[ad_1]

The Magnificent Seven consists of among the most revolutionary tech-orientated corporations available on the market. However what if there was a Magnificent Seven for dividend shares?

Microsoft (NASDAQ: MSFT), Coca-Cola (NYSE: KO), Procter & Gamble (NYSE: PG), Chevron (NYSE: CVX), House Depot (NYSE: HD), JPMorgan Chase (NYSE: JPM), and United Parcel Service (NYSE: UPS) characterize their industries properly and are all high dividend shares you possibly can depend on for many years to come back. This is why they’d make my listing for the Magnificent Seven of dividend shares.

1. Microsoft

Microsoft is the one Magnificent Seven inventory that additionally deserves to be within the Magnificent Seven of dividend shares. It’s the most beneficial firm on this planet. Microsoft solely yields 0.7%, nevertheless it pays probably the most dividends of any U.S.-based firm.

Microsoft’s low yield is because of its outperforming inventory worth, not an absence of dedication to dividend raises. Since fiscal 2019, Microsoft has raised its dividend by 9% to 11% yearly like clockwork. The dividend has doubled over the past eight years — a quicker progress price than most of the market’s high dividend shares.

Microsoft is monetizing synthetic intelligence and rising its earnings, paving the best way for loads of future dividend raises. If the inventory worth languishes, the dividend yield will rise to a way more enticing degree. Nevertheless, Microsoft shareholders would certainly favor outsized features over a better dividend yield.

2. Coca-Cola

Coke makes use of its dividend as the first approach to reward devoted shareholders. With a yield of three.2%, Coke permits traders to gather passive revenue from a tried and true Dividend King with 62 consecutive annual dividend will increase.

Coke is a low-growth enterprise, so traders should not anticipate outsized features from the inventory. However that is the Magnificent Seven of dividend shares, not progress shares. And relating to producing passive revenue, Coke is as dependable because it will get.

Coke’s consistency is the core cause why Warren Buffett’s Berkshire Hathaway has held the inventory for over 30 years.

Story continues

If it had been a choice between Coke and a 10-year Treasury, I would take Coke all day. The ten-year provides traders one other share level or so in yield, however with no participation out there. In fact, no inventory is as secure because the risk-free price, however Coke is shut. It is the perfect funding for risk-averse traders or anybody seeking to complement revenue in retirement.

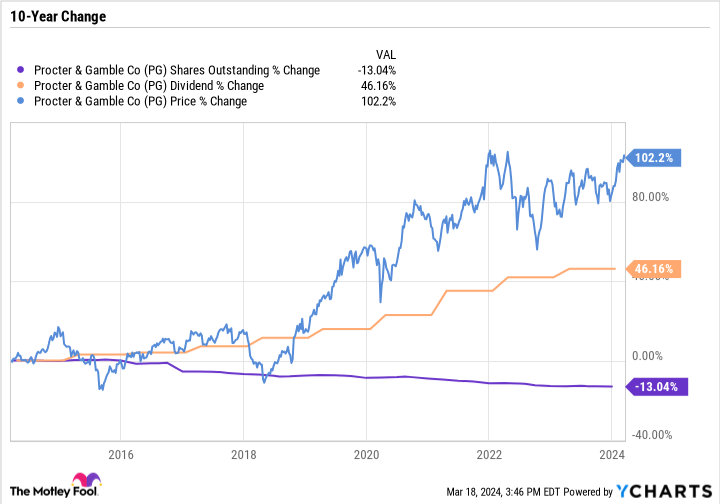

3. Procter & Gamble

Procter & Gamble has a large capital return program. It’s a nice instance of an organization utilizing dividends and inventory repurchases to reward shareholders.

The next chart is likely one of the prettiest you may ever see from a stodgy shopper staple firm.

P&G inventory has greater than doubled over the past decade, the dividend is up over 46%, and P&G has repurchased a substantial quantity of inventory, decreasing its share depend by 13%.

P&G is probably not probably the most thrilling enterprise, however glitz and glam is not the purpose of this listing. On the subject of rewarding shareholders, P&G has completed it in some ways and has the enterprise mannequin and model energy wanted to proceed that streak going ahead.

4. Chevron

Chevron’s inventory buybacks aren’t practically as constant as P&G’s. The oil big tends to purchase again extra inventory throughout an uptick within the enterprise cycle and pull again on repurchases and capital spending when oil and fuel costs fall.

However Chevron’s dividends are as constant as they arrive. Chevron has raised its dividend for 37 consecutive years. Meaning it did not reduce it through the COVID-19-induced crash, the 2014 and 2015 downturn, or any oil and fuel downturn for the reason that late Nineteen Eighties.

Chevron has the stability sheet, value profile, and portfolio to proceed rewarding shareholders. Its dividend yield of 4.2% makes it one of many higher-yielding dependable shares on the market.

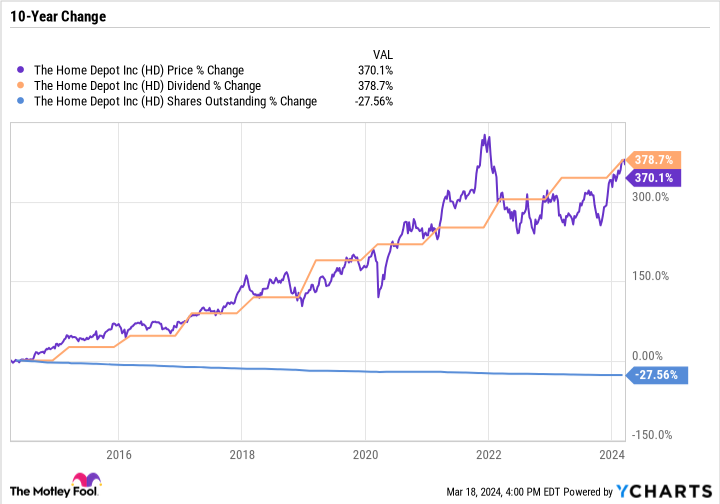

5. House Depot

House Depot has been an ideal dividend inventory over the past decade. It has crushed the broader market, and someway, the dividend has grown at an ever quicker price.

House Depot has additionally decreased its share depend by over a fourth whereas increasing the enterprise.

Traders should not anticipate this degree of progress over the following 10 years, however House Depot continues to be a great funding. The corporate is susceptible to exterior elements, akin to broader financial cycles, the housing market, the development {industry}, and shopper spending. However it’s properly positioned, and probably the greatest cyclical dividend shares to personal long run.

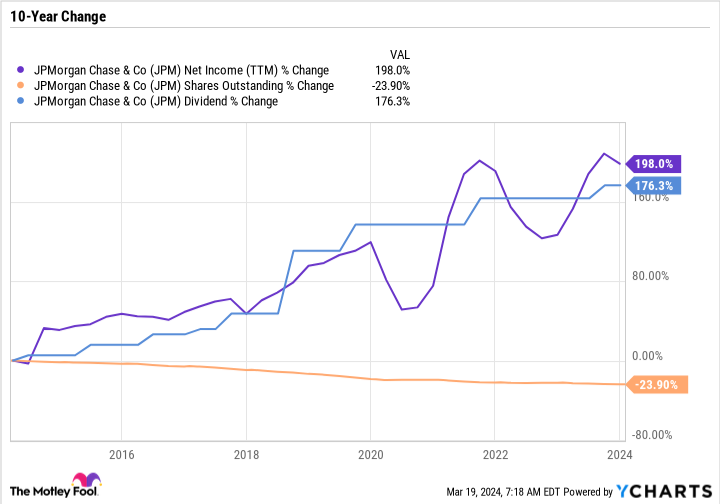

6. JPMorgan Chase

Since Nov. 1, JPMorgan is up over 38% — a large transfer for such a big, diversified financial institution. JPMorgan is now price greater than Financial institution of America, Wells Fargo, and half of Citigroup mixed. The Massive 4 banks have actually become JPMorgan and the opposite three.

Banking is a cyclical {industry} that tends to ebb and circulate to the tune of the broader financial system. Proper now, JPMorgan’s income are hovering.

Nonetheless, what makes the corporate a great long-term funding, and a worthy addition to the Magnificent Seven of dividend shares, is that it recurrently returns worth to its shareholders. Over the past decade, the dividend is up 176%, whereas the share depend is down practically a fourth.

JPMorgan slashed most of its dividend in 2009 through the fallout of the monetary disaster. However since then, it has raised its dividend yearly. At this time, the dividend is sort of triple what it was pre-cut, and JPMorgan has become a top quality passive revenue play.

The latest run-up within the inventory worth has pushed JPMorgan’s yield right down to 2.2%. However the firm is on the high of its recreation and is an effective consultant of the financials sector within the Magnificent Seven of dividend shares.

7. UPS

UPS has raised its dividend yearly for the final 21 years, apart from in 2009, when it saved its dividend flat. The corporate is not probably the most dependable dividend payer on this listing, nevertheless it has more and more used dividends as a key approach to reward shareholders.

In 2022, UPS raised its dividend by 49%, a big improve for its measurement. At this time, UPS yields 4.3%, which is excessive for an industry-leading industrial firm.

UPS is a cyclical enterprise that is determined by the energy of the broader financial system. Package deal supply volumes to companies are larger throughout an financial enlargement. Equally, deliveries to shoppers are larger when discretionary spending is robust.

Though UPS affords traders a compelling yield, it is uncertain the corporate will make as massive of raises to its dividend going ahead. Nonetheless, its present degree is sort of excessive, as UPS inventory must rally about 45% for the yield to fall under 3%.

Completely different corporations, comparable investments

Microsoft, Coca-Cola, Procter & Gamble, Chevron, House Depot, JPMorgan Chase, and UPS have observe information of dividend raises, stable underlying companies, future progress prospects, and {industry} management. Many of those corporations additionally reward shareholders with inventory repurchases, in addition to long-term capital features for affected person traders.

These corporations might not all the time have the very best yields, however they do have earnings progress, which units the stage for future raises.

The place to take a position $1,000 proper now

When our analyst staff has a inventory tip, it might pay to hear. In any case, the e-newsletter they’ve run for 20 years, Motley Idiot Inventory Advisor, has greater than tripled the market.*

They only revealed what they imagine are the ten greatest shares for traders to purchase proper now… and Microsoft made the listing — however there are 9 different shares you might be overlooking.

See the ten shares

*Inventory Advisor returns as of March 21, 2024

Financial institution of America is an promoting associate of The Ascent, a Motley Idiot firm. Wells Fargo is an promoting associate of The Ascent, a Motley Idiot firm. JPMorgan Chase is an promoting associate of The Ascent, a Motley Idiot firm. Citigroup is an promoting associate of The Ascent, a Motley Idiot firm. Daniel Foelber has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Financial institution of America, Berkshire Hathaway, Chevron, House Depot, JPMorgan Chase, and Microsoft. The Motley Idiot recommends United Parcel Service and recommends the next choices: lengthy January 2026 $395 calls on Microsoft and brief January 2026 $405 calls on Microsoft. The Motley Idiot has a disclosure coverage.

If There Was a “Magnificent Seven” for Dividend Shares, These Would Be My High Picks was initially revealed by The Motley Idiot

[ad_2]

Source link