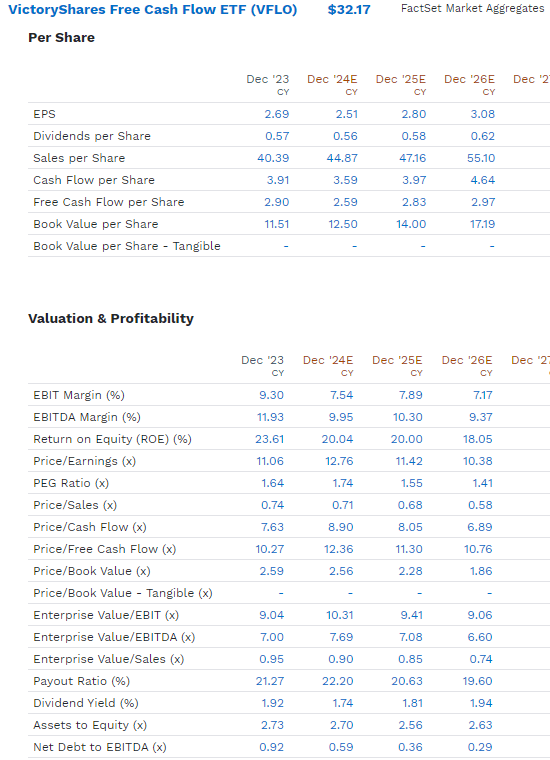

VFLO’s 12-month ahead cash-adjusted PE (EV/EBITDA) is simply over 7X, 33% lower than what personal fairness is paying for firms.

VFLO = 33% cheaper than Billionaires like Mark Cuban are paying for sweetheart offers.

What sort of firms are we getting? Not cigar butts, however firms with nearly no web debt, A-credit scores (typically AA-rated like XOM), and here is the progress charge.

FactSet Analysis Terminal

The present portfolio (turnover is nearly 100% per 12 months) is anticipated to see a minor EPS decline in 2024, however the S&P is forward-looking for 12 months.

Pacer Funds

So, the market is seeing double-digit progress and 7X cash-adjusted earnings, which ends up in a 0.7 PEG ratio, which is even higher than the S&P’s 1.2.

And that is why VLFO’s unbelievable first-year efficiency is greater than 100% justified by fundamentals. There isn’t any bubble, momentum chasing, or FOMO (concern of lacking out) right here.

By definition, VFLO will personal the most effective FCF PEG giant caps, making it my favourite deep worth, high quality, and progress ETF proper now, particularly at this stage of the financial cycle.

Mid-cyle however acceleration in industrials and vitality and cyclical

Conclusion: Lengthy-Time period Investing Is Betting on The US Financial system, A Guess That Is Effectively Supported By In the present day’s Proof

Ritholtz Wealth Administration

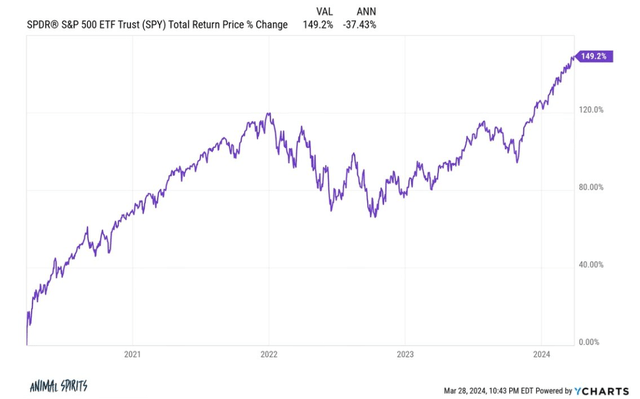

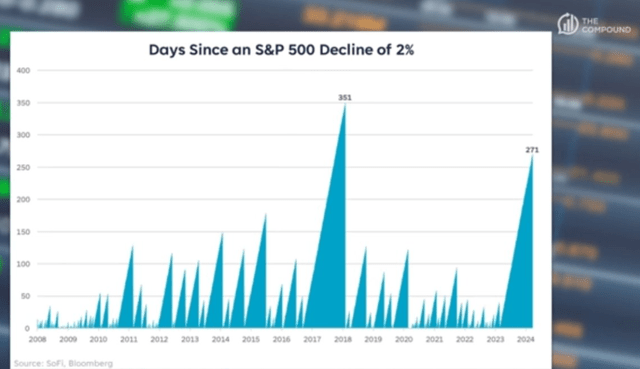

It feels eerie for the inventory market to soar 10% in three months with no declines extra vital than 1.8%.

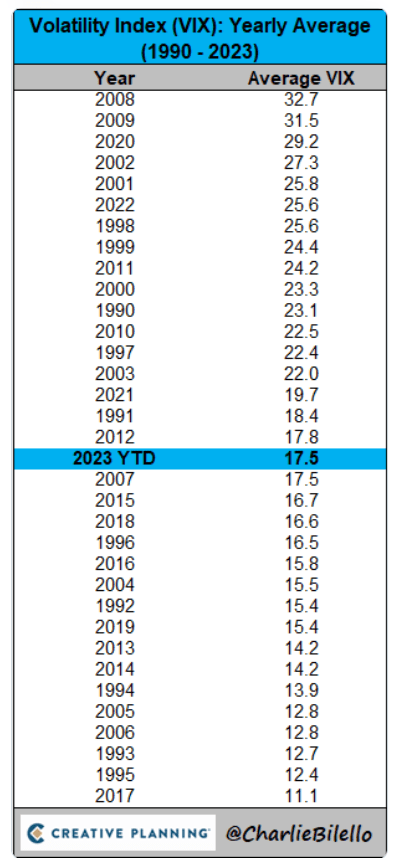

It appears like 2017 when tax-cut euphoria led to a 22% inventory market rally with a median VIX of 11.

Charlie Bilello

That was the bottom volatility in 52 years.

However guess what? The market positive factors have been justified primarily by strong fundamentals.

The financial system seems to be accelerating, with report after report beating to the upside.

Stable jobs and a powerful financial system are at all times and without end excellent news for shares.

If you happen to’re a long-term investor sticking to your personally optimized asset allocation, rates of interest rising should not a priority.

Brief-term merchants? They’re the one ones who’ve to fret about rates of interest. What about the remainder of us?

No one can predict rates of interest, the longer term route of the financial system or the inventory market. Dismiss all such forecasts and focus on what’s really taking place to the businesses by which you’ve invested.”— Peter Lynch

[ad_2]

Source link