[ad_1]

Up to date on March twenty eighth, 2024 by Bob Ciura

Over time, the Dividend Aristocrats have confirmed to be among the many best-performing dividend progress shares in the complete market. Broadly talking, the Dividend Aristocrats have management positions of their respective industries, with sturdy aggressive benefits that enable them to generate long-term progress.

The Dividend Aristocrats are a gaggle of 68 firms within the S&P 500 Index, with 25+ consecutive years of dividend will increase.

You may obtain the complete spreadsheet of all 68 Dividend Aristocrats, together with a number of vital monetary metrics reminiscent of price-to-earnings ratios and dividend yields, by clicking on the hyperlink under:

Disclaimer: Positive Dividend is just not affiliated with S&P International in any means. S&P International owns and maintains The Dividend Aristocrats Index. The data on this article and downloadable spreadsheet is predicated on Positive Dividend’s personal evaluate, abstract, and evaluation of the S&P 500 Dividend Aristocrats ETF (NOBL) and different sources, and is supposed to assist particular person buyers higher perceive this ETF and the index upon which it’s primarily based. Not one of the data on this article or spreadsheet is official knowledge from S&P International. Seek the advice of S&P International for official data.

A choose variety of Dividend Aristocrats additionally qualify as Dividend Kings, an much more unique group of 49 shares which have raised their dividends for 50+ consecutive years.

Colgate-Palmolive (CL) is a Dividend Aristocrat and can also be a Dividend King. Colgate-Palmolive’s lengthy historical past of dividend will increase is because of its sturdy manufacturers and dominant place throughout a number of product classes.

Colgate-Palmolive has paid uninterrupted dividends since 1895 and has elevated its dividend funds for the previous 61 consecutive years.

Colgate-Palmolive inventory could also be buying and selling at a premium in the present day, nevertheless it nonetheless stays a robust holding for dependable and regular dividend progress.

Enterprise Overview

Colgate-Palmolive traces its roots all the way in which again to 1806, making it one of many oldest firms within the US inventory market. It was based by William Colgate, who began a starch, cleaning soap, and candle enterprise in New York Metropolis.

At the moment, the corporate manufactures oral care merchandise like toothpaste, private care merchandise reminiscent of cleaning soap, house cleansing merchandise, and pet meals.

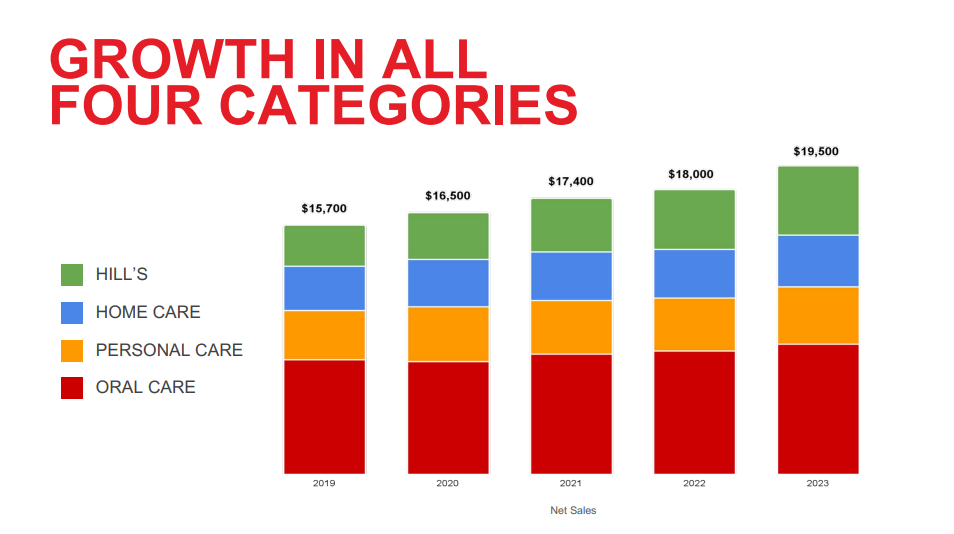

Main manufacturers embrace Colgate, Palmolive, Hill’s Science Weight loss program, and plenty of extra. The core section is Oral Care, which constitutes almost half of the corporate’s revenues. Colgate-Palmolive is a world big. It sells its merchandise in over 200 nations and territories all over the world, and the corporate generates over $19 billion in annual gross sales.

Supply: Investor Presentation

Colgate-Palmolive has a extremely diversified enterprise mannequin by way of merchandise in addition to geographic markets. Roughly half of the corporate’s income comes from rising markets, though its reliance upon these markets for progress has waned a bit just lately.

That is because of the success of the corporate’s pet vitamin enterprise, because it continues to take a income share from different segments. Rising markets will probably be a essential progress catalyst for the corporate shifting ahead. Colgate-Palmolive has the #1 place in China, with a market share above 30%.

Nonetheless, the corporate additionally faces a number of challenges, together with international provide chain points and pronounced inflation that’s growing prices throughout the board, together with in uncooked supplies and labor. These components might hold a lid on progress going ahead.

Progress Prospects

Colgate-Palmolive usually enjoys a world-class model portfolio and high-profit margins. The corporate’s pet meals merchandise, particularly, are a compelling progress catalyst shifting ahead. Pet meals is a progress trade within the U.S.

Colgate posted fourth quarter earnings on January twenty sixth, 2024. The corporate posted an natural gross sales improve of seven% year-over-year for the quarter, which was forward of estimates for a 6.2% acquire. Africa/Euroasia led the way in which with a acquire of 17%, and Latin America was up 16.5%. North America was +3.5% and AsiaPacific was weakest at +1.0%. Natural quantity was flat whereas foreign exchange translation added 0.5% of progress.

Earnings-per-share got here to 87 cents, which was two cents higher than estimates, and up from 77 cents a yr in the past. Working revenue rose 14%. Europe led the way in which from a revenue progress perspective, including 35% year-over-year. Latin America was up 26% on sturdy gross sales features, however Africa/Euroasia revenue declined 15%.

North America noticed a 19% acquire in working revenue. The features in margins have been from value financial savings and better pricing, primarily. Administration guided for 2024 gross sales progress of +1% to +4% on a reported foundation, and natural gross sales to be +3% to +5%.

We see Colgate-Palmolive producing 8% annual earnings-per-share progress on common within the subsequent 5 years.

Aggressive Benefits & Recession Efficiency

Colgate-Palmolive has many aggressive benefits which have fueled its progress over the previous 200+ years.

First, it has constructed a dominant place in its core product classes, most notably in toothpaste, the place Colgate-Palmolive’s market share has risen steadily for a few years. At the moment, it instructions the next market share than the following three largest opponents mixed.

Such a excessive market share permits Colgate-Palmolive to cost increased costs for its premium merchandise and lift costs over time. Pricing energy is a essential aggressive benefit for shopper items shares.

One other main benefit for Colgate-Palmolive is that the merchandise the corporate sells are requirements of recent life. Shoppers want oral, private, and pet care merchandise regardless of financial circumstances. Colgate-Palmolive enjoys regular demand, which supplies the corporate constant profitability, even throughout recessions.

Colgate-Palmolive’s earnings-per-share via the Nice Recession are proven under:

2007 earnings-per-share of $1.69

2008 earnings-per-share of $1.83 (8.3% improve)

2009 earnings-per-share of $2.19 (20% improve)

2010 earnings-per-share of $2.16 (1.4% decline)

Colgate-Palmolive generated optimistic earnings progress in 2008 and 2009, through the worst years of the recession. Earnings dipped barely in 2010 however resumed rising in 2011 and thereafter.

The corporate’s sturdy efficiency from 2007-2010 is a credit score to its sturdy enterprise mannequin and highly effective manufacturers. These similar qualities helped Colgate-Palmolive stay extremely worthwhile and lift its dividend in 2020, even with the influence of the worldwide coronavirus pandemic.

Colgate-Palmolive’s dividend can also be very secure. The corporate has a projected dividend payout ratio of slightly below 60% for fiscal 2024, which means that the dividend is well-covered.

Valuation & Anticipated Returns

With expectations of about $3.45 in earnings-per-share for 2024, Colgate-Palmolive inventory has a price-to-earnings ratio of 26.1.

Our honest worth estimate for CL inventory is a P/E a number of of 24. Subsequently, the inventory seems to be barely overvalued. A declining P/E a number of might cut back annual returns by -1.7% per yr over the following 5 years.

As well as, CL shares have a present dividend yield of two.2%.

Assuming the inventory maintains a reasonably steady valuation forward, together with our projected earnings progress and estimated adjusted earnings-per-share for 2024, we forecast Colgate Palmolive can produce annualized complete returns of roughly 8.5% via 2029.

Now we have assigned a maintain ranking to the corporate’s shares in consequence.

Ultimate Ideas

Colgate-Palmolive is a high-quality enterprise with a number of category-leading manufacturers. The corporate has progress potential via product innovation, its Hill’s pet meals model, and progress in rising markets.

Colgate’s dividend ought to stay well-covered, and so additional dividend hikes within the coming years must be comparatively simple.

With annual returns just under 9%, we at the moment fee CL inventory a maintain.

On the lookout for extra reliable dividend progress shares? The next Positive Dividend databases include essentially the most reliable dividend growers in our funding universe:

In case you’re on the lookout for shares with distinctive dividend traits, contemplate the next Positive Dividend databases:

The foremost home inventory market indices are one other stable useful resource for locating funding concepts. Positive Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to help@suredividend.com.

[ad_2]

Source link