[ad_1]

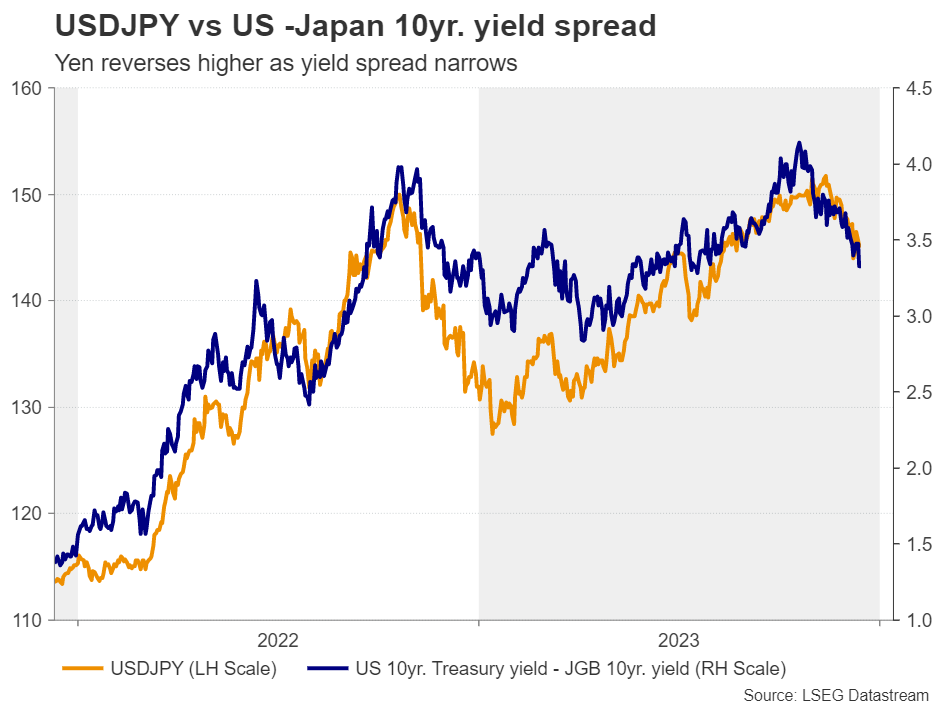

Yen merchants await BoJ resolution for pivot cluesUS core PCE index the spotlight of the US agendaUK CPI numbers to be the pound’s subsequent testLoonie and await Canada’s CPIs and RBA minutesWill BoJ policymakers trace on the finish of unfavourable charges?Following a barrage of central financial institution choices this week the tip credit of main financial coverage choices for 2023 will roll with the BoJ in the course of the Asian session Tuesday. At their final assembly, policymakers determined to permit 10-year JGB yields to rise above 1%. Nevertheless, they didn’t ditch the cap. They simply redefined it from a inflexible ceiling to a reference certain, that means they may intervene within the bond market once more if deemed mandatory. And certainly, that is what they did the day after the choice.

This disenchanted buyers that had been anticipating extra, with the yen tumbling within the aftermath and the next days, with greenback/yen virtually touching its October 2022 excessive of 151.94 on November 13. That mentioned, it was all downhill thereafter with the autumn steepening on December 7 as Governor Ueda talked concerning the doable choices they’ve on interest-rate concentrating on as soon as they finish their unfavourable rate of interest coverage.

Nevertheless, simply the subsequent couple of days, two studies hit the wires, saying that his feedback weren’t supposed to trace at a possible exit timing and that the Financial institution sees the price of ready for extra info as not very excessive. With that in thoughts and given the emphasis the BoJ places on wage progress, policymakers might not go for an imminent shift at this gathering and maybe look forward to April, after the spring wage negotiations.

That doesn’t imply the assembly will move completely unnoticed. Sure, Japan’s GDP information revealed that the economic system contracted by greater than anticipated in Q3, however the Nationwide CPIs revealed that inflation continued to speed up in October which will increase the probability for companies and labor unions to agree on one other spherical of sturdy pay hikes subsequent yr. Thus, even the slightest indication that rates of interest may exit unfavourable territory in April might add extra gas to the yen’s engines, particularly with the market believing that the Fed will minimize rates of interest by round 150bps subsequent yr.

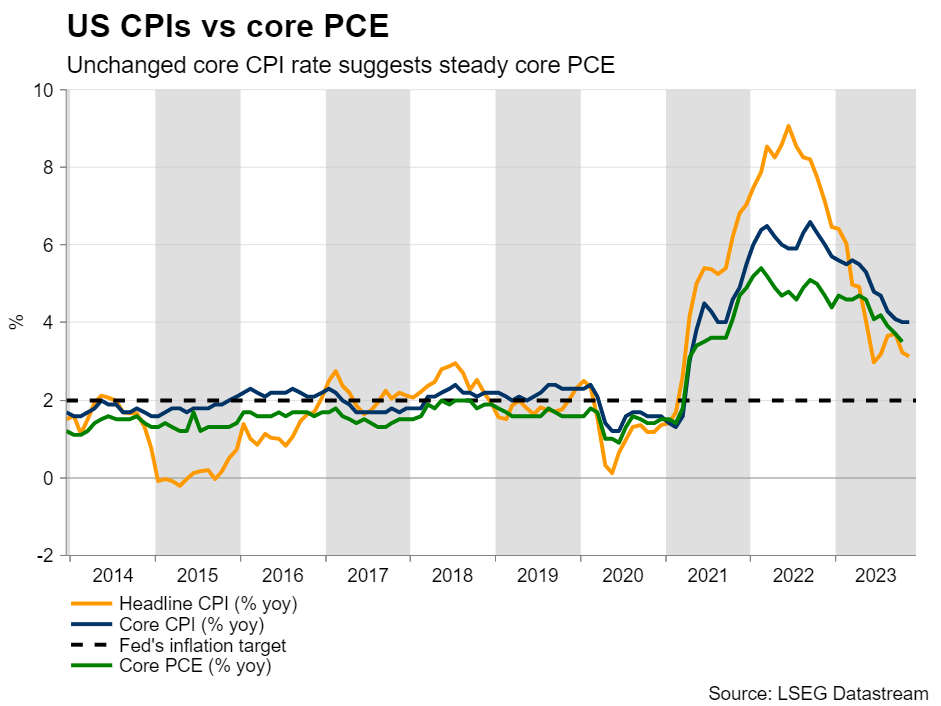

After dovish Fed, greenback merchants lock gaze on core PCE indexSpeaking concerning the Fed, it left rates of interest unchanged as anticipated this Wednesday, however revised down its dot plot to point that rates of interest will finish 2024 at 4.6% as an alternative of 5.1% as projected in September. Powell appeared dovish on the press convention following the choice, saying that greater charges “shouldn’t be the bottom case anymore.” The end result pushed Treasury yields and the US greenback decrease, whereas it was cheered by fairness and gold merchants.

The spotlight on the US agenda subsequent week will be the core PCE index for November, the Fed’s favourite inflation gauge, which comes out on Friday alongside the non-public revenue and spending information for the month. On Tuesday, the core CPI charge for the month remained unchanged at 4.0% y/y suggesting that the core PCE worth index might have additionally held regular at 3.5%. That is unlikely to shake expectations concerning the Fed’s future plan of action, however a miss may encourage buyers to proceed promoting the greenback and shopping for shares. Alternatively, an upside shock might set off a counter transfer, however a gentle one, as market members seem keen to react extra to information and headlines validating their view.

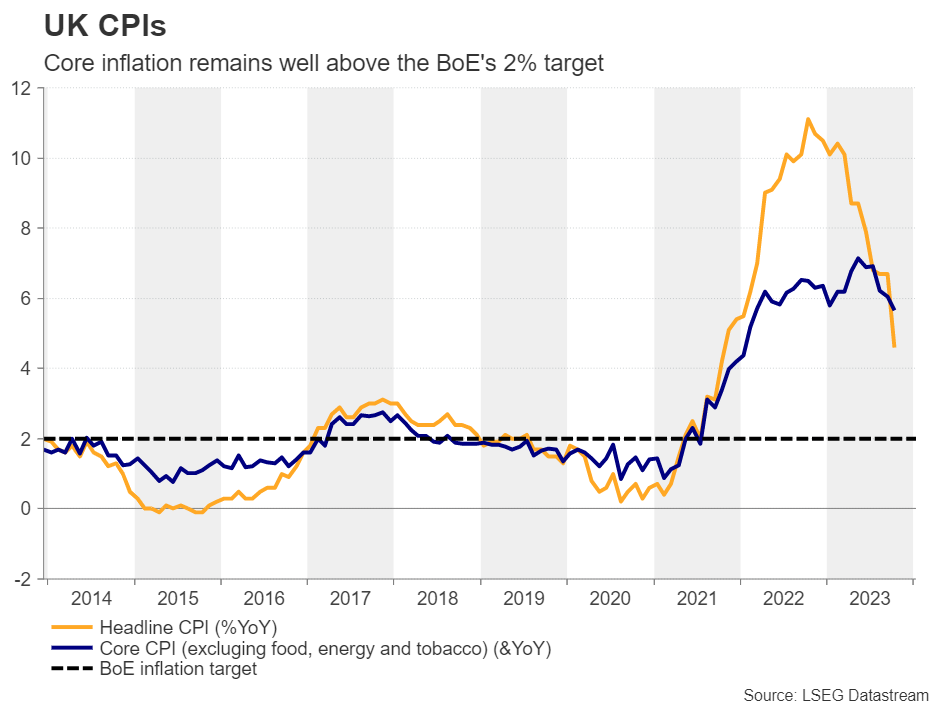

Will UK inflation alter the BoE’s considering?For pound merchants, after the BoE’s hawkish maintain, consideration will now flip to the UK inflation information for November, because of be launched on Wednesday. Though slowing, inflation within the UK is way greater than different main economies, with the core charge declining solely to five.7% from 6.1% in October.

With three members of the BoE voting for a charge hike and most of them saying that it’s too early to conclude that providers inflation and pay progress are on a firmly downward path, some additional, however nonetheless modest, decline in underlying worth pressures might not be a cause for BoE policymakers to alter their minds, and is unlikely to severely damage the pound.

Nonetheless, in line with UK in a single day index swaps, the market continues to imagine that no extra hikes are warranted and that round 115bps price of charge cuts could also be wanted by subsequent December. Maybe they’re extra frightened concerning the efficiency of the UK economic system, which stagnated in Q3, quite than the stickiness of inflation. Due to this fact, ought to upcoming growth-related information proceed to level to deep financial wounds, the pound’s advance might run out of gas in some unspecified time in the future within the not-too-distant future, as buyers insist that some charge reductions might ultimately be wanted. In that respect, the UK retail gross sales for November are scheduled to be launched on Friday.

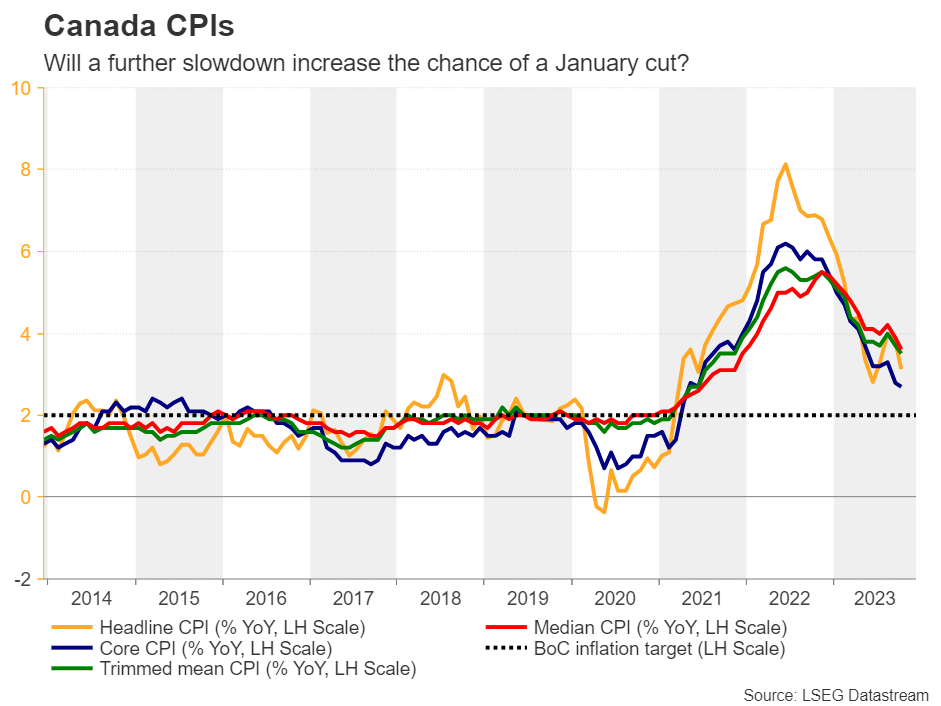

Canadian inflation and RBA minutes additionally on tapThe Canadian inflation numbers for November are additionally popping out on Tuesday. At its newest gathering, the Financial institution of Canada held its key in a single day charge unchanged at 5% and saved the door open to extra tightening, saying that it’s nonetheless involved about excessive inflation, though it acknowledged an easing of worth pressures and an financial slowdown.

Nevertheless, buyers weren’t satisfied that one other charge hike could also be on the horizon. They’re really assigning round a 27% chance for a 25bps minimize in January. In October, headline inflation slowed to only a tick above the Financial institution’s inflation-control goal vary of 1-3%, whereas the carefully watched trimmed imply charge slid to three.5% from 3.7%. Due to this fact, an extra slowdown may take the chance of a January charge discount greater and thereby weigh on the .

Earlier the identical day, and a few hours forward of the BoJ resolution, the RBA releases the minutes of its December coverage assembly, the place policymakers saved their benchmark rate of interest unchanged, however softened their tightening bias, saying that whether or not additional tightening is required will rely upon the info and the evolving evaluation of dangers. With the market assigning a small chance of one other quarter-point hike by the RBA in February, buyers might undergo the minutes and see how keen officers are to press the hike button one final time.

[ad_2]

Source link