[ad_1]

Ole Schwander

Novo Nordisk (NVO) inventory is up greater than 30% YTD after having already tripled since 2020.

In search of Alpha

Regardless of the inventory’s improbable previous share worth efficiency, I proceed to see upside in NVO inventory. Actually, as I see Novo Nordisk doubling revenues by 2027, and producing $100 billion in revenues by 2030 on a higher than 30% EBIT margin, my valuation mannequin means that Novo Nordisk could also be greater than 50% undervalued. On the backdrop of surging demand for diabetes and weight problems care, with an annual TAM potential of $350-450 billion by 2030, I see Novo Nordisk turning into the primary European Champion topping the one trillion greenback market capitalization benchmark. Robust Purchase.

A Targeted Pharma Firm

Novo Nordisk is a Danish pharmaceutical firm that operates in additional than 170 international locations. The corporate’s main focus is on diabetes care and different severe power circumstances, corresponding to weight problems, hemophilia, and progress hormone remedy. In that context, Novo Nordisk has a broad portfolio of pharmaceutical merchandise, starting from insulin merchandise (NovoLog, Levemir, and NovoMix) to GLP-1 Receptor Agonists treating sort 2 diabetes (Victoza, Ozempic, and Rybelsus) to hemophilia therapies (NovoSeven and NovoEight), weight problems therapies (Saxenda), and hormone substitute remedy merchandise.

Novo Nordisk

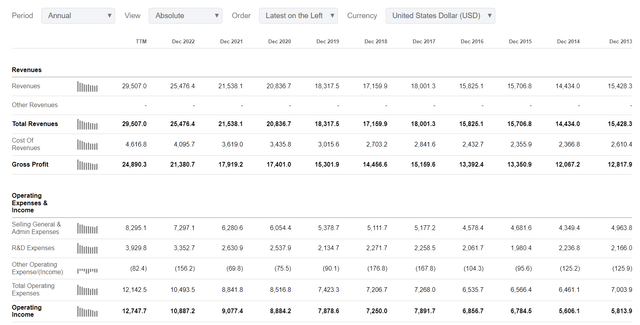

With a deal with treating metabolic ailments, Novo Nordisk has positioned itself within the “bulls-eye” of the worldwide pharma market, as evidenced by the corporate’s long-standing, sturdy monitor -record of income progress and worth accumulation: Over the previous decade, Novo Nordisk has managed to develop its topline each single 12 months since FY 2014, greater than doubling the corporate’s income base from $14.4 billion in 2014 to $29.5 billion for the trailing twelve months, an implied CAGR of near ~8%. In the identical interval, an identical pattern is notable for gross revenue and working earnings, with compounded annual progress charges of ~8% and ~9%, respectively.

In search of Alpha

Development Outlook Is Very Promising

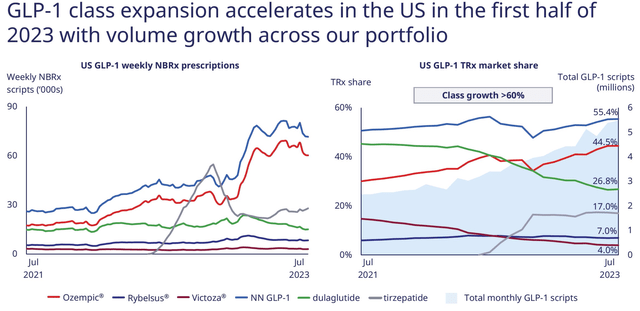

Novo Nordisk’s progress prospects are promising, with the corporate’s market share in weight problems care rising quickly over the previous few years. With that body of reference, it’s price mentioning that the weight problems market is predicted to exceed $100 billion by 2031, in keeping with Jefferies, with possible further, materials upside relying to what extent weight problems will be linked to broader well being points. In August, for instance, Novo Nordisk efficiently proved that Wegovy, the corporate’s weight-loss-drug, reduces the danger of cardiac occasions like coronary heart assaults by roughly 20%. Extra not too long ago, it has additionally been instructed that Novo’s GLP-1 franchise might assist kidney well being.

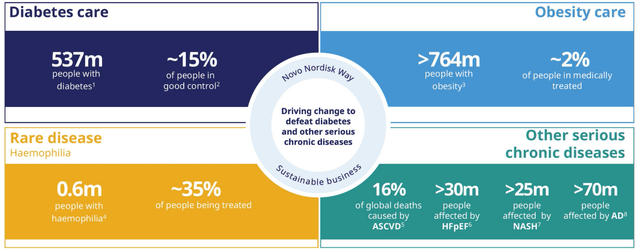

In response to Novo Nordisk itself, the complete future potential of the weight problems care market may very well be a lot bigger than what Jefferies estimated — referencing 764 million individuals identified with weight problems well being points, of which solely 2% are presently medically handled, in keeping with Novo Nordisk estimates. Actually, projecting that each weight problems affected person equals roughly $12,000 in annual income, in keeping with previous spending on weight problems medicine per affected person, and estimating that about 4-5% of the market is serviceable with weight problems medicine by 2030 (as in comparison with 2% presently; discounting for affordability, willingness to take medicine, insurance coverage protection, in addition to entry to remedy), the worldwide weight problems market might fairly be estimated at $350-450 billion, yearly.

Novo Nordisk

If my market sizing is right, and assuming that Novo Nordisk doesn’t lose greater than 20-25 share level market share within the GLP-1 market (taking U.S. market as enclosed because the benchmark), then Novo Nordisk’s FY 2030 potential for the corporate’s GLP-1 franchise would high $100 billion. Now, in my view, assuming a 20-25 share level market share loss could be very pessimistic already; and thus, my estimate ought to carry threat to the upside.

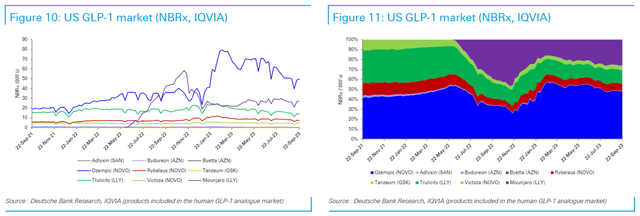

Deutsche Financial institution analysis, IQVIA

Once more increasing on Novo Nordisk proprietary estimates, it’s price mentioning that the corporate’s administration targets a 30% group CAGR by way of 2025. That mentioned, it’s price noting that Novo Nordisk quarterly outcomes reveal a robust tendency of underestimating the corporate’s future progress, as instructed by 7 upward revision in gross sales steering over the previous 12 quarters. Actually, solely not too long ago (13 October), Novo raised gross sales progress and earnings steering as soon as extra, after elevating in August with Q2 reporting, commenting on the distinctive energy of the GLP-1 franchise:

The gross sales outlook for 2023 is up to date, primarily reflecting increased full-year expectations for Ozempic® volumes bought within the US and gross-to-net gross sales changes for Ozempic® and Wegovy® within the US.

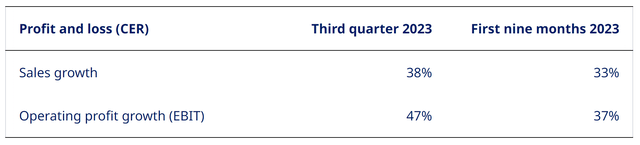

For Q3 2023, Novo now expects gross sales progress and EBIT progress of 38% YoY and 47% YoY, respectively.

Novo Nordisk

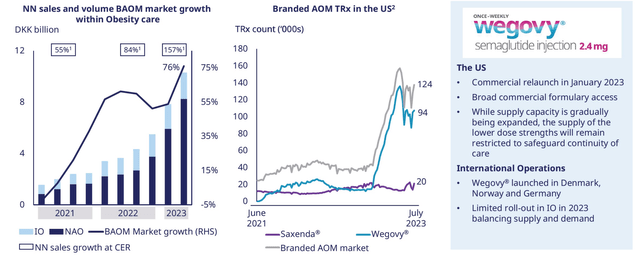

In my view, it’s cheap to estimate Novo Nordisk’s compounded annual progress for GLP-1 nearer to ~28-30, if the corporate can handle provide chain limitations. Simply to provide some context, in FY 2021, FY 2022, and FY 2023, weight problems gross sales really jumped YoY by 55%, 84%, and 157%, respectively. Evidently, these numbers don’t counsel a slowing in progress charges, however an acceleration.

Novo Nordisk Novo Nordisk

Residual Earnings Mannequin

Novo Nordisk inventory does worth plenty of optimism, buying and selling at a ahead P/E of roughly 37x. Nonetheless, the optimism remains to be underestimating Novo’s potential. There have been many shares that have been a discount at comparable valuation metrics, at comparable market capitalization (Nvidia, Microsoft, Apple, Tesla, to call probably the most notable); and I imagine Novo is one such alternative.

To again up my confidence, I’ve constructed a residual earnings mannequin for NVO inventory. The residual earnings mannequin anchors on the concept a valuation ought to equal a enterprise’ discounted future earnings after capital cost. As per the CFA Institute:

Conceptually, residual earnings is web earnings much less a cost (deduction) for widespread shareholders’ alternative value in producing web earnings. It’s the residual or remaining earnings after contemplating the prices of all of an organization’s capital.

With that mentioned, for my Novo Nordisk inventory valuation mannequin, I make the next assumptions:

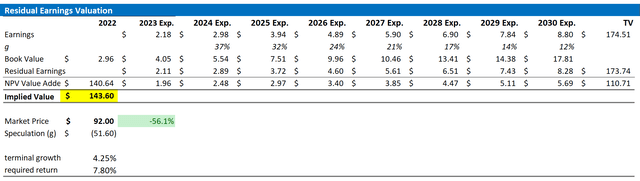

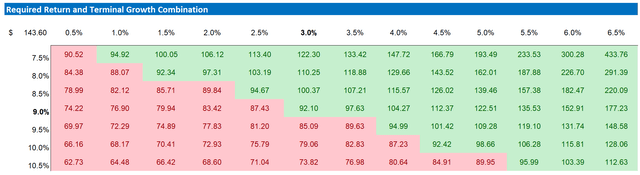

To forecast 2025 gross sales, I anchor on my beforehand mentioned 30% CAGR progress estimate; I see $100 billion for 2030 on a 25-30% market share within the $350-450 billion weight problems care TAM. To estimate the capital cost, I anchor on NVO’s value of fairness at 7.8%, in keeping with the CAPM mannequin. For the terminal progress charge after 2025, I apply 4.25%, which I imagine is an affordable estimate post-2030, as my weight problems care SAM estimate by 2030 solely references about 30% addressability. Traders with completely different assumptions relating to NVO’s value of capital and terminal progress might take reference from the sensitivity desk enclosed.

Given the above assumptions, I calculate a base-case goal worth for Novo Nordisk of about $143.6/share, discounted to 2023 worth. (Repricing as much as 2028, Novo’s valuation would break the $1 Trillion market capitalization benchmark).

Firm Financials, Creator’s EPS Estimates; Creator’s Calculation

As promised, beneath can be the sensitivity desk, testing numerous terminal progress charge and price of fairness assumptions.

Firm Financials, Creator’s EPS Estimates; Creator’s Calculation

Ideas on Dangers

Investing in Novo Nordisk huge potential shouldn’t be with out dangers. Particularly, buyers ought to be aware that the pharmaceutical trade is topic to rigorous laws that may have an effect on pricing, reimbursement, and drug approvals. In that context, the sooner Novo Nordisk’s addressable market is rising, the extra are healthcare methods/ governments motivated to manage pricing. As well as, growing competitors in diabetes and weight problems care market should not be ignored. Concerns about competitors are particularly noteworthy within the context of the success of Eli Lilly’s (LLY) Mounjaro. Furthermore, Novo Nordisk’s progress outlook could also be constrained by provide limitations, as the corporate might battle to fulfill the large, surging demand for its weight problems drug, Wegovy. Lastly, broader market circumstances and financial components also can affect Novo Nordisk’s inventory worth.

Conclusion

Novo Nordisk’s inventory has loved an unlimited progress tailwind from weight problems care, offering buyers with spectacular multi-year features. Regardless of this outstanding efficiency, nevertheless, the Danish pharma firm seems to nonetheless have important upside potential. The corporate’s GLP-1 franchise is a key driver of this progress, with a possible TAM of $350-450 billion by 2030. Anchored on this, my projections counsel that Novo Nordisk might double its revenues by 2027 and obtain $100 billion in revenues by 2030, with a secure EBIT margin above 30%. This evaluation, together with a residual earnings mannequin, implies that the inventory could also be undervalued by greater than 50%. Novo Nordisk inventory is a Robust Purchase on an distinctive progress outlook and product energy.

[ad_2]

Source link