[ad_1]

Traders seeking to US NFPs for affirmation of their Fed fee lower betsRBA may nonetheless sign that larger charges are possibleBut BoC might affirm that rates of interest have peaked in CanadaJapan’s Tokyo CPIs and employment numbers to influence BoJ speculationWill the US jobs report change the greenback’s destiny?The US greenback has been struggling recently on rising bets that the Fed will lower charges massively subsequent yr. The most recent robust hit got here from Fed Governor Waller earlier this week, who stated that if the decline in inflation continues for a number of extra months, they might begin decreasing the coverage fee. This was the primary time a Fed official, and notably a hawkish one, mentioned the opportunity of a lower and that’s why market contributors added to their fee lower bets, with a 25bps lower now being absolutely priced in for Might and the entire variety of foundation factors of fee cuts anticipated for subsequent yr elevated from 90 to round 115.

As they attempt to incorporate each new info into their forecasts, subsequent week, buyers are more likely to flip their consideration again to financial information as Fed officers enter the same old pre-meeting blackout interval, and thus, there will probably be no extra speeches. On Tuesday, the ISM non-manufacturing PMI for November and the JOLTS job openings for October are popping out, whereas on Wednesday, the ADP report for November could also be scrutinized forward of the spotlight of the week, the official employment report for November.

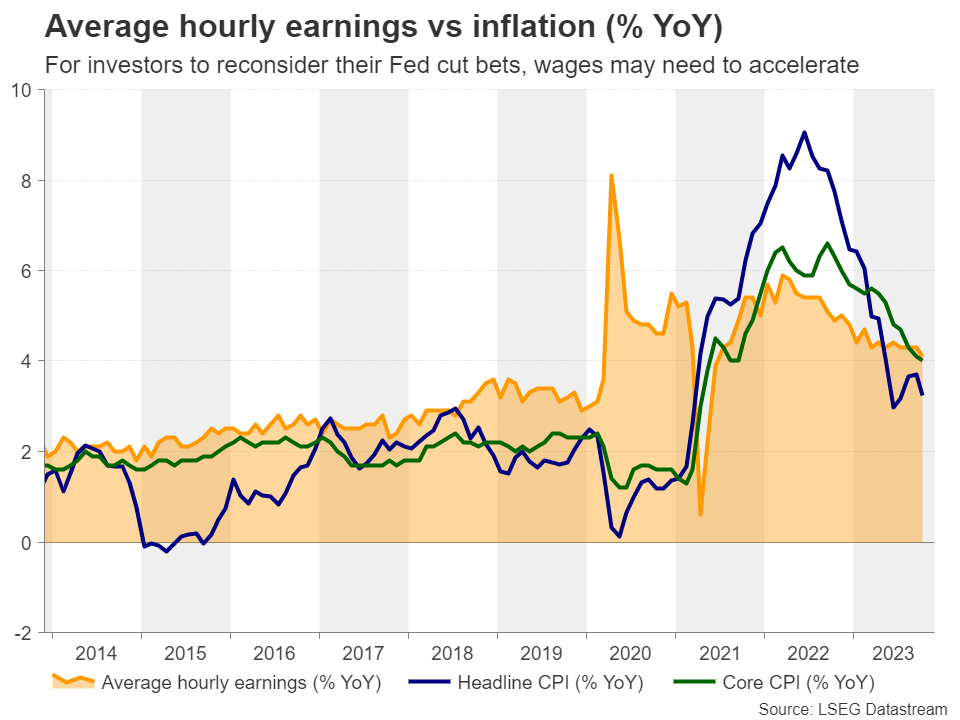

The report is predicted to point out that the unemployment fee held regular at 3.9% and that nonfarm payrolls elevated by 175k in November from 150k in October. Presently, there isn’t any forecast for common hourly earnings. A 3.9% jobless fee and a slight acceleration within the nonfarm payrolls are unlikely to shake a lot market expectations close to a number of fee reductions by the Fed subsequent yr. For that to occur, these numbers might have to be accompanied by a reacceleration in wages.

This might spark some concern that inflation may choose up steam within the months to come back, thereby prompting the Fed to maintain rates of interest excessive for an extended interval than at the moment anticipated. Alternatively, an extra slowdown in wages may solidify buyers’ perception and push the greenback decrease. In any case, recently, market strikes recommend that buyers are promoting the greenback extra aggressively when information or headlines corroborate their view, than shopping for it when there are indications supporting the opposing ‘larger for longer’ case.

Aussie awaits RBA resolution, Australia’s GDP and Chinese language dataAt its November assembly, the RBA raised rates of interest, citing extra persistent inflationary pressures. Nonetheless, within the accompanying assertion, there was a component of uncertainty about whether or not one other fee hike could also be wanted. This resulted in a drop within the Aussie, as heading into the assembly there was confidence that one other quarter-point hike could also be within the works for the flip of the yr.

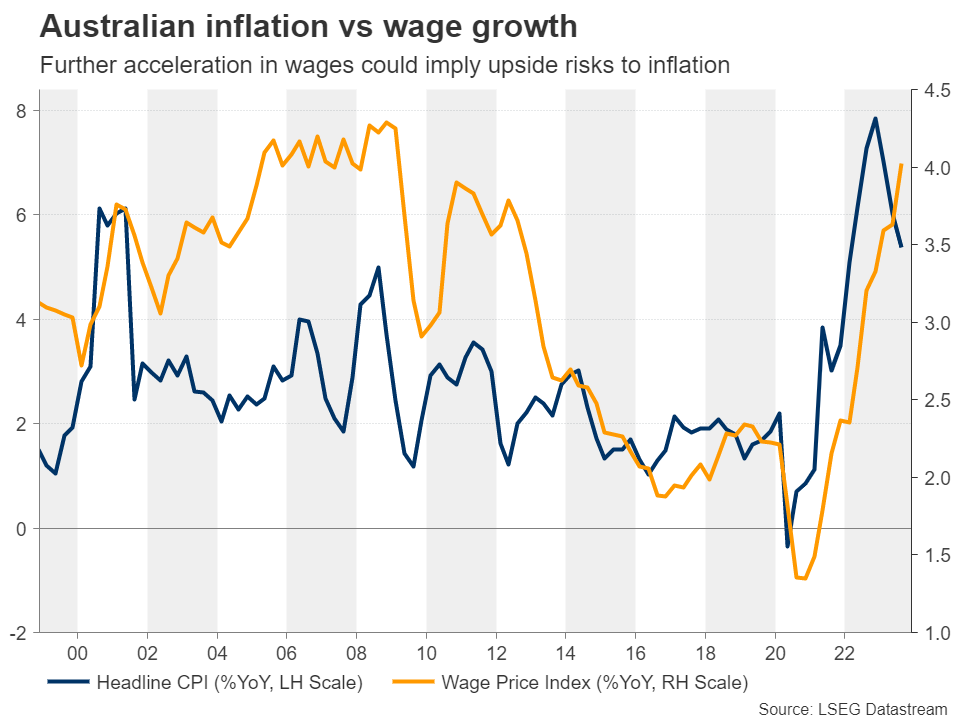

That stated, with the brand new Governor, Michele Bullock sounding hawkish thereafter, and the minutes of that assembly revealing issues about excessive inflation, buyers stored some fee hike bets on the desk. Even after the month-to-month y/y CPI fee for October dropped by greater than anticipated on Wednesday, buyers proceed to assign a good 40% chance for an additional hike by March.

Maybe that’s as a result of the carefully watched trimmed imply CPI solely ticked down to five.3% y/y from 5.4%, which remains to be nicely above the higher certain of the RBA’s 2-3% goal and/or as a result of the month-to-month CPI information doesn’t present all of the elements included within the quarterly CPI. In different phrases, the quarterly studying is a extra dependable inflation metric. The q/q CPI fee for This autumn will probably be obtainable on January 31. What’s extra, the Wage Worth Index for Q3 rose to 4.0% from 3.6%, which suggests upside dangers to inflation within the months to come back.

With all that in thoughts, the RBA is extra more likely to stand pat on Tuesday, however it’s unlikely to obviously sign that this mountaineering cycle is over. Officers are more likely to keep the view that rates of interest may additional rise if wanted, which may enable the to increase its restoration towards the US greenback.

That stated, the aussie will not be pushed solely by the RBA resolution subsequent week, as on Wednesday, Australia’s GDP for Q3 is scheduled to be launched. The forecast is for a slowdown to 0.3% q/q from 0.4%, which may reignite some hypothesis that the RBA is finished elevating charges, even when simply yesterday policymakers sign readiness to do extra. On Thursday, Australia’s and China’s commerce numbers will probably be launched, whereas on Saturday, China publishes its CPI and PPI information. Given the shut commerce ties between Australia and China, extra indicators that the world’s second-largest financial system is bottoming out may enable the aussie to proceed marching north.

Will the BoC sign the tip of this tightening campaign?There may be one other central financial institution resolution on subsequent week’s agenda: The Financial institution of Canada on Wednesday. After they final met, policymakers of this Financial institution held rates of interest regular, citing moderating spending and relieving worth pressures. Nonetheless, they remained ready to boost the coverage fee additional if wanted.

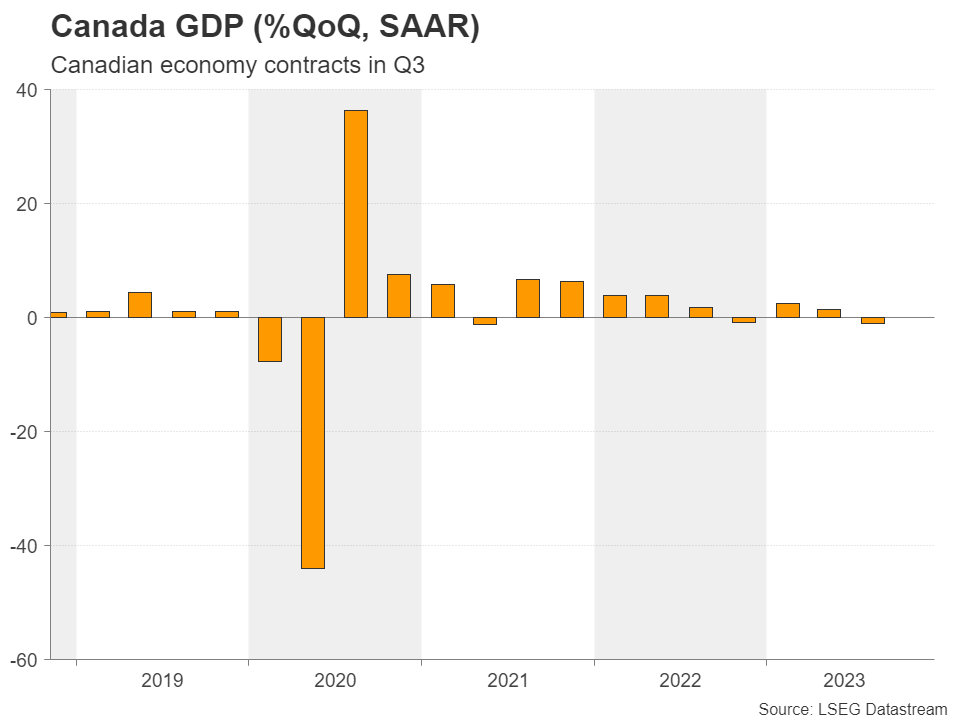

Since then, information have been popping out on the gentle aspect with the unemployment fee rising to five.7% from 5.5% in October, the employment change revealing that the financial system added much less jobs than forecast through the month, and inflation cooling greater than anticipated. This mixed with Thursday’s GDP information for Q3 pointing to a contracting financial system has led buyers to cost in round 105bps price of fee cuts by the tip of 2024.

Though officers are unlikely to verify the market’s view of so many bps price of cuts, they might sign that they’re performed elevating rates of interest, which may harm the . Simply final week, BoC Governor Macklem stated that rates of interest could also be at their peak, on condition that extra demand has vanished, and weak progress is predicted to persist for months.

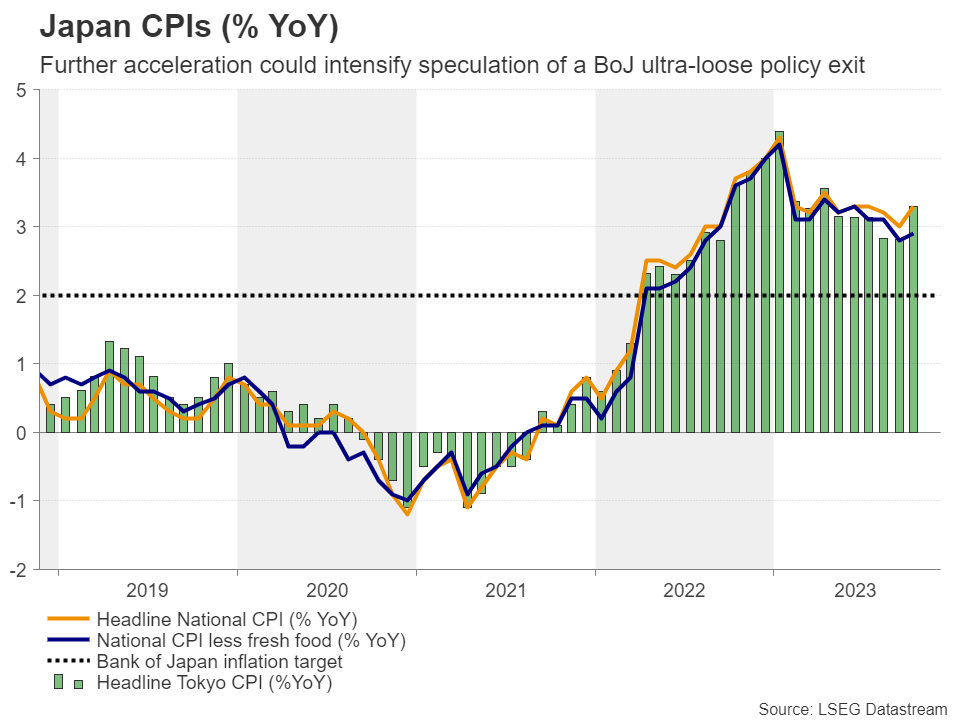

Japanese information may gas hypothesis a few BoJ coverage exit soonIt will probably be an attention-grabbing week for yen merchants as nicely, as through the Asian session Tuesday, Japan’s Tokyo CPI figures are as a consequence of be launched, whereas on Thursday, the ultimate estimate of Q3 GDP and the employment report are popping out. The ultimate estimate of GDP is forecast to verify that the financial system shrank 0.5% in Q3, but when the Tokyo CPIs, that are carefully correlated with the Nationwide numbers, level to additional acceleration in inflation, and the roles information reveal one other choose up in wages, then hypothesis that the BoJ may exit ultra-loose financial coverage circumstances quickly is more likely to intensify, thereby including extra gas to the yen’s engines.

[ad_2]

Source link

Add comment