[ad_1]

DNY59

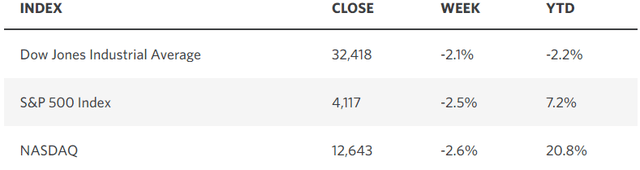

Defying the skeptics all yr lengthy, customers continued to energy the continued enlargement, as financial progress within the third quarter soared at an annualized 4.9%. But that didn’t drive rates of interest increased, because the consensus may need anticipated as a result of inflation information in the report was higher than anticipated. Consequently, bond yields throughout the curve declined from their current highs. Company earnings for the third quarter have additionally been higher than anticipated thus far this earnings season. Regardless, the foremost market averages have been decrease throughout the board final week with the S&P 500 and Nasdaq Composite coming into correction territory with declines over the previous three months of greater than 10%. Countering financial resilience, the market has been digesting a better interest-rate atmosphere with the added headwinds of Washington’s disfunction, the United Auto Staff strike, and warfare within the Center East. The problem now’s when market costs greater than accounted for increased rates of interest and these near-term headwinds, setting the stage for the restoration.

Edward Jones

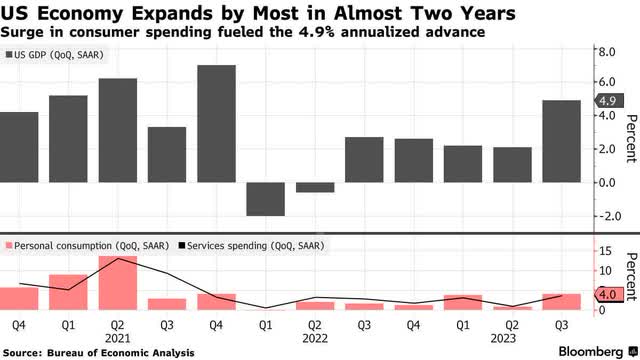

The financial system expanded within the third quarter on the quickest tempo for the reason that fourth quarter of 2021. Progress was fueled primarily by a 4% improve in client spending, however the perfect information within the GDP report was on the inflation entrance, because the core private consumption expenditures (PCE) worth index rose at a charge of two.4% through the quarter, which was beneath the two.5% expectation and three.7% charge within the second quarter. That was the slowest tempo since 2020 and is quickly approaching the Fed’s goal of two%.

Bloomberg

Confirming what we realized within the newest Shopper Value Index report, the core PCE rose at a charge of simply 1.8% through the third quarter once we excluded housing. That is vitally vital as a result of we all know that shelter prices are sure to decelerate quickly within the coming months, which ought to carry the Fed’s most popular measure down to focus on through the first half of 2024.

Bloomberg

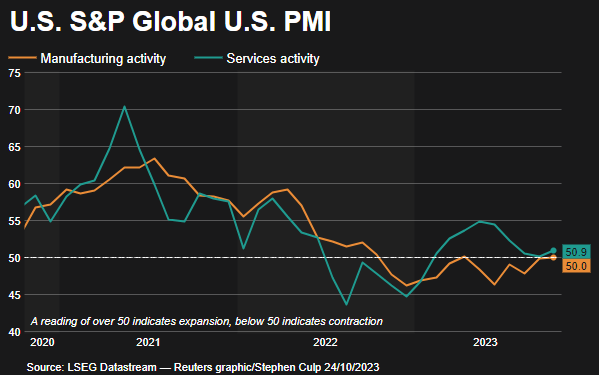

Regardless of current financial power, nobody is anticipating one other charge hike from the Fed’s assembly this week. That’s as a result of it’s properly understood that financial exercise will gradual sharply within the present quarter underneath the burden of a lot tighter monetary situations that developed over the previous three months. Nonetheless, final week’s measure of financial exercise throughout October from S&P International confirmed an honest begin to the fourth quarter. The service sector index rose to a three-month excessive of fifty.9, whereas the manufacturing sector is at a six-month excessive and on the cusp of progress at 50.0 after a yr of contraction.

Reuters

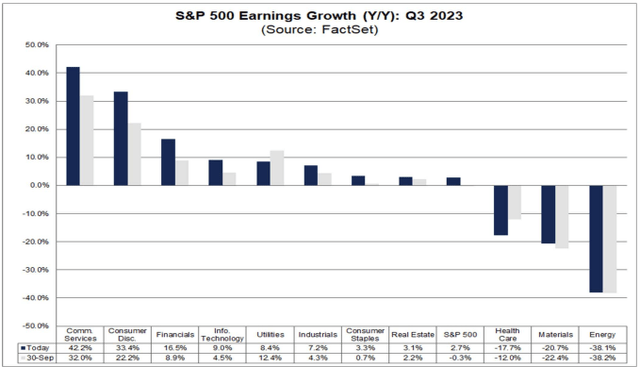

Disinflation mixed with resilient progress has been a tailwind for company income, which has resulted in a return to year-over-year earnings progress for the primary time for the reason that third quarter of final yr. Midway by way of the earnings season, income are actually rising 2.7%, which is healthier than the 0.3% decline anticipated at the start of October. Higher but, when the vitality sector is excluded, income have risen 8.4%.

FactSet

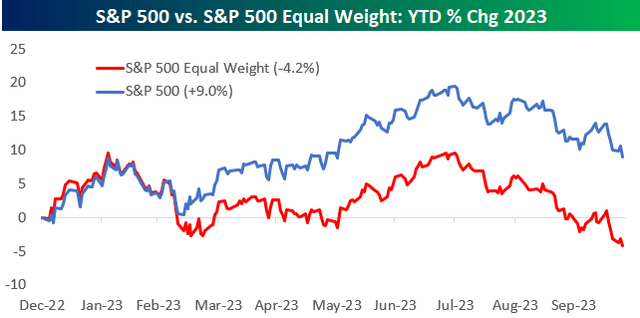

Regardless of the outperformance, the S&P 500 has declined roughly 3% thus far this month and 10% from its peak this yr, because the market digests the upper interest-rate atmosphere. There may be additionally the expectation for a deceleration in financial exercise that’s breeding warning from company administration groups. This is the reason now we have had a correction over the previous three months, however I feel now we have largely priced in these developments with extra affordable valuations. The S&P 500 now trades at a ahead price-to-earnings a number of of 17.1, which is beneath its 5- and 10-year averages. Extra importantly, the equal-weighted index a number of is all the way down to 14 occasions, whereas the Russell 1000 Worth index is all the way down to 13 occasions. The S&P 500 index remains to be being closely influenced by the Magnificent 7 (Amazon, Apple, Alphabet, Meta, Microsoft, Nvidia, and Tesla), buying and selling at a mean of 30 occasions and accounting for greater than 30% of the index worth.

Bespoke

Nobody rings a bell on the tops and bottoms, as each are processes, however this looks like we’re transferring nearer to the tip of the correction course of. There may be now lots of worth within the common inventory, particularly the place dividend yields are difficult the 5% provided by every part from cash markets to longer-term bonds, that are yields that will not final when the financial system slows, and the Fed begins to scale back charges in some unspecified time in the future subsequent yr. Moreover, market technicals are deeply oversold and sentiment is approaching extraordinarily bearish ranges, each of that are good contrarian indicators pointing to a rebound throughout two of the best-performing months of the yr in November and December.

[ad_2]

Source link