[ad_1]

The Eurozone financial system has gone via a tough patch over the past 12 months. Progress has been virtually stagnant, held again by Germany, which fell into contraction as a slowdown in international commerce suppressed demand for exports and crippled the nation’s manufacturing sector.

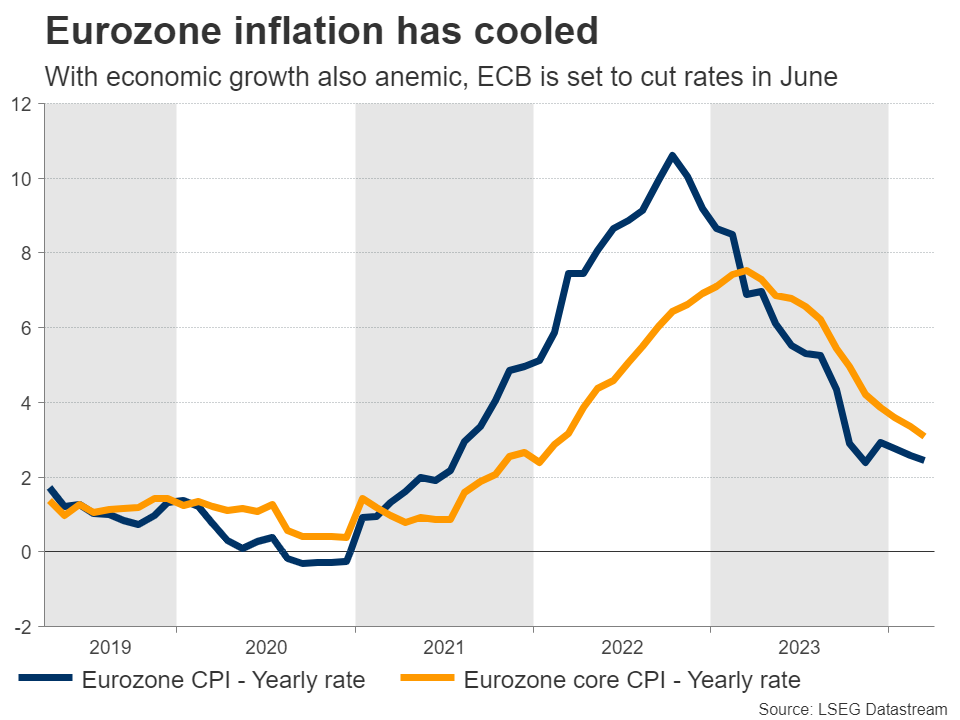

On the intense facet, the financial stagnation has helped dampen inflationary pressures. Inflation fell to 2.4% in March, pushing the European Central Financial institution one step nearer to reducing rates of interest. Most ECB officers have pointed to a reduce in June because the almost definitely state of affairs.

Buyers share this view. A June price reduce is already absolutely priced into cash markets, reflecting the slower development pulse and the cooldown in inflation. The unemployment price has additionally risen a contact this 12 months, reinforcing hopes that inflation is headed decrease.

Subsequently, the ECB will probably use the assembly on Thursday as a stepping stone, setting the stage for summer time price cuts. President Lagarde may spotlight the progress on inflation and argue that reducing charges quickly would assist decrease the danger of a recession.

As for the euro, its gloomy financial fundamentals paint a detrimental image. One motive the one foreign money has been so resilient over the previous 12 months has been the collapse in costs, which benefited the euro via the commerce channel. The euphoric tone in inventory markets additionally helped, by pinning down the safe-haven US greenback.

So the euro has been stored afloat not by financial efficiency, however somewhat by developments in different monetary markets. It is a double-edged sword, as a result of it implies that any change in these tendencies may take away a giant pillar of help for the foreign money.

In different phrases, the euro wants low fuel costs and rising inventory markets to stay above water. In any other case, merchants may begin specializing in the anemic development outlook and price cuts.

US inflation and Fed minutes in focus

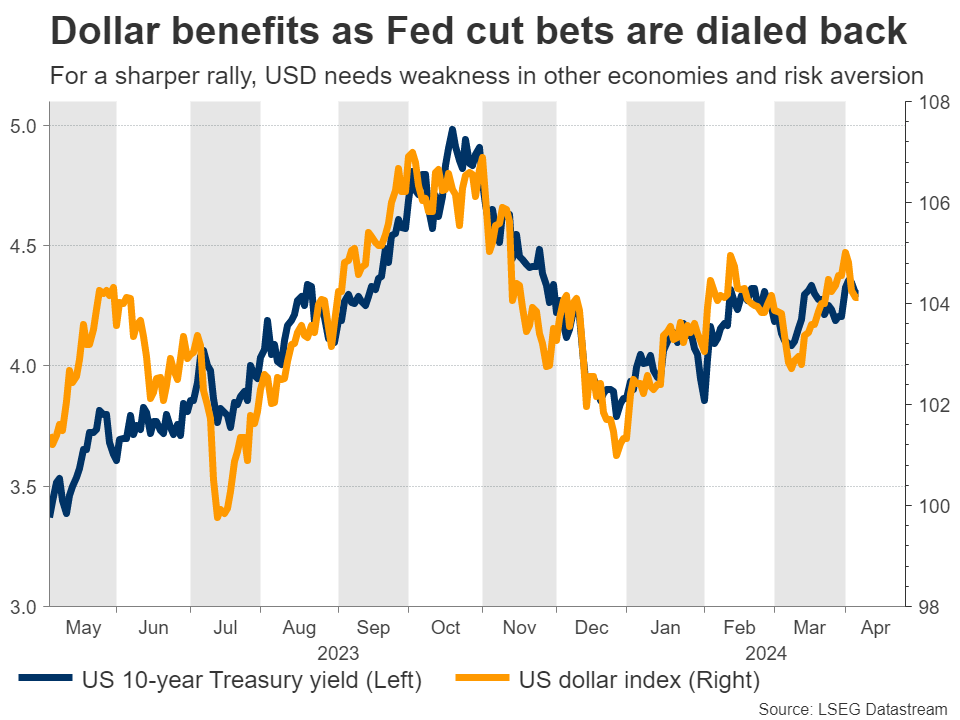

Over in the USA, the focus will fall on CPI inflation knowledge and the minutes of the most recent Fed assembly, each on Wednesday. These will assist traders determine whether or not the Fed will reduce charges in June, which markets at present assign a 70% likelihood to.

Forecasts counsel inflation reaccelerated, with the CPI price seen at 3.4% in March from 3.2% beforehand. Nonetheless, the core price is anticipated to tick down to three.7%. The distinction almost definitely displays the rally in oil in the course of the month, because the core determine excludes the results of vitality costs.

This may translate right into a blended report for the Fed. A decline within the core price would counsel the broader pattern of disinflation continues, even when rising vitality costs are retaining headline inflation elevated.

In the meantime, the minutes will cowl the March assembly, the place FOMC officers upgraded their development and inflation forecasts however nonetheless projected three price cuts for this 12 months. Will probably be fascinating to see the discussions behind the scenes. That mentioned, this launch is unlikely to include any groundbreaking revelations, as most officers have spoken a number of instances since this assembly.

As for the greenback, it went for a wild trip this week, shedding floor after a disappointing ISM companies survey however then recovering with some assist from threat aversion amid fears of an Iranian assault in opposition to Israel.

Total, US financial fundamentals appear stronger than most areas. For example, GDP development is on observe to hit 2.5% this quarter in line with the Atlanta Fed. Subsequently, the broader outlook appears optimistic, though for the reserve foreign money to stage an enduring rally, it would want extra indicators of weak spot in international economies or a risk-off environment that fuels demand for haven property.

Fee choices in Canada and New Zealand

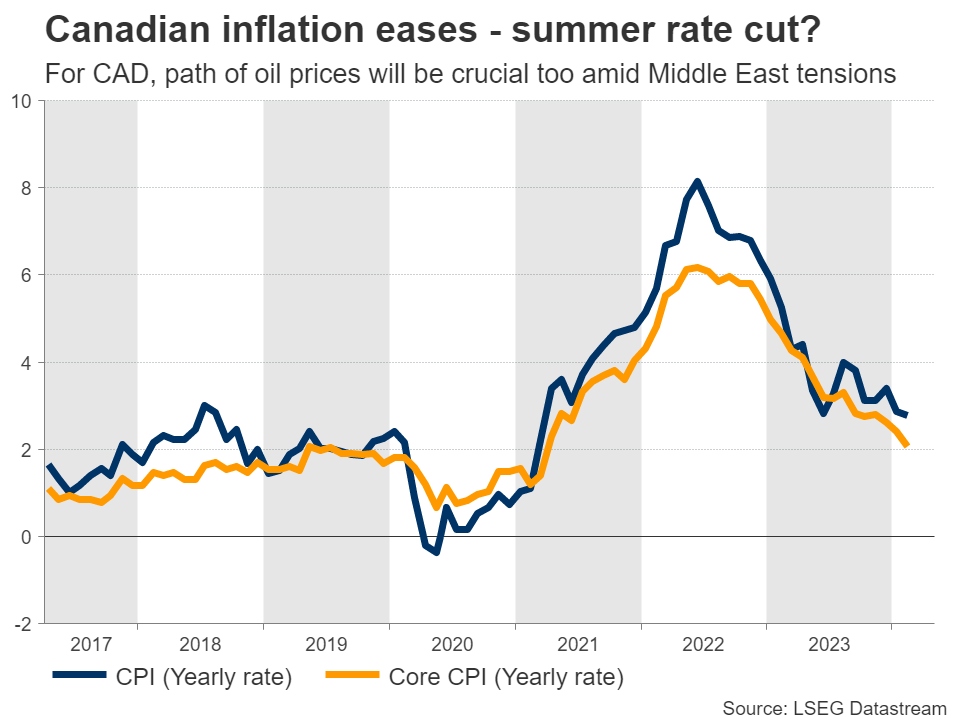

In Canada, the central financial institution meets on Wednesday and markets assign a 15% likelihood for an instantaneous price reduce, as core inflation has declined steadily. Huge inhabitants development has helped to loosen labor market situations, dampening issues about wage-fueled inflation. The detrimental facet of that’s housing shortages, that are retaining shelter inflation scorching.

As such, the Financial institution of Canada is unlikely to slash charges at this assembly, though it would present clearer alerts that cuts are coming this summer time. The Canadian greenback will even be pushed by oil costs, with any escalation within the Center East prone to profit the oil-exporting foreign money.

Crossing into New Zealand, the native foreign money has been on the ropes this 12 months, shedding greater than 4% in opposition to the US greenback. The financial system fell right into a minor technical recession late final 12 months, which has weighed on client and enterprise confidence. However inflation stays elevated, so markets don’t anticipate any transfer from the Reserve Financial institution when it meets on Wednesday.

For the New Zealand greenback to mount a sustainable comeback, it’s going to in all probability want a significant restoration in China that enhances demand for the nation’s commodity exports.

On this sense, China’s commerce knowledge for March might be carefully watched on Friday for any indicators of a rebound. Different notable releases on Friday embody month-to-month GDP stats from the UK.

[ad_2]

Source link